全球模内标签市场概览

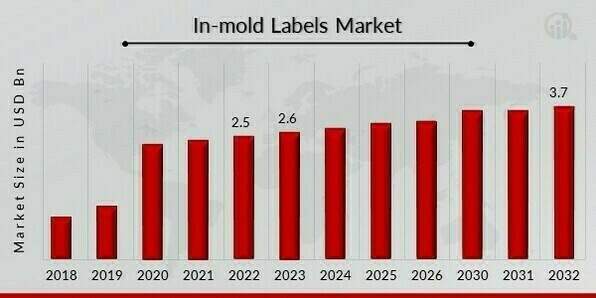

2023 年,全球模内标签市场规模预计为 26 亿美元。模内标签行业预计将从 2024 年的 27.2 亿美元增长到 2032 年的 37 亿美元,在预测期内(2024 年 - 2032 年)复合年增长率 (CAGR) 为 3.94%。模内标签提供了环保的解决方案,因为它们不需要额外的标签供应或程序,从而减少浪费和提高环境可持续性,是促进市场增长的关键市场驱动力。

来源:二次研究、初步研究、MRFR 数据库和分析师评论

模内标签市场趋势

-

对具有吸引力和视觉吸引力的包装解决方案的需求不断增长,推动市场增长

由于其生产视觉美观包装的能力,市场复合年增长率将会增加。模内标签(IML)在这一领域经历了大幅增长。模内标签在制造过程中集成到包装中,这与涉及在包装上单独粘贴标签的传统技术不同。这种集成使得精确、无缝地粘贴标签成为可能,从而创造出抛光的外观。模内标签能够接受复杂而详细的设计是其主要优点之一。高分辨率的设计、鲜艳的色彩,甚至金属或压花饰面等独特效果都可以打印在标签上。凭借这种程度的个性化和设计自由度,品牌可以在商店货架上区分其商品,吸引顾客的注意力,并有效地传达其品牌信息。

模内标签还具有无缝外观,因为它们是永久性包装组件。由于无需额外的粘合剂或标签材料,包装设计简单、整洁。没有明显的边框或重叠的标签提高了产品的整体美感并赋予其优质的外观。除了美观之外,模内标签还具有额外的实用优势。它们使用寿命长,耐化学物质、防潮和耐磨。由于其韧性,即使在冷藏或液体暴露等不利条件下,标签也能保证产品的使用。通过保持产品徽标和关键细节(例如成分或使用说明)清晰可见且完整,可以改善整体客户体验。在食品和饮料、个人护理和化妆品等行业,对有吸引力的包装解决方案的需求很高。这些行业在很大程度上依靠审美吸引力来吸引客户并提升良好的产品印象。模内标签提供色彩缤纷且有吸引力的包装替代方案,可提高品牌识别度和客户吸引力,使其成为这些行业的完美答案。此外,电子商务的发展增加了对美观包装的需求。随着越来越多的货物直接送到客户家门口,包装通常是公司与消费者之间的最初物理接触点。企业可以使用模内标签提供难忘的拆包体验,从而提高品牌忠诚度。

总体而言,对创新且美观的包装解决方案的需求不断增长,极大地推动了模内标签市场的发展。模内标签集美学吸引力、坚固性和实用优势于一体,可满足品牌和客户不断变化的需求。随着越来越多的公司意识到包装作为战术营销工具的价值,预计模内标签将在未来几年继续流行。因此,推动了模内标签市场收入。

2020 年 12 月,为消费者提供可持续包装解决方案的全球供应商 Huhtamaki 宣布在俄罗斯投资以实现进一步增长。为此,该公司计划在其阿拉布加工厂(鞑靼斯坦共和国)建设一座新的纤维包装制造工厂,以应对东部和东部地区零售业务和鸡蛋包装行业的快速发展。俄罗斯中部地区。

模内标签细分市场洞察

模内标签技术见解

全球模内标签市场细分基于技术,包括挤出吹塑、注塑和热成型。注塑成型类别是与模内标签市场最常相关的项目。在注射成型过程中,熔融塑料被注入模具型腔,硬化后形成所需的形状。将模内标签无缝集成到注塑成型过程中,可实现快速、准确的产品贴标。由于其适应性强、产量高以及生产复杂形状的能力,该技术被广泛应用于各个领域。它是模内贴标应用的首选。

