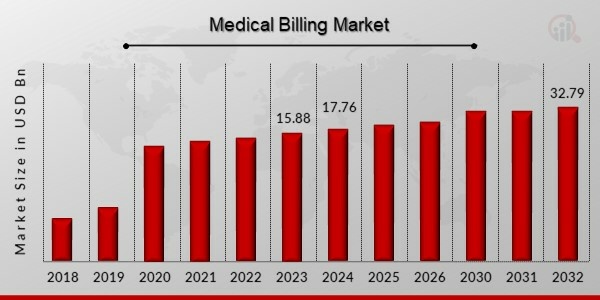

What is the current valuation of the Medical Billing Market as of 2024?

The Medical Billing Market was valued at 17.76 USD Billion in 2024.

What is the projected market size for the Medical Billing Market in 2035?

The market is projected to reach 62.65 USD Billion by 2035.

What is the expected CAGR for the Medical Billing Market from 2025 to 2035?

The expected CAGR for the Medical Billing Market during the forecast period 2025 - 2035 is 12.14%.

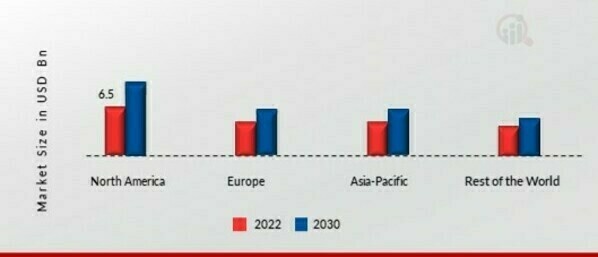

Which companies are considered key players in the Medical Billing Market?

Key players include Optum, Cognizant, GeBBS Healthcare Solutions, MediGain, eCatalyst Healthcare Solutions, Vee Technologies, R1 RCM, Visionary RCM, and nThrive.

How does the Professional Billing segment perform in terms of market valuation?

The Professional Billing segment was valued at 10.65 USD Billion in 2024 and is projected to reach 38.0 USD Billion by 2035.

What is the market valuation for the Institutional Billing segment?

The Institutional Billing segment was valued at 7.11 USD Billion in 2024 and is expected to grow to 24.65 USD Billion by 2035.

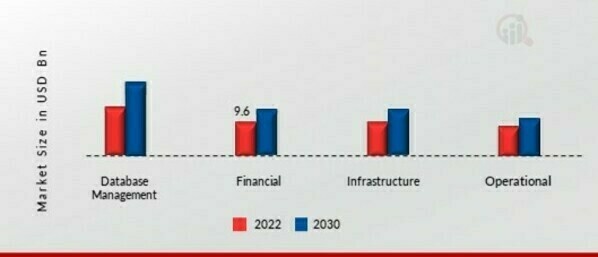

What are the key applications within the Medical Billing Market?

Key applications include Database Management, Financial, Infrastructure, and Operational, with valuations ranging from 3.55 to 18.0 USD Billion.

What is the projected growth for Electronic Billing in the Medical Billing Market?

The Electronic Billing segment was valued at 7.06 USD Billion in 2024 and is projected to reach 25.0 USD Billion by 2035.

How does the Medical Billing Services segment compare in terms of market size?

The Medical Billing Services segment was valued at 6.7 USD Billion in 2024 and is expected to grow to 23.15 USD Billion by 2035.

What is the significance of the Payment process in the Medical Billing Market?

The Payment process was valued at 4.0 USD Billion in 2024 and is projected to reach 14.5 USD Billion by 2035.