Surfactants Market Summary

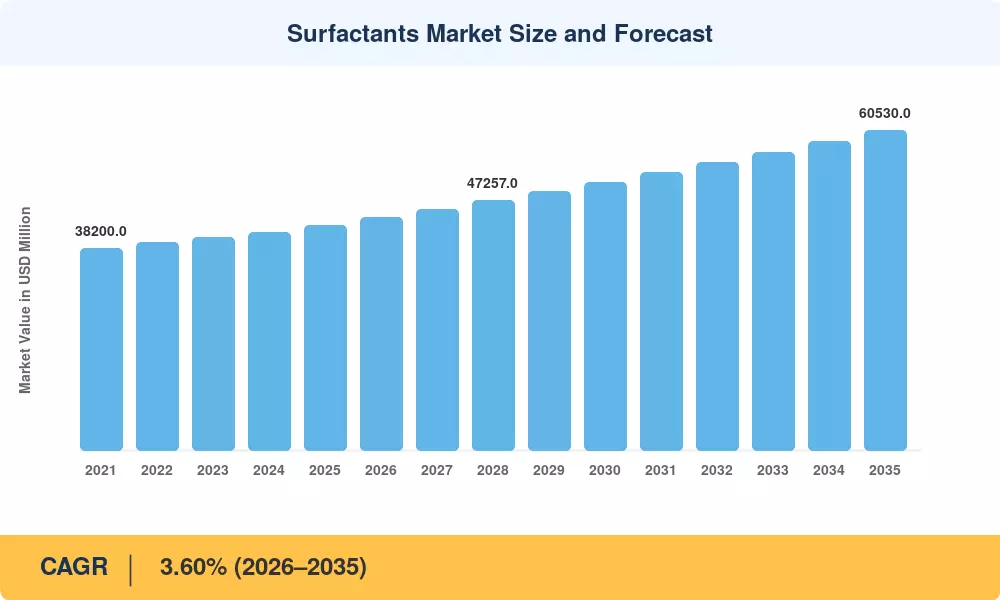

The global Surfactants Market reached an estimated USD 42,500 Million in 2025 and is projected to grow from USD 44,030 Million in 2026 to USD 60,530 Million by 2035, registering a compound annual growth rate of 3.60% during the forecast period. This expansion reflects rising demand across household cleaning, personal hygiene, and industrial process applications, underpinned by tightening sustainability regulations in the European Union and North America that are pushing formulators toward greener chemistries. The EU's revised Detergents Regulation and the U.S. EPA's Safer Choice program have accelerated reformulation timelines, creating a sustained pull for compliant raw materials [1].

A significant technology shift is reshaping the Surfactants Market as conventional petroleum-derived formulations give way to bio-based and enzymatic alternatives. Global investment in oleochemical refining capacity exceeded USD 2.8 billion between 2022 and 2024, with Southeast Asian palm-kernel and coconut-oil processing hubs attracting the largest share of capital [2]. Cold-water detergent platforms now account for a growing slice of laundry product launches in Europe, reducing energy intensity per wash cycle by roughly 30% and demanding surfactant architectures that perform effectively at temperatures below 30 °C [3].

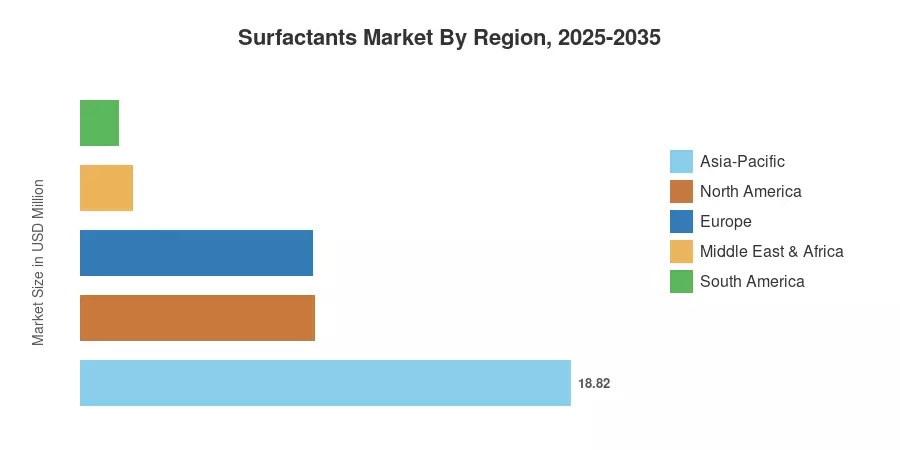

Asia-Pacific commands the largest share of the Surfactants Market at approximately 44.8% of global revenue in 2025, driven by population-scale consumption in China and India. The region is also the fastest-growing, with an anticipated CAGR of 4.60% through 2035 as urbanization and rising disposable incomes lift per-capita cleaning-product expenditure. Europe holds the second-largest position at around 21.2% share, anchored by mature personal-care and institutional-cleaning verticals. North America contributes roughly 22.5%, supported by strong industrial and oilfield-service demand. These regional dynamics will continue to shape competitive positioning and capacity-investment decisions across the next decade.

Key Report Takeaways

• By Type

- Anionic surfactants accounted for approximately 44.2% of the global Surfactants Market share in 2025, underpinned by their dominant role in household and industrial cleaning formulations.

- Amphoteric surfactants are forecast to grow at the fastest pace through 2035, reflecting rising demand in mild personal-care and baby-product segments.

- Cationic surfactants generated approximately USD 5,100 Million in 2025, driven by fabric-softener and hair-conditioning applications.

• By Application

- Household soap and detergent applications represented roughly 46.3% of the Surfactants Market revenue in 2025, reinforcing the category's position as the single largest demand pool.

- Personal-care product applications are expected to register the highest CAGR of 5.00% through 2035, supported by premiumization trends in skincare and haircare.

• By Region

- Asia-Pacific led the Surfactants Market with a 44.8% revenue share in 2025 and is projected to maintain the fastest regional growth trajectory through 2035.

- North America contributed approximately USD 9,560 Million in 2025, with oilfield-chemicals and institutional-cleaning segments providing additional demand resilience.

Market Size and Forecast (2021–2035)

Market Research Future's proprietary estimation framework integrates primary interviews with surfactant producers and downstream formulators, secondary data from trade associations (CESIO, SDA, ICIS), and import-export databases to construct historical baselines and calibrate forward projections. Forecast-period values reflect a constant 3.60% CAGR applied uniformly, with qualitative adjustments noted for years affected by raw-material price shocks or pandemic-era demand anomalies.