Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| By Caliber | Small Caliber, Medium Caliber, Large Caliber, Others | Small Caliber (~46% share, 2025) | Large Caliber |

| By Product | Bullets and Cartridges, Artillery Shells and Mortars, Others | Bullets and Cartridges (~65% share, 2025) | Artillery Shells and Mortars |

| By Guidance | Non-Guided, Guided | Non-Guided (~86% share, 2025) | Guided |

| By End-User | Military, Law Enforcement, Others | Military (~88% share, 2025) | Military |

| By Platform | Land, Naval, Airborne | Land (~73% share, 2025) | Naval |

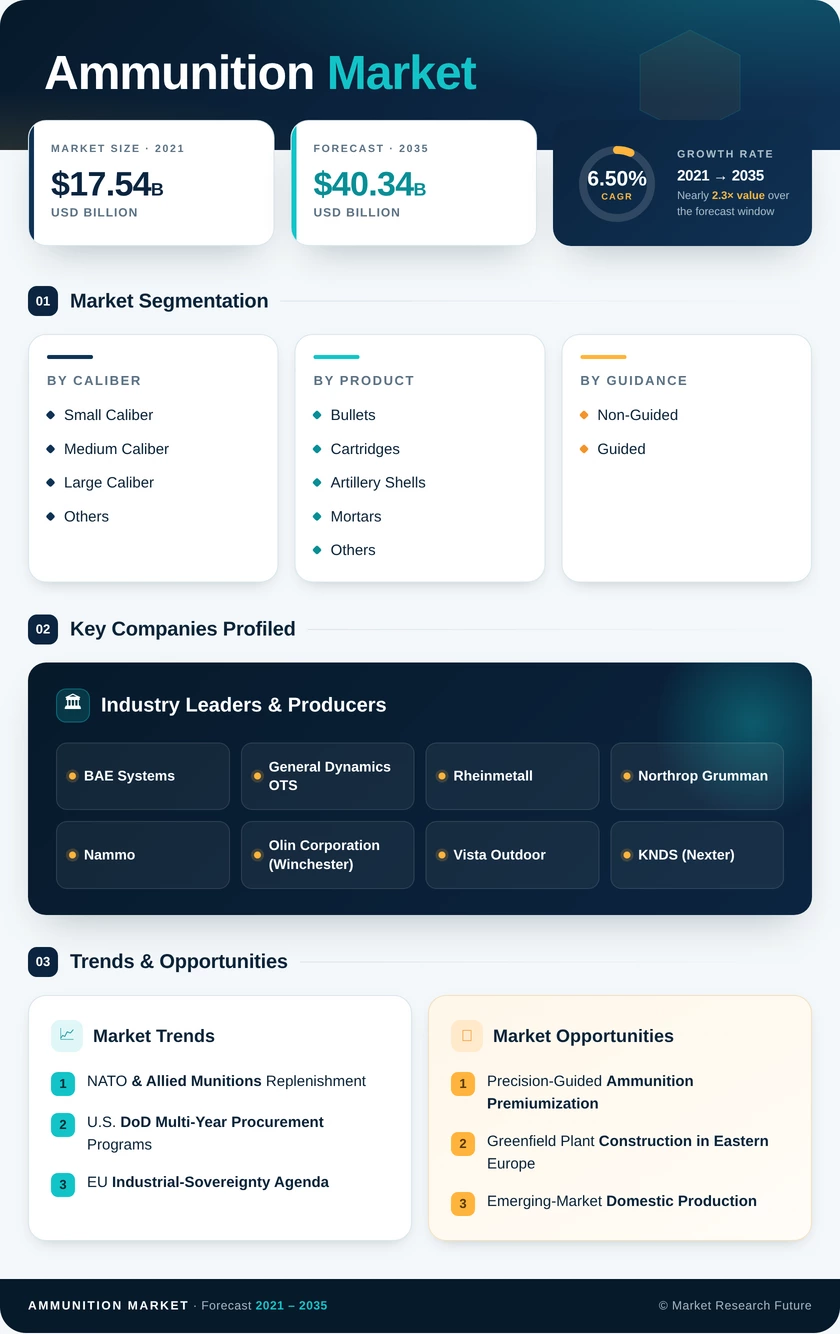

Market Segmentation Overview

By Caliber

| Sub-Segment | Key Trend |

| Small Caliber | Sustained volume from infantry modernization and civilian sporting-arms demand |

| Medium Caliber | Growing adoption in IFV/APC turret upgrades and naval CIWS systems |

| Large Caliber | Rapid expansion driven by NATO 155 mm replenishment and howitzer fleet growth |

| Others | Niche specialty ordnance including less-lethal and pyrotechnic applications |

Small-caliber ammunition accounts for the largest share of the Ammunition Market by volume, supported by military training cycles, law-enforcement duty loads, and a robust civilian base particularly in North America. Large-caliber rounds represent the most dynamic growth area as allied nations race to rebuild artillery stockpiles depleted since 2022.

By Product

| Sub-Segment | Key Trend |

| Bullets and Cartridges | High-volume recurring consumption across all end-user segments |

| Artillery Shells and Mortars | Accelerated procurement under NATO and Indo-Pacific defense frameworks |

| Others (Rockets, Grenades, Specialty) | Precision-strike and area-denial applications driving value growth |

Bullets and cartridges dominate product-level revenue, reflecting billions of rounds consumed annually. Artillery shells and mortars are gaining value share as multi-year government contracts for 155 mm and 120 mm projectiles expand production backlogs beyond 36 months at several major facilities.

By Guidance

| Sub-Segment | Key Trend |

| Non-Guided | Cost-efficient mass production; remains the foundation of military and civilian volumes |

| Guided | Course-correcting fuzes and programmable air-burst rounds driving premium pricing |

Non-guided ammunition continues to represent the overwhelming majority of units produced, though guided variants are capturing an increasing share of total value as defense ministries prioritize precision-strike capabilities and reduced collateral damage.

By End-User

| Sub-Segment | Key Trend |

| Military | Sustained by multi-year procurement cycles and stockpile-replenishment mandates |

| Law Enforcement | Steady demand driven by duty-ammunition refresh and training requirements |

| Others (Civilian, Sport) | Normalized retail inventories supporting stable small-caliber volumes |

The military segment dominates the Ammunition Market, accounting for the vast majority of both value and volume. Law enforcement and civilian end-users provide a stable demand floor that smooths cyclical defense-budget fluctuations.

By Platform

| Sub-Segment | Key Trend |

| Land | Largest platform segment spanning infantry to main-battle-tank calibers |

| Naval | Modernization of close-in weapon systems and medium-caliber naval guns |

| Airborne | Sustained by rotary-wing ground-support and aircraft cannon applications |

Land-based platforms consume the widest range of calibers and product types, from individual soldier loads to heavy artillery. Naval and airborne segments remain smaller but are growing as platform-upgrade cycles introduce higher-rate-of-fire weapons systems.