Drone Logistics Transportation Market Summary

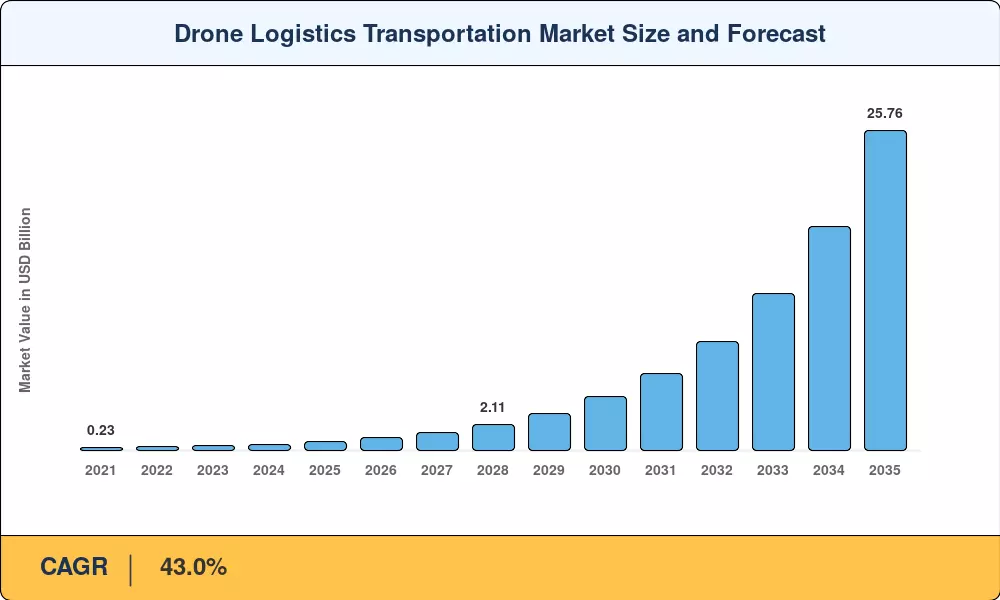

The Drone Logistics and Transportation Market was valued at USD 0.72 billion in 2025 and is projected to reach USD 25.76 billion by 2035, expanding at a 43.0% CAGR during the 2026–2035 forecast period. This trajectory reflects a structural shift driven by the FAA's updated Part 135 air carrier certification pathway for unmanned aircraft operators and the European Union Aviation Safety Agency's U-space regulatory framework, which together have unlocked commercial beyond-visual-line-of-sight corridors in over a dozen national markets [1][2]. The 2026 starting forecast value stands at USD 1.03 billion, marking the inflection point where pilot programs convert into revenue-generating route networks.

The growth of the drone logistics and transportation market is largely dependent on technological advancement. Decentralized drone sorting micro-depots located within five kilometers of final customers are replacing traditional ground-courier networks based on diesel vehicles and centralized distribution centers. Prototypes of lithium-sulfur cells now surpass 450 Wh/kg at the pack level, which is about double the energy density of traditional lithium-ion cells. This allows single-charge ranges with payloads weighing less than 5 kg to surpass 80 km [3]. In 2024, venture capital pledges to drone delivery start-ups exceeded USD 2.8 billion worldwide, indicating investor confidence that unit economics in tight urban corridors are getting close to parity with surface transit [4].

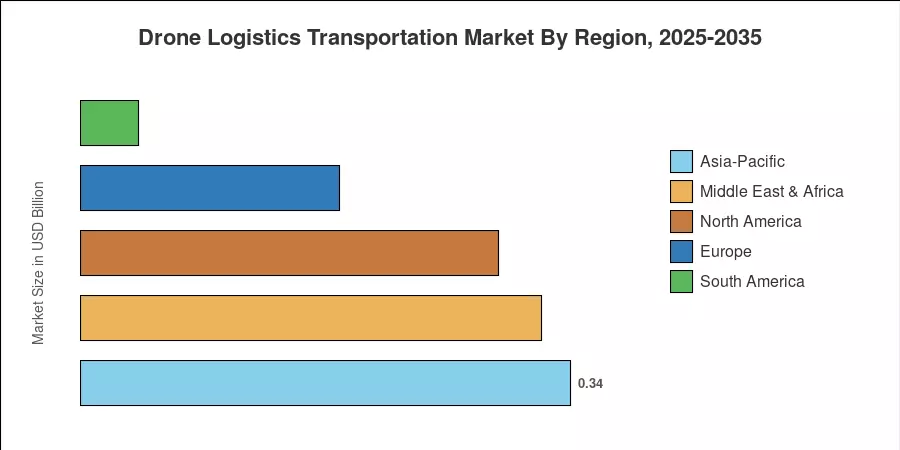

Thanks to early fleet deployments by tech-native operators and regulatory momentum in the US, North America holds 40.8% of the drone logistics and transportation market. Asia-Pacific is the fastest-growing region at a 47.2% CAGR, pushed by China's low-altitude economy plan and India's PLI-Drones scheme. Europe, led by France and Germany, has the second-largest proportion at over 24.5%. As airspace integration standards evolve and payload capabilities expand, the Drone Logistics and Transportation Market is poised to transform last-mile supply chains across both developed and emerging nations.

Key Report Takeaways

• By Service Type

- Drone-as-a-Service (DaaS) captured 45.1% of the Drone Logistics and Transportation Market in 2025, reflecting enterprise preference for capex-light fleet access.

- On-demand delivery services are advancing at a 45.6% CAGR through 2035, fueled by e-commerce fulfillment demand.

• By Application

- Retail and logistics held a 41.5% share of the Drone Logistics and Transportation Market in 2025, led by parcel and grocery fulfillment.

- Medical supply delivery is expanding at a 46.7% CAGR through 2035, driven by vaccine cold-chain requirements in underserved regions.

• By Payload Weight

- Consignments under 5 kg commanded 43.2% of the Drone Logistics and Transportation Market in 2025.

- Payload classes above 5 kg are projected to expand at a 44.3% CAGR to 2035.

• By Range

- Short-range flights carried 50.2% share in 2025, while long-range missions are forecast to grow at a 44.7% CAGR.

• By Geography

- North America led with 40.8% revenue share in 2025.

- Asia-Pacific is forecast to expand at a 47.2% CAGR through 2035.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology combines bottom-up operator revenue analysis with top-down validation against regulatory filings, disclosed delivery volumes, and venture funding disclosures. Historical figures (2021–2024) reflect actual commercial shipments and contracted DaaS revenues; forecast values (2026–2035) apply the calibrated 43.0% CAGR to the 2025 base, adjusted for anticipated regulatory phase-ins and payload-class expansion.