Alcoholic Beverages Market Summary

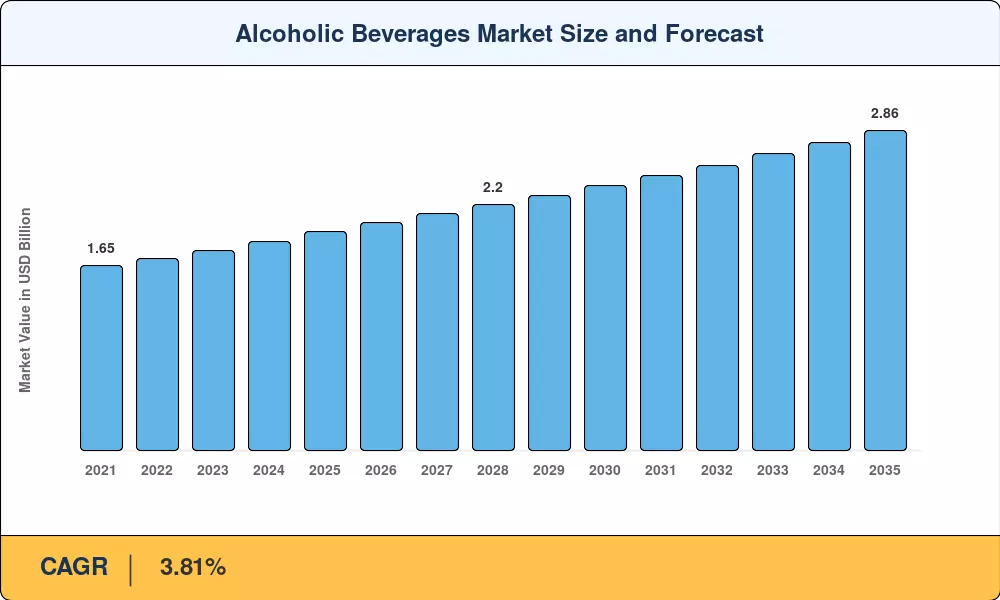

The Alcoholic Beverages Market reached a valuation of USD 1.96 trillion in 2025, positioning it among the largest consumer goods categories worldwide. Projected to grow from USD 2.04 trillion in 2026 to USD 2.86 trillion by 2035 at a CAGR of 3.81%, the Alcoholic Beverages Market is being reshaped by premiumization, evolving consumer preferences, and expanding digital distribution infrastructure. Government efforts to modernize excise frameworks — including updated U.S. fill standards enacted in 2024 and the EU's revised alcohol labeling directive — have created new portfolio flexibility for producers while simultaneously raising compliance costs for smaller operators [1][7].

A pronounced shift toward omnichannel retailing is redefining how producers connect with consumers. E-commerce platforms now account for a meaningful share of off-trade volume in mature economies, while direct-to-consumer models are emerging across craft and premium categories. Sustainability investments have accelerated, with major producers committing over USD 4 billion collectively toward water-positive distilleries, recyclable packaging, and carbon-neutral brewing operations between 2023 and 2025 [14][18].

Asia-Pacific commands approximately 31% of the Alcoholic Beverages Market, anchored by rising middle-class spending across China and India. The Middle East & Africa region is the fastest-growing geography at a 5.43% CAGR through 2035, driven by tourism infrastructure development and relaxation of licensing restrictions in select Gulf states. Europe holds the second-largest share at roughly 27.5%, sustained by deep-rooted consumption cultures and a robust premium export ecosystem. As health-conscious formulations and functional ingredients gain traction, the Alcoholic Beverages Market is set for structural diversification over the coming decade.

Key Report Takeaways

• By Product Type

- The Alcoholic Beverages Market saw its largest product category command a 46% share in 2025, driven by affordability, ubiquitous distribution, and cultural embeddedness across both developed and emerging economies.

- The fastest-growing product category is projected to register a 3.97% CAGR through 2035, fueled by premiumization and cocktail culture expansion in urban centers.

• By End User

- Male consumers accounted for 67% of the Alcoholic Beverages Market in 2025.

- Female consumption is expanding at a 4.21% CAGR, reflecting shifting social norms and targeted product innovation in lighter, flavored categories.

• By Region

- Asia-Pacific led the Alcoholic Beverages Market with a 31% revenue share in 2025.

- The Middle East & Africa region is forecast to register a 5.43% CAGR, the highest among all regions through 2035.

Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated methodology combining top-down revenue modeling, bottom-up production and consumption analysis, and trade flow reconciliation across 40+ countries. Historical figures draw on government excise records, customs data, and producer financial disclosures. Forecast projections apply category-level elasticity models adjusted for demographic, regulatory, and macroeconomic variables.