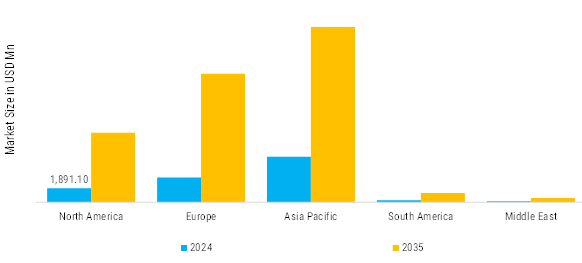

North America: Expanding EV charging sector

The North American EV charging sector is making strides with mega-partnerships and robust governmental backing. Vehicle manufacturers and power firms are leading large-scale development with interoperability and reliability in mind. General Motors and ChargePoint deploy hundreds of fast-charging centers with CCS and NACS compatibility, while Mercedes-Benz and Starbucks deploy high-speed charging along key highway segments. The joint venture of IONNA supported by BMW, GM, Toyota, Hyundai, and more envisions 30,000 dual-standard highway charging centers. In a similar vein, ChargePoint's joint venture with Eaton offers bi-directional and grid-integrated charging, while the joint venture of EV edged with AMPECO guarantees strong, software-centric uptime management.

Europe: Emerging EV charging sector

Europe is growing fast, supported by robust regulation, standardization, and investment in green infrastructure. The CCS2 connector is the common fast-charging standard on the majority of public stations, having replaced the previously ubiquitous CHAdeMO system employed by previous models such as the Nissan LEAF. On the AC charging front, Type 2 ports are the European standard, whereas GB/T chargers are seen very irregularly in markets that import Chinese EVs. Infrastructure growth across the continent is significant the ratio of EVs-to-public chargers is better at 13:1, compared to almost a 10% increase from 2023. Ultra-fast chargers (150 kW+) increased by 50% to a total of 71,000, equivalent to approximately 10% of all public chargers, with approximately 20% providing 350 kW or more capability, although very limited vehicle compatibility is possible with such speed levels.

Asia-Pacific: Development of EV charging sector

The Asia-Pacific is experiencing rapid development in smart EV charging, facilitated by favorable government policies, mass-scale public–private investments, and accelerated consumer uptake of electric vehicles. Regional governments are strongly incentivizing EV infrastructure development. In Thailand, the BEV 3.5 incentive program for the period of 2024–2027 aligns import and excise tax discounts with subsidies tied to battery capacity, with a aim of reaching more than 2,200 public fast chargers by 2025 and 12,000 by 2030. Vietnam is lining up electricity subsidies for charging companies and is concluding unified technologies standards to promote citywide and intercity network deployment.

Middle Eat & Africa: Emerging EV adoption

Middle East and Africa (MEA) is growing swiftly based on high incentive government initiatives, private investments, and increasing EV adoption in city centers. In the Middle East, nations like Saudi Arabia and UAE are leading infrastructure growth through large deployments like ABB's chargers across 100 sites of Saudi and Siemens' ultra-fast 160 kW chargers on UAE highways backed by clear national EV policies and green transition objectives. On the African continent, public charge points have increased by more than two times, with OEM-driven initiatives (Audi, BMW, Jaguar, Nissan) and private schemes growing ultra-fast DC grids.

South America: Emerging wind turbine

South America is maintaining steady strides in building its electric vehicle (EV) charging infrastructure, spurred on by government initiatives, private investment, and local assembly programs. Of them, Brazil is the regional leader, its energy firm WEG having initiated local assembly of EV chargers and set a course for shipping products to Europe, thereby marking a growing importance of South America to the global EV value chain. Chile and Colombia are also picking up speed, as they establish public EV charging corridors and ramp up direct current (DC) fast-charging grids across urban and intercity corridors by teaming up with companies like Enel X, Blink Charging, and Celsia.