全球熔模铸造市场概览

2022 年熔模铸造市场规模为 150 亿美元,预计将从 2023 年的 190 亿美元增长到 2030 年的 260 亿美元,在预测期内(2023 - 2030 年)复合年增长率 (CAGR) 为 6.00%。熔模铸造市场增长的主要推动力是其对紧密尺寸结构和良好表面的控制。推动增长的其他因素包括其在飞机零部件制造中的广泛应用,以及工业中使用的机器零件的广泛使用,这是促进市场增长的关键市场驱动力。

资料来源:二次研究、初步研究、MRFR 数据库和分析师评论

熔模铸造市场趋势

国防工业需求的增加是推动熔模铸造市场增长的关键因素之一。熔模铸造,也称为精密铸造,是一种用于生产各种材料(包括钢、铝和钛)复杂、高精度部件的制造工艺。国防工业是熔模铸造部件的主要消费者,这些部件的应用范围广泛,包括航空航天和国防系统、军用车辆和武器系统。随着全球紧张局势的加剧以及对先进军事技术的需求,国防部门对熔模铸造零部件的需求预计将增长。

除国防工业外,熔模铸造还广泛应用于航空航天工业、汽车工业、医疗行业等。这些行业对轻质和高性能部件不断增长的需求也推动了熔模铸造市场的增长。此外,技术的进步和新材料的开发正在为熔模铸造创造新的机遇。 3D 打印和其他数字技术的使用也正在改变熔模铸造流程,使其更快、更准确且更具成本效益。因此,与熔模铸造相关的这些因素近年来提高了全球熔模铸造市场的复合年增长率。 2023年6月,铝铸造行业的知名企业CFS Foundry宣布推出广泛的先进铸造服务。凭借最先进的设备和技术,CFS Foundry重力铸造服务即使是复杂的设计也能确保高质量的铸件。

熔模铸造市场细分洞察

熔模铸造类型见解

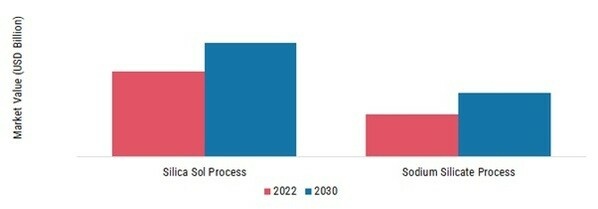

熔模铸造市场根据类型细分,包括硅溶胶工艺、硅酸钠工艺。 2022 年,硅溶胶工艺领域占据了熔模铸造市场收入的大部分份额。在硅溶胶工艺中,首先由所需的部分制成模型,然后涂上由二氧化硅和粘合剂的混合物制成的陶瓷壳。然后对外壳进行烧制,模型熔化或蒸发,在外壳中留下一个空腔。然后将熔融金属倒入型腔中,一旦金属凝固,外壳就会破裂,露出成品部件。

熔模铸造应用见解

根据应用,熔模铸造市场细分包括航空航天和航空航天领域。军事、一般工业、工业燃气轮机、汽车、其他。航空航天与军事领域在 2022 年占据市场主导地位,预计在 2023-2030 年预测期内将成为增长更快的领域。熔模铸造广泛应用于航空航天和国防工业,以制造需要承受高温、压力和其他极端条件的复杂零件。所有这些因素都对熔模铸造的市场增长产生积极影响。2023 年 7 月,Zollem GmbH Co., KG 完成了新的 IGT/AERO 熔模铸造生产线。 VA Technology 提供的 EQX 的 DS/SX 脱壳生产线和七轴 ABB 机器人系统均包含在本次开发中。

图 2:熔模铸造市场,按 2022 年和 2022 年类型划分2030 年(十亿美元)

资料来源:二次研究、初步研究、MRFR 数据库和分析师评论

投资铸造区域见解

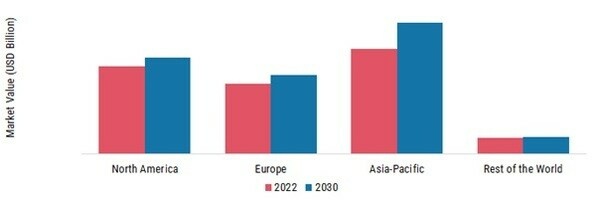

按地区划分,该研究提供了北美、欧洲、亚太地区和世界其他地区的市场洞察。亚太地区在熔模铸造市场中占据主导地位,预计在预测期内将以最快的复合年增长率增长。这主要是由于该地区工业化和基础设施发展迅速增长,特别是中国和印度等国家。汽车、航空航天和国防工业对熔模铸造的需求不断增长也推动了亚太地区市场的增长。

此外,市场报告研究的主要国家包括美国、加拿大、德国、法国、英国、意大利、西班牙、中国、日本、印度、澳大利亚、韩国和巴西

图 3:2022 年各地区投资铸造市场份额 (%)

资料来源:二次研究、初步研究、MRFR 数据库和分析师评论

欧洲熔模铸造市场占据第三大市场份额。欧洲市场的推动因素包括该地区几个主要参与者的存在,特别是德国和法国等国家,以及汽车和航空航天行业对熔模铸造的需求不断增长。然而,与其他地区相比,欧洲市场增长预计相对较慢,主要是由于该地区工业格局成熟且经济增长缓慢。此外,德国熔模铸造市场占有最大的市场份额,英国熔模铸造市场是欧洲地区增长最快的市场。