模内标签材料见解

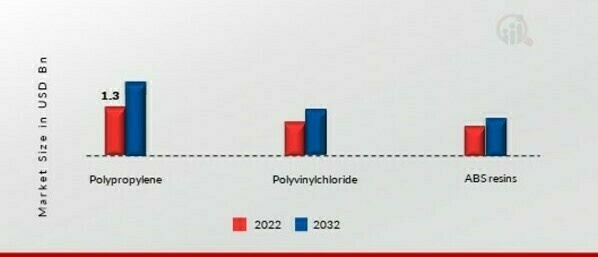

全球模内标签市场细分基于材料,包括聚丙烯、聚氯乙烯和 ABS 树脂。一种称为聚丙烯的热塑性聚合物以其卓越的品质而闻名,包括韧性、适应性和耐化学性。由于其与不同印刷工艺的兼容性以及与油墨和粘合剂形成牢固结合的能力,它经常用于模内标签应用。聚丙烯的适应性使其成为食品和饮料、家居用品和个人护理等行业包装的热门选择,因为它可以在模内标签上实现生动耐用的图像。

图 1:2022 年和 2022 年全球模内标签市场(按材料划分) 2032(十亿美元)

资料来源:二次研究、初步研究、MRFR 数据库和分析师评论

模内标签应用见解

全球模内标签市场细分基于应用,包括食品和饮料。饮料、化学品、个人护理品和消费品。食物饮料行业使用模内标签,因为它们可以生产美观的包装、提供重要的产品信息并保证法律合规性。模内标签适用于各种食品和饮料商品,因为它们持久、防潮且能承受各种温度。在这个竞争激烈的市场中,标签可以提高品牌认知度、区分商店货架上的产品并提高消费者满意度。

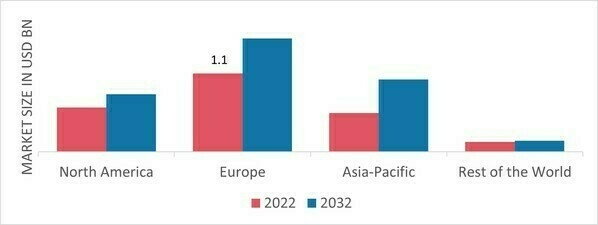

模内标签区域见解

按地区划分,该研究提供了北美、欧洲、亚太地区和世界其他地区的市场洞察。欧洲的包装行业十分完善,并以其高设计、可持续性和产品质量标准而闻名。该地区的特点是模内标签技术的采用率很高,并且模内标签市场上有大量重要参与者。模内标签非常适合欧洲国家流行的环保包装运动。该地区强大的制造基础、对创新的重视以及宽松的监管框架促进了模内标签在欧洲的广泛使用和发展。

此外,市场报告研究的主要国家包括美国、加拿大、德国、法国、英国、意大利、西班牙、中国、日本、印度、澳大利亚、韩国和巴西。

图 2:2022 年全球模内标签市场份额(按地区)(十亿美元)

资料来源:二次研究、初步研究、MRFR 数据库和分析师评论

北美模内标签市场占据第二大市场份额。由于食品和饮料、个人护理和汽车等行业的主导地位、对创意包装解决方案的关注以及对具有视觉吸引力和持久标签以改善产品品牌和消费者体验的需求等因素,北美成为模内标签市场第二重要的地区。 此外,英国模内标签市场占有最大的市场份额,加拿大模内标签市场是该地区增长最快的市场。

预计 2023 年至 2032 年,亚太地区模内标签市场将以最快的复合年增长率增长。亚太地区拥有强大的制造业,其中中国、日本和韩国在生产方面处于领先地位。由于快速的城市化、可支配收入的增加以及对产品品牌的高度重视,模内标签存在着相当大的市场。此外,中国模内标签市场占有最大的市场份额,印度模内标签市场是亚太地区增长最快的市场。

模内标签主要市场参与者和主要市场参与者竞争洞察

领先的市场参与者预计将在预测期内通过扩大销售和收入方面的足迹实现大幅增长。市场参与者还开展各种战略活动,以扩大其全球足迹,重要的市场发展包括新技术发布、合同协议、并购、增加投资以及与其他组织的合作。模内标签行业的市场参与者将通过增加对本地和区域产能的投资来进一步提高产能。

全球模内标签行业的知名制造商正在通过大力投资增加其容量来扩大其足迹。在预测期内,全球模内标签行业的成果将发生令人难以置信的变化。模内标签市场的主要参与者包括 CCL Industries Inc.(加拿大)、Constantia Flexibles Group GmbH(奥地利)、Huhtamaki Group(芬兰)和 Coveris Holdings S.A.(卢森堡),试图通过投资研发业务来增加市场需求。

