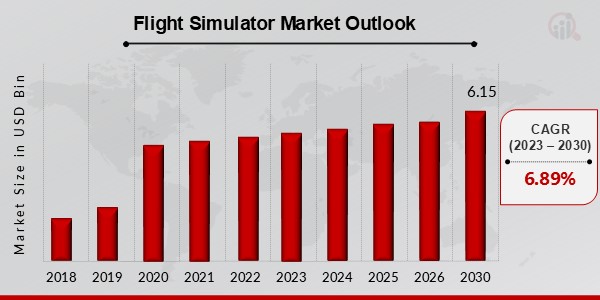

What is the current valuation of the Flight Simulator Market as of 2024?

The Flight Simulator Market was valued at 21.8 USD Billion in 2024.

What is the projected market size for the Flight Simulator Market by 2035?

The market is projected to reach 42.2 USD Billion by 2035.

What is the expected CAGR for the Flight Simulator Market during the forecast period 2025 - 2035?

The expected CAGR for the Flight Simulator Market during 2025 - 2035 is 6.21%.

Which companies are considered key players in the Flight Simulator Market?

Key players include Microsoft, Lockheed Martin, Laminar Research, and Dovetail Games.

What segment of the Flight Simulator Market had the highest valuation in 2024?

The Pilot Training segment had the highest valuation at 8.0 USD Billion in 2024.

How much is the Air Traffic Control Simulation segment projected to grow by 2035?

The Air Traffic Control Simulation segment is projected to grow from 3.5 USD Billion in 2024 to 6.5 USD Billion by 2035.

What is the valuation range for the Consumer Flight Simulators segment by 2035?

The Consumer Flight Simulators segment is expected to range from 7.0 USD Billion to 14.0 USD Billion by 2035.

Which platform is anticipated to have the highest growth in the Flight Simulator Market?

The Virtual Reality platform is anticipated to grow from 5.0 USD Billion in 2024 to 10.0 USD Billion by 2035.

What is the projected valuation for the Simulation Software technology segment by 2035?

The Simulation Software technology segment is projected to reach between 9.8 USD Billion and 16.2 USD Billion by 2035.

How does the Home Users segment compare to the Military segment in terms of valuation?

The Home Users segment was valued at 1.8 USD Billion in 2024, whereas the Military segment was valued at 5.0 USD Billion.