Veterinary Medicine Market Summary

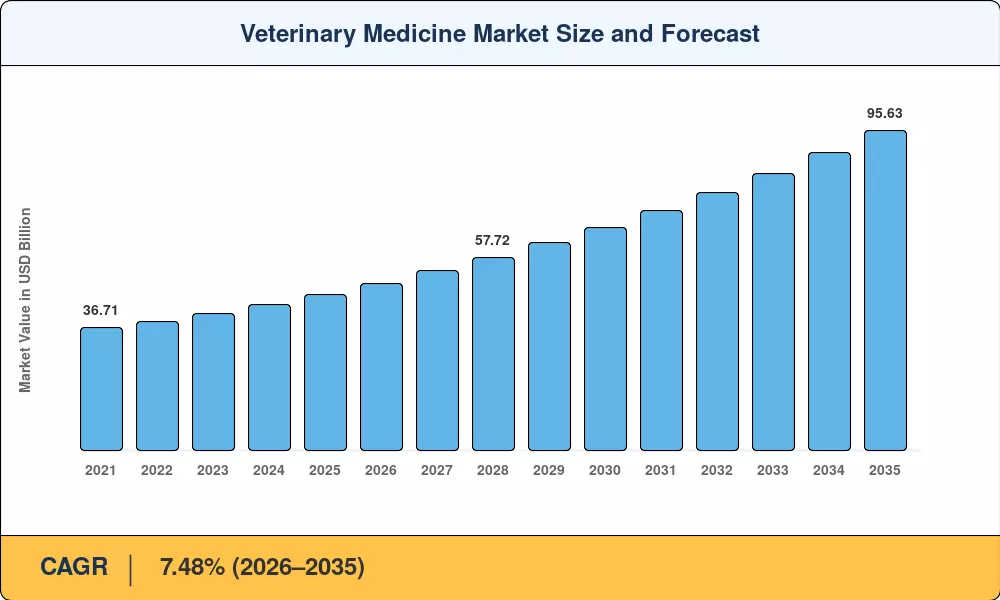

The Global Veterinary Medicine Market size was valued at USD 46.48 Billion in 2025, and the market is projected to grow from USD 49.96 Billion in 2026 to USD 95.63 Billion by 2035, registering a CAGR of 7.48% during the forecast period 2026–2035. Rising global expenditure on animal disease treatment — driven by one-health policy alignment and antibiotic stewardship regulations such as the FDA's Guidance for Industry #263 and the EU Veterinary Medicinal Products Regulation 2019/6 — is accelerating demand for vaccines, biologics, and next-generation parasiticides[2].

A pronounced technology shift is reshaping the Veterinary Medicine Market as legacy small-molecule generics cede ground to recombinant platforms, monoclonal antibody therapies, and gene-edited vaccines. Venture capital deployed into companion animal pharmaceuticals exceeded USD 2.8 billion globally in 2024, reflecting investor conviction that biologics — which carry gross margins of 40–60% versus 20–30% for generics — will anchor the next innovation cycle[4]. E-pharmacy channels, still at roughly 13% penetration, are widening owner access to chronic-care prescriptions for pet health medications and reducing dispensing friction.

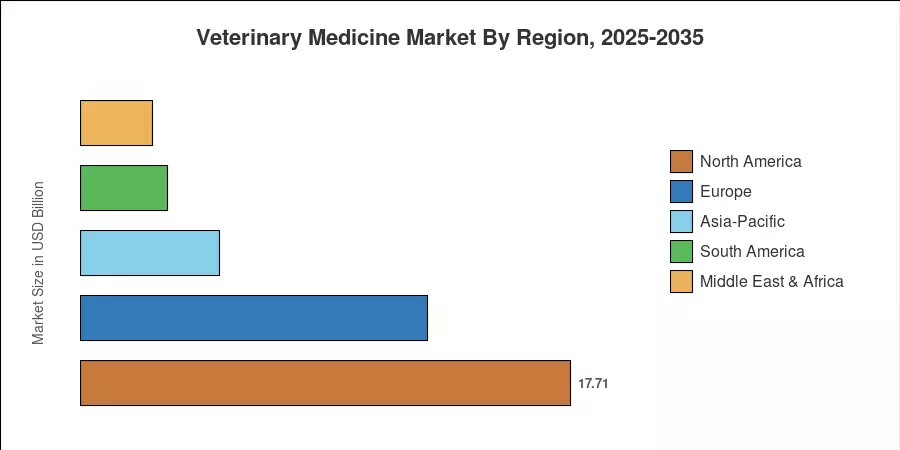

North America commanded approximately 38.1% of 2025 revenue, anchored by the United States' USD 36 billion companion-animal care economy. Asia-Pacific is the fastest-growing region with a projected 10.80% CAGR, propelled by surging pet adoption in China and India and industrialized livestock veterinary care across Southeast Asia. Europe holds the second-largest share at roughly 27.0%, with tightening antimicrobial-use directives fueling demand for vaccines over antibiotics

Key Report Takeaways

• By Product Type

- Drugs held a 52.5% revenue share of the Veterinary Medicine Market in 2025, supported by broad-spectrum anti-infectives and parasiticides

- Vaccines are projected to advance at a 9.70% CAGR through 2035, driven by recombinant and mRNA platform adoption

• By Animal Type

- Companion animals accounted for 51.5% of 2025 spending in the Veterinary Medicine Market, reflecting the premiumization of pet health medications

- Livestock treatments are projected to grow at an 11.24% CAGR through 2035, led by poultry and swine biologics

• By Region

- North America represented 38.1% of the 2025 Veterinary Medicine Market, led by the United States' advanced animal clinical diagnosis infrastructure

- Asia-Pacific is forecast to post a 10.80% CAGR from 2026 to 2035, the fastest among all regions

Veterinary Medicine Market Size and Forecast (2021–2035)

Market sizing integrates primary interviews with 120+ veterinary supply-chain stakeholders, secondary data from regulatory filings and trade associations, and proprietary bottom-up revenue modeling validated against company disclosures.