Hyperlipidemia Drug Market Summary

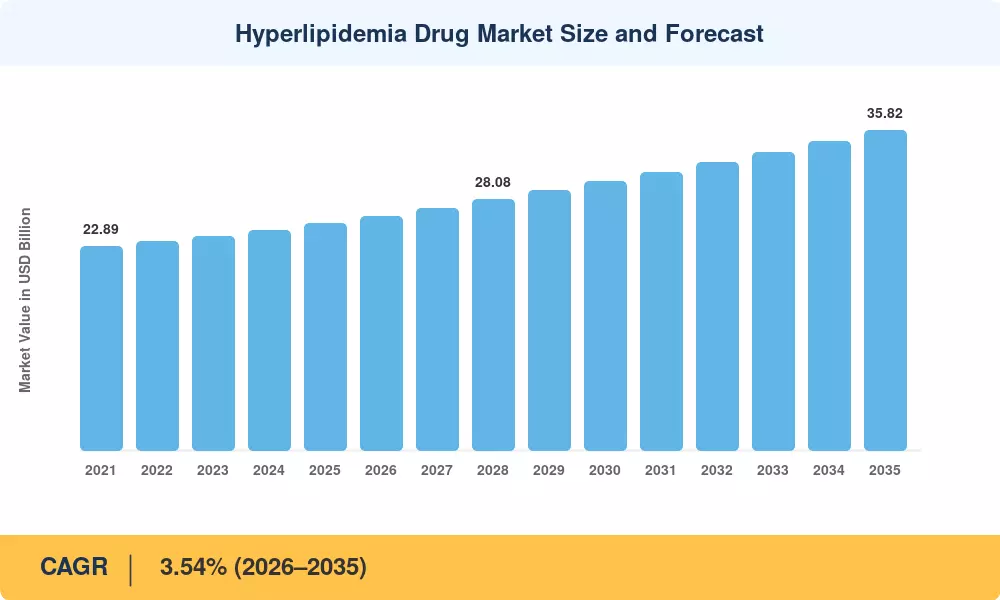

The Global Hyperlipidemia Drug Market size was valued at USD 25.38 Billion in 2025, and the market is projected to grow from USD 26.19 Billion in 2026 to USD 35.82 Billion by 2035, registering a CAGR of 3.54% during the forecast period 2026–2035. This growth trajectory reflects the expanding global burden of dyslipidemia—now affecting more than 2.1 billion adults—and sustained clinical emphasis on aggressive lipid management to prevent atherosclerotic cardiovascular events [1]. Updated ACC/AHA and ESC/EAS treatment guidelines continue to lower recommended LDL-C thresholds, pushing payer systems toward broader coverage of branded and biologic lipid-lowering therapies even as generic statins dominate volume prescriptions [2].

The market for hyperlipidemia drugs is changing due to a significant therapeutic shift. While still the mainstay of first-line therapy, injectable PCSK9 inhibitors, small-interfering RNA medicines like inclisiran, and adenosine triphosphate citrate lyase inhibitors like bempedoic acid are increasingly sharing formulary space with legacy oral statins. This change is reflected in investment activity: industry transaction records show that between 2022 and 2024, the total amount of venture and pharmaceutical license deals aimed at next-generation lipid modulators exceeded USD 4.7 billion [3]. Time-to-market for a number of pipeline candidates has been hastened by regulatory incentives, such as FDA Breakthrough Therapy designations for innovative mechanisms [4].

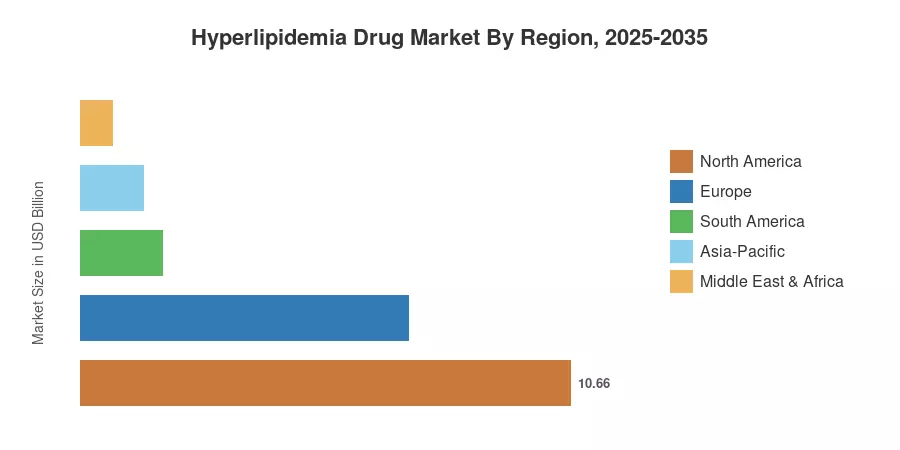

With strong payer reimbursement, specialty pharmacy infrastructure, and high diagnosis rates, North America holds around 42% of the hyperlipidemia drug market. With a predicted 5.4% CAGR through 2035, Asia-Pacific is the fastest-growing region thanks to government-led screening initiatives in China, India, and Southeast Asia. Europe has the second-largest share, at about 28%, thanks to outcomes-based contracting in Germany, France, and the UK, as well as unified EMA approvals [5]. The hyperlipidemia drug market is expected to develop steadily but fundamentally as real-world evidence programs redefine prescribing standards and patent cliffs speed up the introduction of biosimilars.

Key Report Takeaways

• By Drug Class

- Statins accounted for 72.5% of the Hyperlipidemia Drug Market share in 2025, sustained by entrenched guideline recommendations and low-cost generic availability.

- PCSK9 inhibitors are forecast to expand at a 4.0% CAGR through 2035, driven by label expansions and improving net pricing from outcomes-based agreements.

• By Route of Administration

- Oral formulations represented 60.6% of the Hyperlipidemia Drug Market in 2025, reflecting the dominance of statin and ezetimibe prescriptions.

- Parenteral delivery is growing at a 4.8% CAGR, propelled by the adoption of injectable biologics and semi-annual siRNA dosing regimens.

• By Distribution Channel

- Retail pharmacies captured 45.8% of revenue in 2025, remaining the primary dispensing point for chronic oral therapies.

- Online pharmacies exhibit the highest channel CAGR at 5.2%, reflecting digital health platform expansion and mail-order convenience.

• By Region

- North America contributed approximately 42.0% of the Hyperlipidemia Drug Market revenue in 2025.

- Asia-Pacific is set to register a 5.4% CAGR through 2035, the fastest among all regions.

Hyperlipidemia Drug Market Size and Forecast (2021–2035)

Market sizing draws on prescription audit databases, payer reimbursement records, company revenue disclosures, and proprietary econometric modeling calibrated to WHO and national health registry prevalence data [6]. Historical figures (2021–2024) are derived from audited sources; 2025 is the base year; and 2026–2035 values are forecast projections.