到2032年,全球GigE相机市场的预期市场规模是多少?

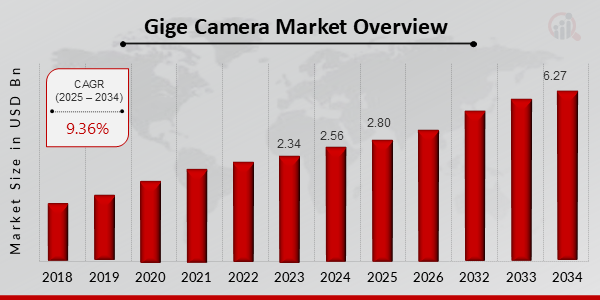

到2034年,全球GigE相机市场预计将达到62.7亿美元的价值

2024年至2032年全球GigE相机市场的复合年增长率(CAGR)是多少?

全球GigE相机市场在2025年至2034年的复合年增长率(CAGR)预计为9.36%。

到2032年,预计哪种相机类型将在全球GigE相机市场中按价值占主导地位?

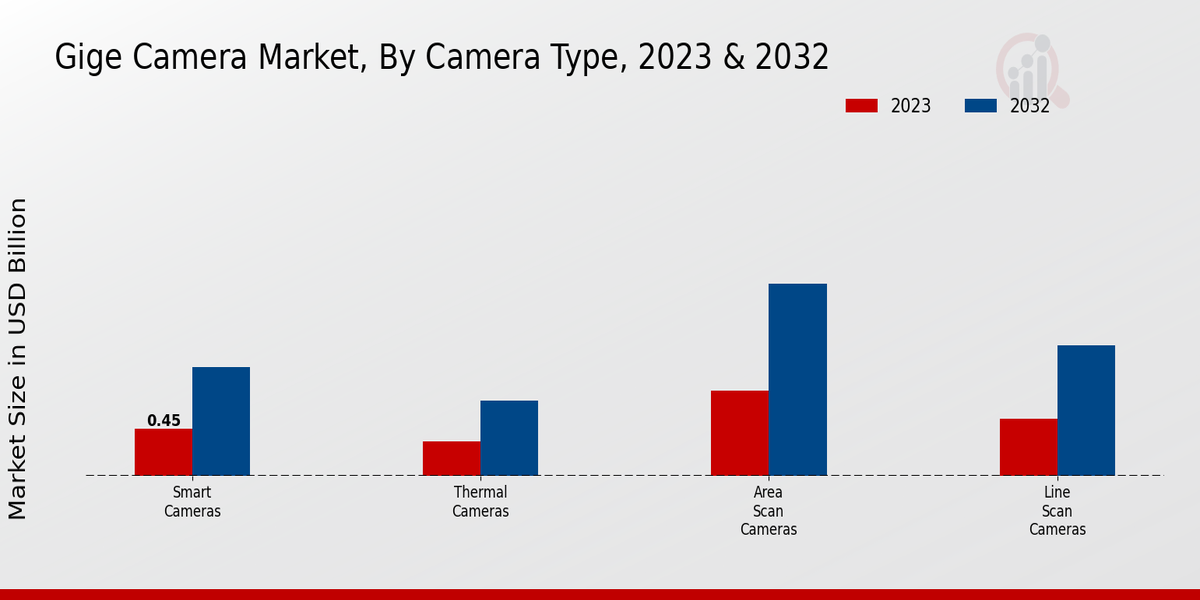

区域扫描相机预计将在2034年主导全球GigE相机市场,市场价值为18.6亿美元。

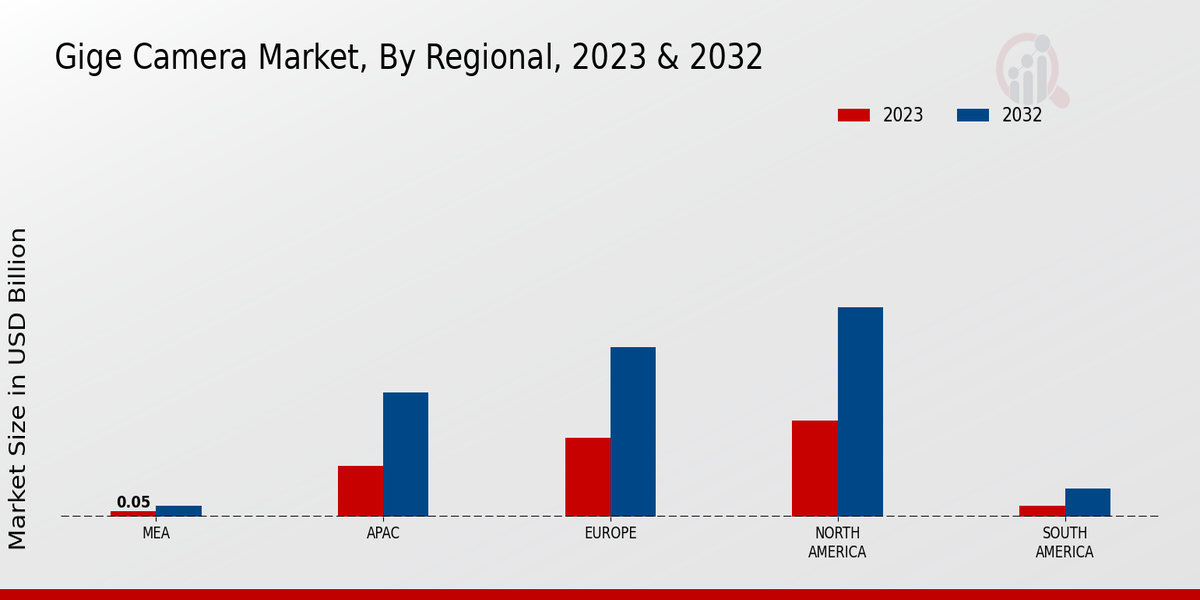

到2032年,北美地区在全球GigE相机市场的预测价值是多少?

预计到2032年,北美在全球GigE相机市场的价值将达到18.5亿美元。

目前在全球GigE相机市场中,哪些关键参与者具有重要意义?

全球GigE相机市场的主要参与者包括Point Grey、The Imaging Source、Sony和FLIR Systems。

到2032年,线扫描相机细分市场预计将达到什么市场价值?

线扫描相机细分市场预计在2032年将达到12.6亿美元的价值。

到2032年,亚太地区在全球GigE相机市场预计将实现什么增长?

预计到2032年,亚太地区在全球GigE相机市场的价值将增长至11亿美元。

到2032年,全球GigE相机市场中热像仪的预期市场规模是多少?

热成像相机预计到2032年市场价值将达到7.3亿美元。

全球GigE相机市场增长可能面临哪些挑战?

挑战可能包括技术变革和主要参与者之间的竞争加剧。

2032年智能相机的预测市场价值是多少?

智能摄像头预计在2032年的市场价值为10.5亿美元。