What is the current valuation of the Gluten-free Bakery Market?

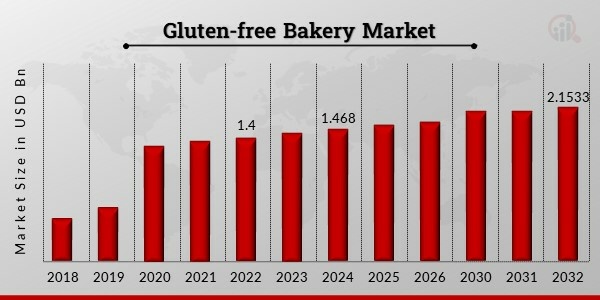

The Gluten-free Bakery Market was valued at 1.468 USD Billion in 2024.

What is the projected market size for the Gluten-free Bakery Market by 2035?

The market is projected to reach 2.485 USD Billion by 2035.

What is the expected CAGR for the Gluten-free Bakery Market during the forecast period?

The expected CAGR for the Gluten-free Bakery Market from 2025 to 2035 is 4.9%.

Which product segment holds the highest valuation in the Gluten-free Bakery Market?

The Main Ingredients segment holds the highest valuation, with a range from 1.0 to 1.7 USD Billion.

How do the sales of Cookies & Biscuits compare to Doughnuts in the market?

Cookies & Biscuits generated between 0.25 and 0.4 USD Billion, whereas Doughnuts accounted for 0.15 to 0.25 USD Billion.

What are the key players in the Gluten-free Bakery Market?

Key players include Udi's Gluten Free, Schär, Canyon Bakehouse, and Katz Gluten Free, among others.

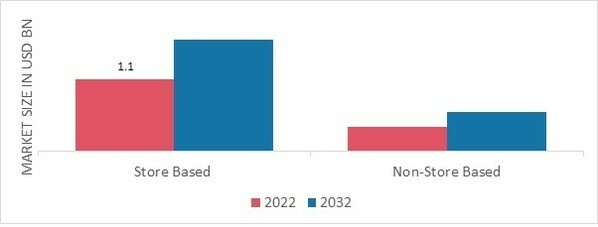

What distribution channel is expected to generate more revenue in the Gluten-free Bakery Market?

The Store-based distribution channel is expected to generate more revenue, with a range from 0.88 to 1.44 USD Billion.

What is the valuation range for Cakes & Cheesecakes in the market?

Cakes & Cheesecakes have a valuation range from 0.3 to 0.5 USD Billion.

How does the valuation of Muffins & Cupcakes compare to Sandwiches & Wraps?

Muffins & Cupcakes are valued between 0.2 and 0.35 USD Billion, while Sandwiches & Wraps range from 0.2 to 0.3 USD Billion.

What is the expected growth trend for the Gluten-free Bakery Market in the coming years?

The market is likely to experience steady growth, reaching 2.485 USD Billion by 2035, driven by a 4.9% CAGR.