Poultry Diagnostics Market Summary

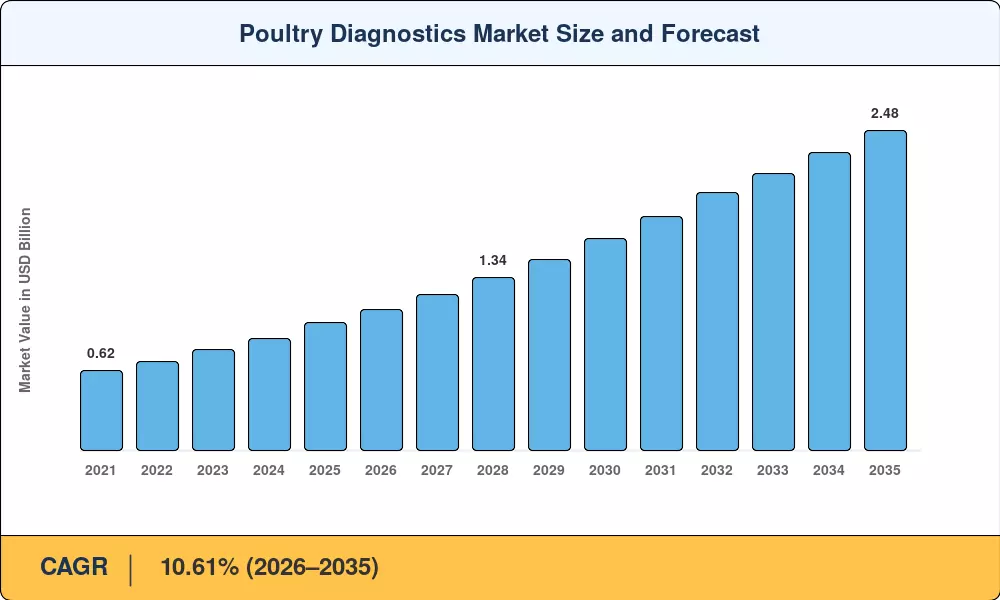

The Global Poultry Diagnostics Market size was valued at USD 0.99 Billion in 2025, and the market is projected to grow from USD 1.09 Billion in 2026 to USD 2.48 Billion by 2035, registering a CAGR of 10.61% during the forecast period 2026–2035. Successive waves of highly pathogenic avian influenza (HPAI) across North America and Europe have forced governments to mandate flock-level surveillance before granting export certificates, creating a regulatory floor beneath testing volumes. Integrated poultry producers now treat avian disease testing as a non-negotiable cost of doing business rather than an optional quality layer.

The industry is changing due to a technological revolution. Portable veterinary PCR for birds systems and AI-enabled hatchery analytics that may identify Newcastle disease diagnosis abnormalities in real time are replacing legacy serology-based procedures that needed centralized veterinary reference laboratories and multi-day turnaround [2]. While the EU's revised Animal Health Law requires recorded chicken pathogen detection for all flocks entering intra-community trade, the USDA's 2024 pledge of USD 1.3 billion to animal-disease preparedness programs has sped up the deployment of molecular instruments at the farm gate [3].

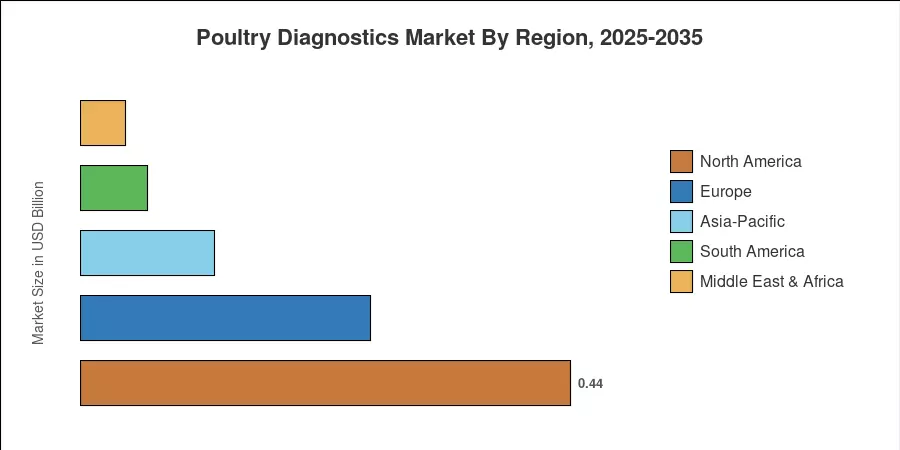

Due to strict NPIP (National Poultry Improvement Plan) testing regulations and extensive broiler integration, North America accounts for about 44% of global income. With a predicted 12.36% CAGR, Asia-Pacific is the fastest-growing market due to the quick industrialization of chicken production in China, India, and ASEAN countries. At roughly 26%, Europe has the second-largest share, and stricter biosecurity regulations maintain the bloc's demand for chicken flock health monitoring As trade compliance demands and disease complexity increase through 2035, the poultry diagnostics market is expected to grow at a steady double-digit rate.

Key Report Takeaways

• By Test Type

- ELISA-based assays captured the leading revenue position in the poultry diagnostics market during 2025, reflecting their entrenched role in large-scale serological screening programs

- PCR platforms are forecast to register the strongest CAGR through 2035 as veterinary PCR for birds gains regulatory preference for confirmatory testing of emerging viral strains

• By Disease Type

- Infectious diseases represented the largest disease-segment share in the poultry diagnostics market in 2025, driven by recurrent HPAI and Marek's disease outbreaks

- Parasitic diseases are on track for the fastest segment growth rate, propelled by rising coccidiosis screening in antibiotic-free production systems

• By Service Type

- Bacteriology services led the poultry diagnostics market by service revenue in 2025, supported by Salmonella and Mycoplasma monitoring mandates

- Virology services are positioned to expand most rapidly as avian disease testing demand shifts toward real-time influenza subtyping

• By End User

- Veterinary reference laboratories accounted for the dominant end-user share in the poultry diagnostics market in 2025

- On-farm point-of-care units record the highest end-user CAGR as portable chicken pathogen detection devices reach price points accessible to mid-scale producers

• By Regional

- North America held the largest regional revenue share in 2025, with the US accounting for the majority of testing expenditure

- Asia-Pacific is the fastest-growing region in the poultry diagnostics market, fueled by government-backed poultry flock health screening programs in India and China

Market Size and Forecast (2021–2035)

MRFR's market sizing relies on a bottom-up revenue model combining diagnostic kit shipment data, laboratory service revenues, and end-user procurement surveys across 32 countries.