CCL Sectors Inc. 是特种标签和包装解决方案领域的领导者,为全球众多行业提供尖端的产品和服务。 CCL Industries 是一家加拿大公司,其公司办事处位于多伦多。通过其众多的子公司和部门,它为 40 多个不同国家的客户提供服务。 CCL Industries 成立于 1951 年,现已发展成为一家在标签和包装领域具有重要地位的国际组织。压敏标签、收缩套管、模内标签、软包装、促销和保健品以及专用薄膜都是该公司广泛产品的一部分。 CCL Industries 支持的众多行业包括消费品、医疗保健、汽车、电子、个人护理、食品和饮料以及其他行业。由于公司拥有丰富的专业知识,因此可以提供符合最高质量标准的专业解决方案,同时满足特定的要求各行业的包装要求。

全球领先的包装和涂料公司 Coveris Holdings S.A. 专门为各行业提供尖端解决方案。 Coveris 为欧洲、美洲和亚洲的 40 多个地点提供服务,其全球总部位于卢森堡。自 2013 年成立以来,Coveris 迅速崛起,成为包装行业的重要参与者。该公司提供多种包装材料,包括硬容器、标签、技术薄膜和软包装。 Coveris 为各个行业提供服务,包括食品和饮料、医疗、农业、个人护理和工业市场。为了创建满足每个客户特定要求的定制包装解决方案,Coveris 非常强调开发以客户为中心的解决方案。该公司提供一流、实用且环保的包装解决方案,可保护产品完整性、提高货架吸引力并促进品牌成功。

SABIC 于 2023 年 9 月与三位专家联手:迪拜电影提供商 Taghleef Industries Group;希腊印刷专家 Stephanos Karydakis IML S.A.;以及注塑商 Kotronis Packaging。此次合作将展示可再生认证聚丙烯 (PP) 树脂在高质量单聚丙烯薄壁容器包装中的应用。在这种情况下,单步 IML 技术用于在注塑模具中实现无缝部件装饰,其中标签成为包装主体的一部分。

模内标签市场的主要公司包括

- CCL Industries Inc.(加拿大)

- Constantia Flexibles Group GmbH(奥地利)

- Huhtamaki 集团(芬兰)

- Coveris Holdings S.A.(卢森堡)

- Cenveo Inc.(美国)

- 富士密封国际公司。 (日本)

- Multicolor Corporation(美国)

- EVCO Plastics(美国)

- Innovia Films Ltd.(英国)

- Mepco 标签系统(美国)

- 艾利丹尼森公司(美国)

- Century Label Inc.(美国)

- 艾伦塑胶(台湾)

模内标签行业发展

CCL Industries 于 2023 年 7 月完成了一项收购交易,收购了总部位于阿利坎特、专门从事模具标签(“IML”)制造的 Creaprint S.L.。

Sonoco 开发新产品并投资生产线,以提供高品质、独特的 IML 产品,这些产品于 2023 年 3 月在 Interpack 2023 上进行了展示。

Cosmo Films 于 2019 年 9 月推出了各种由高抗撕裂聚丙烯薄膜制成的合成纸,用于可重新定位和可移除的标签应用、哑光涂层压敏标签纸薄膜、透明模内标签薄膜;高速WAL薄膜;以及珠光/金属化 WAL 薄膜。这表明模内标签市场可能会在预测期内扩大。

CCL Industries Inc. 旗下的 Innovia Films 挤出工厂宣布计划于 2020 年 11 月在波兰普沃茨克进行新产能投资。为了生产 EcoFloat 收缩套管材料,将安装一条新的 6 米多层共挤出生产线。

总部位于科罗拉多州柯林斯堡的 Muller Technology Colorado 透露,该公司将于 2020 年 3 月推出 M-Line 机器人。通过将机器人与自动化集成,整个机器人系统在进行注塑包装时提供了更大的自由度和范围。

2024 年:CCL Industries 推出了新型模内标签,具有更高的耐用性和包装应用的定制选项。

2023 年:Sappi Lanaken 推出了具有增强性能和环保材料的创新模内标签。

模内标签市场细分

模内标签技术展望

模内标签材料展望

模内标签应用展望

模内标签区域展望

- 北美

- 欧洲

- 亚太地区

- 中国

- 日本

- 印度

- 澳大利亚

- 韩国

- 澳大利亚

- 亚太地区其他地区

- 世界其他地区