北美熔模铸造市场是全球主要市场之一,预计在预测期内将占据第二大市场份额。这主要是由于该地区存在一些关键参与者,包括主要的航空航天和国防公司,以及各种应用对高质量和复杂零件的需求不断增加。航空航天和国防工业是北美熔模铸造市场的主要驱动力之一。该地区是多家知名航空航天和国防公司的所在地,这些公司需要为飞机发动机、涡轮机和其他关键部件等各种应用提供高质量和精密的熔模铸件。此外,美国熔模铸造市场占有最大的市场份额,加拿大熔模铸造市场是北美地区增长最快的市场。

投资铸造主要市场参与者和市场参与者竞争洞察

主要市场参与者正在研发上投入大量资金以增加其产品线,这将有助于熔模铸造市场进一步增长。市场参与者还采取一系列战略举措来扩大其全球影响力,包括新产品发布、合同协议、并购、增加投资以及与其他组织的合作等关键市场发展。熔模铸造行业的竞争对手必须提供具有成本效益的产品,以便在竞争日益激烈和不断发展的市场环境中扩张和生存。

主要市场参与者正在研发上投入大量资金以扩大其产品线,这将刺激熔模铸造市场的进一步增长。随着新产品发布、合同协议、并购、投资增加以及与其他组织的合作等重大市场发展,市场参与者也在采取各种战略活动来扩大其全球影响力。为了在竞争日益激烈、不断发展的市场环境中发展壮大,熔模铸造行业的竞争对手必须提供价格实惠的产品。

本地制造以降低运营成本是制造商在全球熔模铸造行业中为使客户受益并扩大市场领域而采用的主要商业策略之一。主要熔模铸造市场参与者包括美国铝业公司、万冠公司、Precision Castparts CORP、Metatek International Inc、WINSERT、宁波吉伟熔模铸件有限公司、Zollern GMBH Co.。 CO. KG、台州新宇精密制造有限公司、Milwaukee Precision Casting, INC、东风精密铸造有限公司、IMPRO Precision Industries Limited、AGC陶瓷和东营嘉扬精密金属有限公司等都试图通过资助研发活动来增加市场需求。

美国铝业公司 (Alcoa Corporation) 是铝土矿、氧化铝和铝产品生产的全球领导者。该公司经营三个业务部门:铝土矿、氧化铝和铝。铝土矿业务包括开采铝土矿,然后将其加工成氧化铝。氧化铝部门包括将铝土矿精炼成氧化铝,然后将其出售给铝冶炼厂。 铝部门包括将氧化铝熔炼成铝,以及生产轧制、挤压和锻造铝产品等增值产品。美铝的产品广泛应用于各个行业,包括航空航天、汽车、商业运输、建筑、包装和工业产品。

MetalTek International 是一家为航空航天、国防、能源、工业和医疗行业关键应用提供工程解决方案、冶金专业知识和精密部件制造的全球供应商。 MetalTek International 提供一系列产品和服务,包括熔模铸造、砂型铸造、离心铸造、连续铸造和制造。该公司的熔模铸造能力包括不锈钢、超级合金和铝等多种合金,其应用范围从飞机发动机部件到医疗植入物。

美国铝业公司 (Alcoa Corporation) 公布了到 2050 年在全球实现温室气体 (GHG) 净零排放的计划。这一目标与该公司推进可持续发展的优先事项一致,并建立在现有目标的基础上,其中包括直接和间接排放减少 30%。铝冶炼和铝冶炼间接温室气体排放氧化铝精炼作业由二十五时五十起。目标设定过程还考虑了范围一(直接)和范围二(间接)排放,美国铝业公司控制下的全球所有工厂应不迟于本世纪中叶消除这些排放,同时仍然跟上每个相关部门的业务增长机会。

熔模铸造市场的主要公司包括

- 美国铝业公司

- 万冠

- 精密铸件公司

- etaltek国际公司

- WINSERT

- 宁波吉伟熔模铸件有限公司

- 佐伦有限公司两合公司

- 台州新宇精密制造有限公司

- 密尔沃基精密铸造公司

- 东风精密铸造有限公司

- IMPRO精密工业有限公司

- AGC陶瓷

- 东营嘉扬精密金属有限公司等

熔模铸造行业发展

根据新闻稿,2022 年 10 月,关键金属零件的先进制造商 Winsert 收购了熔模铸造和机械加工公司 Alloy Cast Products Inc.。此举将使两家公司受益,因为他们将能够在其生命周期中进入产品开发的新领域。

2022 年 8 月,AmeriTi Manufacturing 成立了 TriTech Titanium Parts,在底特律市场推出钛部件。 TriTech Titanium Parts 采用先进的方法生产高质量的产品,包括金属注射、3D 粘合剂喷射打印和熔模铸造。这些钛零件专为各种工业、航空航天、汽车和医疗应用而设计。

2021 年 10 月,美国铝业公司公开承诺到 2050 年在全球所有业务中实现温室气体 (GHG) 净零排放目标。这符合公司可持续发展的愿景,也是公司当前行业转型目标的补充,即到 2025 年将铝冶炼和氧化铝精炼业务的直接和间接温室气体排放量分别减少 30% 和 2030 年 50%。目标是通过公司战略的直接(范围 1)和间接(范围 2)排放,到 2050 年实现温室气体净排放量为零,因此将在 2050 年实现。

熔模铸造市场细分

熔模铸造类型展望

熔模铸造应用前景

熔模铸造区域展望

- 北美

- 欧洲

- 亚太地区

- 中国

- 日本

- 印度

- 澳大利亚

- 韩国

- 澳大利亚

- 亚太地区其他地区

- 世界其他地区