Battery Size

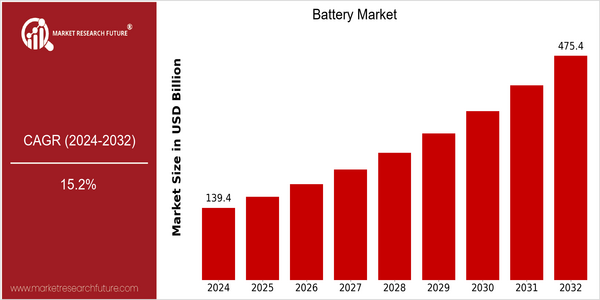

Market Size Snapshot

| Year | Value |

|---|---|

| 2024 | USD 139.36 Billion |

| 2032 | USD 475.37 Billion |

| CAGR (2024-2032) | 15.2 % |

Note – Market size depicts the revenue generated over the financial year

The market for batteries is expected to grow to an estimated $139.3 billion by 2024 and $475.3 billion by 2032. This remarkable growth translates into a compound annual growth rate (CAGR) of 15.2% for the forecast period. The increasing demand for energy storage, driven by the rise of electric vehicles, the integration of solar energy and the rise of mobile devices, is the main driver of this growth. The batteries are becoming an increasingly important part of the world's energy strategy. The technological development of batteries, such as the development of lithium-ion batteries and the improvement of lithium-ion batteries, is also driving market growth. The major players in the industry, such as Panasonic, Tesla and LG Chem, are also investing in research and development to improve the performance of batteries and reduce costs. Strategic initiatives, such as the establishment of joint ventures for battery recycling and the establishment of "big factories", are also shaping the industry. The goal of these efforts is to meet the increasing demand for batteries, but also to address the serious environmental issues caused by the production and use of batteries. , in order to ensure the sustainable development of the battery market.

Regional Market Size

Regional Deep Dive

The Battery Market is a multi-regional industry, characterized by the increasing demand for batteries for the production of electric vehicles, as well as for the production of electricity from renewable sources, and for the production of portable electronic devices. Each region has its own characteristics, which are determined by the local legal environment, technological development and economic situation. North America focuses on EVs and battery recycling, Europe is leading in terms of innovation and responsibility, Asia-Pacific is a manufacturing center with rapid technological development, the Middle East and Africa are interested in storing electricity from renewable sources, and Latin America is gradually investing in the development of battery technology.

Europe

- The European Union has set ambitious targets for reducing carbon emissions, leading to increased investments in battery technology and recycling, with companies like Northvolt and BASF spearheading innovative projects.

- The European Battery Alliance is fostering collaboration among key stakeholders, including governments and private companies, to create a competitive battery manufacturing ecosystem in Europe.

Asia Pacific

- China continues to dominate the battery market, with companies like CATL and BYD leading in lithium-ion battery production and innovations in solid-state batteries.

- Government initiatives in countries like Japan and South Korea are promoting research and development in battery technologies, particularly in enhancing energy density and reducing costs.

Latin America

- Brazil is increasing its focus on lithium extraction, with companies like Companhia Brasileira de Lítio working to supply the growing global demand for battery materials.

- Government programs in countries like Chile are promoting the development of sustainable mining practices for lithium, which is crucial for the battery supply chain.

North America

- The U.S. government has introduced incentives for EV purchases and investments in battery manufacturing, with companies like Tesla and General Motors ramping up production capabilities to meet growing demand.

- Recent regulatory changes, such as California's mandate for all new cars to be zero-emission by 2035, are pushing automakers to invest heavily in battery technology and infrastructure.

Middle East And Africa

- Countries like the UAE are investing in renewable energy projects, such as the Mohammed bin Rashid Al Maktoum Solar Park, which requires advanced battery storage solutions to manage energy supply.

- The African Development Bank is supporting initiatives to improve energy access through battery storage systems, particularly in off-grid and rural areas.

Did You Know?

“Did you know that lithium-ion batteries, which power most of today's portable electronics and electric vehicles, can lose up to 20% of their capacity in extreme temperatures?” — International Energy Agency (IEA)

Segmental Market Size

Lithium-ion batteries play a major role in the global market for batteries, which is currently growing rapidly, primarily because of the growing demand for electric vehicles and storage systems for solar and wind power. The demand for lithium-ion batteries is increasing because of the worldwide trend towards sustainable energy, the policy support for electric vehicles, and the technological progress in battery development, which is reducing the costs and improving the performance of batteries. There are a number of companies, such as Panasonic and Tesla, that are investing heavily in the development and production of batteries. Compared to Europe and North America, the market penetration of lithium-ion batteries is higher than in Asia. The main applications are electric vehicles, consumer electronics, and storage systems for solar and wind power. The growth of the market is being driven by the reduction in the use of fossil fuels and by the trend towards reducing the carbon footprint. The development of new battery systems, such as solid-state batteries and battery management systems, will also have an effect on the evolution of the market.

Future Outlook

The world market for batteries is expected to reach $475.4 billion by 2032, at a CAGR of 15.2%. This growth is mainly driven by the growing demand for electric vehicles, storage solutions for renewable energy and portable electronics. Governments are increasingly regulating emissions and promoting sustainable energy. This is driving the adoption of advanced batteries, resulting in greater penetration in the industrial and consumer sectors. The electric vehicle market is expected to account for more than 30% of the world's vehicle sales by 2032. This will drive a significant increase in the demand for high-capacity batteries. Meanwhile, technological advancements such as the development of lithium-sulfur batteries and improvements in lithium-ion technology are expected to increase the energy density, reduce charging time and prolong battery life. Meanwhile, the rise in battery recovery and reuse will help to establish a circular economy, which will also benefit market growth. The development of smart battery management systems and the expansion of charging stations will also play a critical role in the future development of the battery market. The combination of these factors will result in a rapidly evolving market that will offer lucrative opportunities to the entire value chain.

Leave a Comment