Market Summary

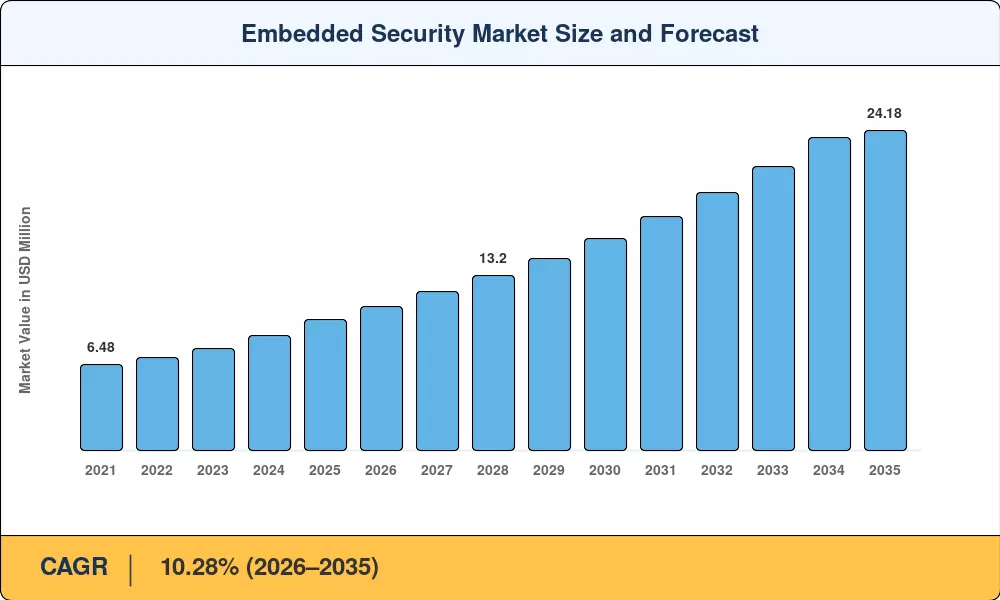

The embedded security market reached an estimated USD 9.92 billion in 2025 and is projected to grow from USD 10.86 billion in 2026 to USD 24.18 billion by 2035, advancing at a CAGR of 10.28% during the forecast period. Two regulatory catalysts have accelerated this trajectory: the European Union's Cyber Resilience Act, which mandates hardware root of trust for IoT devices across all connected products sold within the bloc, and UNECE Regulation 155, requiring secure boot and firmware signing for embedded systems in every new vehicle type-approved after mid-2024 [2][3]. Together, these policies have converted voluntary chip-level safeguards into non-negotiable design requirements.

A technology transformation is reshaping silicon architectures. Legacy software-only security stacks are giving way to integrated hardware security modules for IoT and ARM TrustZone for embedded security implementations baked directly into microcontrollers. Automotive electrification alone has tripled the electronic control unit count per vehicle, expanding both silicon content and the attack surface. Investment in cryptographic acceleration in embedded processors surpassed USD 1.4 billion globally in 2024, driven by enterprises migrating toward post-quantum cryptography readiness and FIDO2 passkey provisioning [4][5].

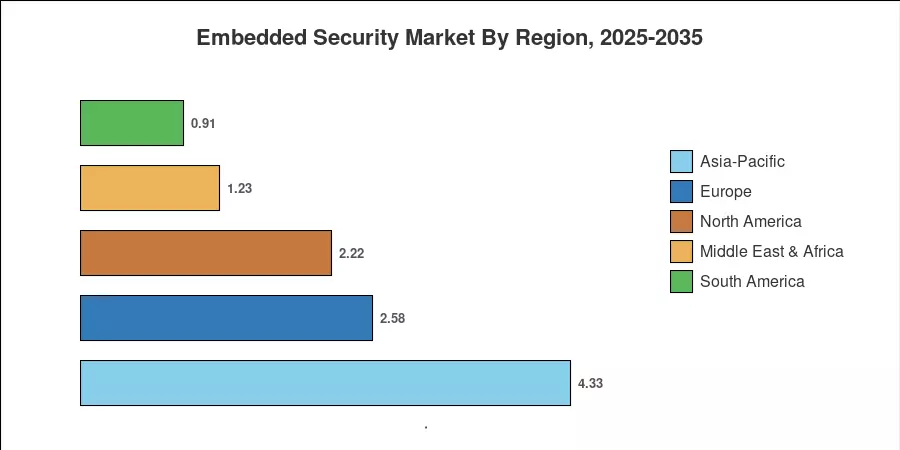

Asia-Pacific commands the dominant share of the embedded security market at approximately 43.6% of 2025 revenue, anchored by semiconductor fabrication capacity in Taiwan, South Korea, and mainland China. The Middle East & Africa region is the fastest-growing geography, registering a projected CAGR of 12.44% through 2035, propelled by smart-city initiatives in Saudi Arabia and the UAE Europe holds the second-largest share at roughly 26%, where regulatory mandates continue to drive embedded security market adoption across automotive and industrial verticals.

Key Report Takeaways

• By Component Type

- Hardware maintained a 53.1% share of the embedded security market in 2025, reflecting demand for secure elements, TPMs, and hardware security modules for IoT integration

- Services recorded the highest segment CAGR at 12.34% through 2035, driven by managed security provisioning and lifecycle firmware management

• By Deployment

- Cloud deployment led with USD 6.24 billion in 2025 revenue, as enterprises scaled elastic HSM instances for cryptographic acceleration in embedded processors

- On-premises deployment is growing at a 8.76% CAGR, fueled by data-localization statutes that require local secure element provisioning

• By Application

- Payment captured 39.4% of the embedded security market size in 2025, supported by eSIM provisioning and FIDO passkey rollouts

- Authentication is poised for an 11.49% CAGR to 2035 as secure boot and firmware signing for embedded systems becomes standard

• By End-User Industry

- Automotive held a 34.7% share of 2025 demand, where ARM TrustZone for embedded security underpins vehicle-to-everything communication

- Healthcare is forecast to expand at a CAGR of 11.02% between 2026 and 2035

• By Region

- Asia-Pacific commanded 43.6% of the global embedded security market revenue in 2025

- The Middle East & Africa is on track for the fastest regional CAGR of 12.44%