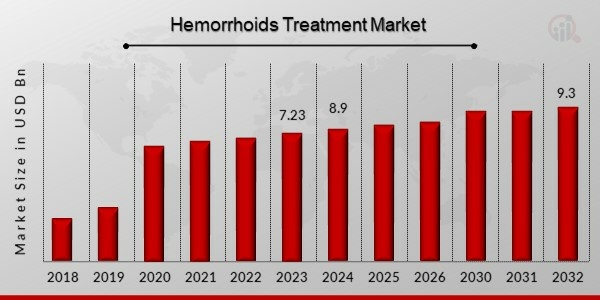

What is the projected market valuation of the Hemorrhoids Treatment Market by 2035?

The projected market valuation for the Hemorrhoids Treatment Market is 2994.6 USD Million by 2035.

What was the market valuation of the market in 2024?

The overall market valuation of the market was 1441.59 USD Million in 2024.

What is the expected CAGR for the Hemorrhoids Treatment Market during the forecast period 2025 - 2035?

The expected CAGR for the Hemorrhoids Treatment Market during the forecast period 2025 - 2035 is 6.83%.

Which treatment type segment had the highest valuation in 2024?

The Minimally Invasive Procedures segment had the highest valuation at 450.0 USD Million in 2024.

How do the valuations of oral medications compare to topical treatments in 2024?

In 2024, oral medications were valued at 250.0 USD Million, whereas topical treatments were valued at 300.0 USD Million.

What demographic segment is expected to have the highest market valuation by 2035?

The Adults demographic segment is expected to have the highest market valuation, projected at 1200.0 USD Million by 2035.

Which distribution channel is anticipated to dominate the Hemorrhoids Treatment Market by 2035?

Pharmacies are anticipated to dominate the Hemorrhoids Treatment Market, with a projected valuation of 1200.0 USD Million by 2035.

What was the valuation of surgical procedures in 2024?

The valuation of surgical procedures in 2024 was 441.59 USD Million.

Which key players are leading the Hemorrhoids Treatment Market?

Key players in the Hemorrhoids Treatment Market include Johnson & Johnson, Bayer AG, and Medtronic.

What is the projected valuation for the severe severity level segment by 2035?

The projected valuation for the severe severity level segment is 594.6 USD Million by 2035.