Ammunition Market Summary

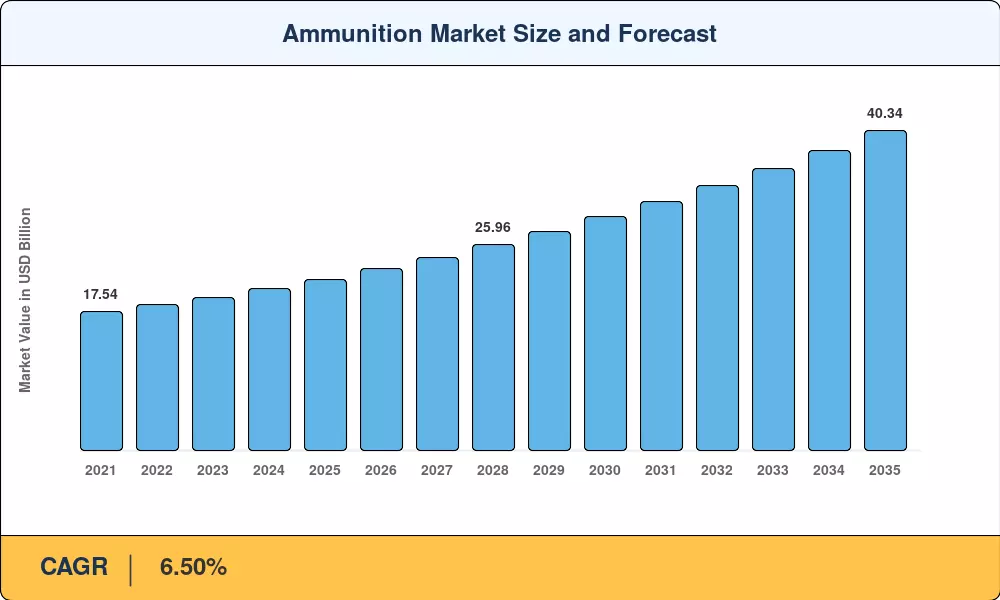

The global Ammunition Market reached an estimated USD 21.59 Billion in 2025 and is projected to climb to USD 22.89 Billion in 2026 before expanding to USD 40.34 Billion by 2035, registering a compound annual growth rate of 6.50% over the 2026–2035 forecast window. Two catalysts are propelling this trajectory: sustained U.S. Department of Defense multi-year procurement commitments exceeding USD 7.8 Billion annually for conventional munitions, and the European Union's Act in Support of Ammunition Production (ASAP), which channeled EUR 500 Million toward 155 mm shell capacity-building between 2023 and 2025 [4].

A pronounced technology transformation is reshaping the Ammunition Market as legacy unguided rounds give way to programmable air-burst munitions and precision-guided artillery. Rheinmetall's Assegai family and BAE Systems' Shaped Trajectory Projectile illustrate the shift, while the U.S. Army's Next Generation Squad Weapon program has accelerated adoption of 6.8 mm hybrid-case cartridges at an investment of over USD 4.7 Billion through 2030 [13]. Lead-free primer mandates in the EU and select U.S. ranges are further driving reformulation across the small-caliber segment.

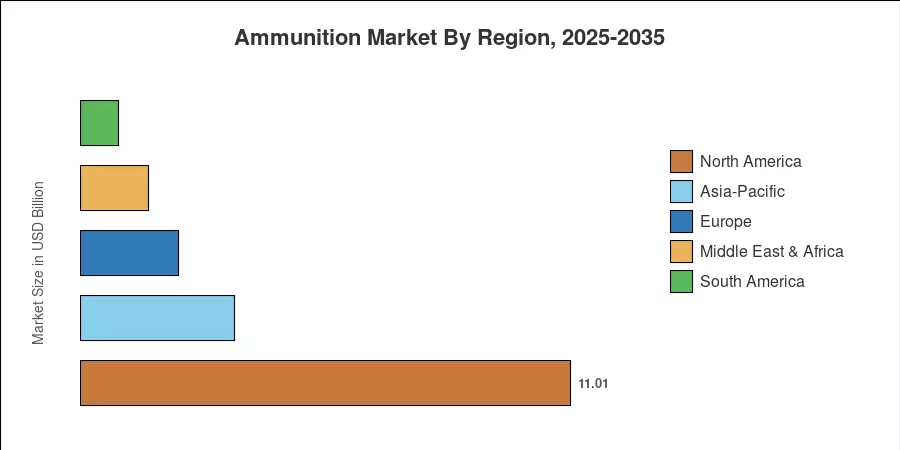

North America commanded roughly 51% of global Ammunition Market revenue in 2025, anchored by large-scale military procurement and a civilian sporting-arms base of over 16 million active participants [16]. Europe is the fastest-growing region, tracking a 10.20% CAGR through 2035, fueled by NATO replenishment targets and greenfield shell plants in Poland, Norway, and Germany [5]. Asia-Pacific held the second-largest share at approximately 16%, led by India's indigenous ordnance factory modernization and South Korea's K-series artillery programs [6]. The decade ahead promises a convergence of defense urgency and industrial expansion that will keep the Ammunition Market on an elevated growth path.

Key Report Takeaways

• By Product & Caliber

- Bullets and cartridges accounted for roughly 65% of the Ammunition Market in 2025, driven by high-volume military rifle and sidearm contracts worldwide.

- Small-caliber ammunition is forecast to grow at a 6.75% CAGR through 2035, outpacing the overall Ammunition Market as infantry modernization accelerates.

- Artillery shells and mortars are expanding at a 6.85% CAGR, reflecting NATO's 155 mm replenishment drive.

• By Guidance & End-User

- Non-guided ammunition represented roughly 86% of the global Ammunition Market in 2025, although precision-guided rounds are gaining share at twice the rate.

- The military segment contributed an estimated 88% of total Ammunition Market demand in 2025.

• By Region

- North America accounted for approximately USD 11.01 Billion of the Ammunition Market in 2025, bolstered by the Pentagon's sustained munitions procurement.

- Europe is forecast to reach the fastest regional CAGR of 10.20% through 2035, with the EU industrial-sovereignty agenda as the primary catalyst.

Market Size and Forecast (2021–2035)

Market Research Future's projections integrate bottom-up supply-side production data with top-down government procurement budgets, validated through primary interviews with defense procurement officers, OEM executives, and trade-body analysts across 32 countries.