The Reusable Beverage Packaging Market is a type of container and system that can be used multiple times to store, transport, and drink beverages. It replaces traditional single-use formats. Most of the time, these packages are made of strong materials like glass, stainless steel, high-quality reusable plastics, or new composites that can handle being cleaned, sanitized, and refilled repeatedly without affecting the safety or quality of the product. Reusable beverage packaging works in several reuse models such as closed-loop systems, brewery refill & collection, distribution center-based refill loops, deposit return schemes (DRS), retail refill stations, direct-to-consumer (D2C) return models, and event-based circular models that help in collecting, returning, and redistributing the packaging.

These systems are often encouraged through deposit-return schemes or membership models. Common types are reusable bottles, reusable kegs, reusable pouches, reusable cups and jugs, and transport and refill packaging that can be returned. These systems follow the rules for sustainability and the principles of a circular economy by extending the life of packaging. This means less raw material use, less waste, and less greenhouse gas emissions. Environmental rules, corporate commitments to sustainability, and rising consumer demand for eco-friendly packaging options are all factors that drive its adoption.

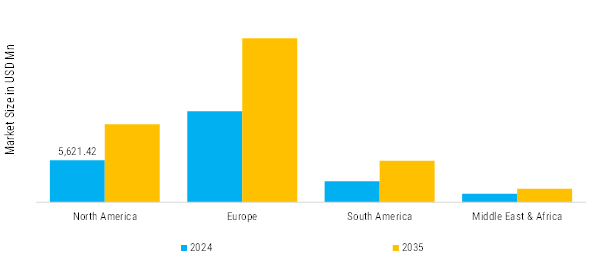

The Reusable Beverage Packaging Market is shaped by a combination of regulatory, environmental, technological, and consumer-driven factors. Regulatory requirements like Extended Producer Responsibility (EPR) laws, bans on single-use plastics, and deposit-return schemes are making beverage makers switch to reusable formats. Consumers want circular economic solutions that use fewer resources because they are worried about plastic waste and carbon emissions. Currently, consumers are becoming more eco-friendly when they shop, and younger people are especially open to refill and return systems. Corporate sustainability commitments are speeding up adoption because big beverage companies are setting measurable reuse goals to meet ESG goals. Also, new materials smart tracking (like RFID and QR codes) are making things more efficient, easier to track, and cheaper. But problems like high initial costs, limited infrastructure, and concerns about hygiene still affect market growth. For long-term success, innovation, collaboration, and education are all very important.

The market is segmented based on packaging types, including Reusable Bottles, Reusable Kegs, Reusable Pouches, Reusable Cups and Jugs, and Transport and Refill Packaging. It is also classified by Material Type, such as PET, and Composite or Multilayer Packaging (e.g., barrier-layer PET for carbonation retention). Additionally, in Beverage Type segmentation the market is divided into Beer, Carbonated Soft Drinks, Bottled Water, Juices, Wine and Spirits, Functional Drinks (e.g., Kombucha, Energy Drinks), and Others. Moreover, for end user Industry, market is segmented into Breweries (Craft and Commercial), Beverage Manufacturers (Soft Drinks, Juices, etc.), Wineries and Distilleries, Hospitality (Hotels, Restaurants, Cafes, Bars), Beverage Distributors, and Institutional Users (Airlines, Events, Stadiums). Based on Reuse Model, the market is segmented into Closed-Loop Systems, Brewery Refill & Collection, Distribution Center-Based Refill Loops, Deposit Return Schemes (DRS), Retail Refill Stations, Direct-to-Consumer (D2C) Return Models, and Event-Based Circular Models.