Menstrual Cup Market Summary

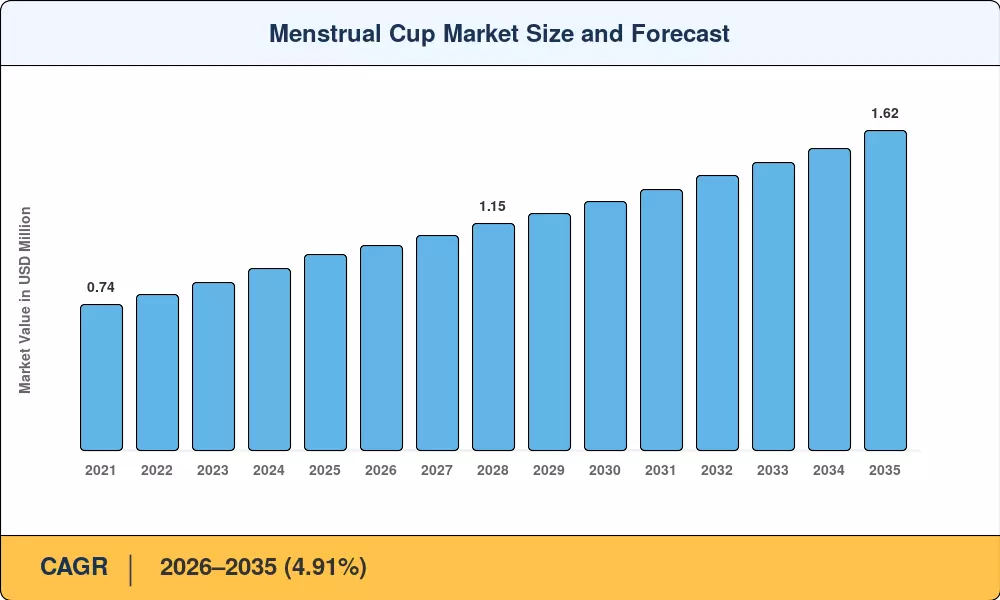

The Global Menstrual Cup Market size was valued at USD 0.99 Billion in 2025, and the market is projected to grow from USD 1.04 Billion in 2026 to USD 1.62 Billion by 2035, registering a CAGR of 4.91% during the forecast period 2026–2035. This expansion is anchored in a decisive consumer pivot toward reusable feminine hygiene products and growing government investment in period-poverty alleviation programs. Scotland's Period Products Act — the first national legislation guaranteeing free access to menstrual products — has catalyzed similar policy discussions across the EU and parts of Southeast Asia, lending structural support to demand for silicone period cup alternatives [2].

A generational shift away from single-use tampons and pads is reshaping the feminine hygiene landscape. Where disposable products once dominated shelf space unchallenged, eco-friendly period care options now command premium positioning in both brick-and-mortar pharmacies and digital storefronts. Environmental analyses consistently show menstrual flow collection devices cut lifecycle carbon emissions by roughly 85–90% compared to disposable counterparts, a data point that resonates with Gen Z and millennial consumers willing to pay upfront premiums for sustainability [3]. E-commerce platforms have simultaneously lowered the information barrier, offering sizing guides, instructional videos, and peer reviews that accelerate first-time adoption of the silicone period cup.

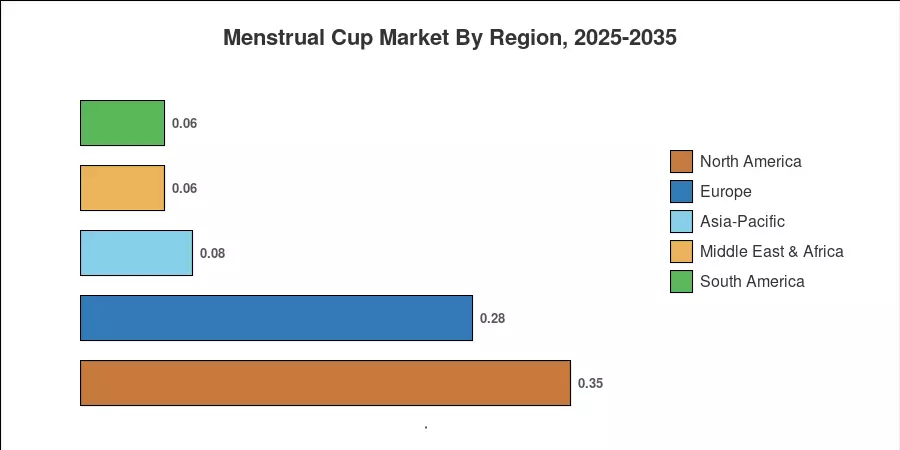

North America remains the dominant region in the Menstrual Cup Market, holding approximately 35.5% of global revenue in 2025, driven by mature retail infrastructure and strong DTC brand ecosystems. Asia-Pacific, however, is the fastest-growing region at a projected 8.1% CAGR through 2035, fueled by rising disposable incomes in India and China and government-backed menstrual health awareness campaigns Europe holds the second-largest share at roughly 28%, supported by stringent single-use plastics directives that favor reusable feminine hygiene adoption. The decade ahead will reward brands that combine material innovation with culturally sensitive education strategies.

Key Report Takeaways

• By Product Type

- Reusable menstrual cups commanded 48.7% of the Menstrual Cup Market in 2025, reflecting consumer preference for long-term cost savings and sustainability

- Disposable cups are forecast to expand at a 6.2% CAGR through 2035, attracting first-time users seeking a lower-commitment alternative to tampons

• By Material

- Medical-grade silicone dominated with 64.8% revenue share in 2025, backed by FDA and CE clearance and broad physician endorsement

- Thermoplastic elastomer (TPE) is projected to grow at a 6.6% CAGR, gaining traction among latex-sensitive consumers

• By Distribution Channel

- Online stores accounted for 41.8% of the Menstrual Cup Market size in 2025, powered by subscription models and influencer-driven education

- Pharmacies and retail stores remain critical for trial-driven purchases in emerging economies

• By Region

- North America led with 35.5% share in 2025, while Asia-Pacific is projected to grow at an 8.1% CAGR through 2035

- Europe's Menstrual Cup Market benefits from the EU Single-Use Plastics Directive, driving the adoption of alternatives to tampons

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s proprietary estimation framework combines primary interviews with OB-GYN professionals, gynecological device distributors, and e-commerce analytics, triangulated against trade-level import/export data and manufacturer revenue disclosures. Historical figures (2021–2024) reflect actual market performance; forecast figures (2026–2035) apply the calibrated 4.91% CAGR with adjustments for anticipated regulatory catalysts and material innovation cycles.