North America: Expanding high‑spend healthcare system

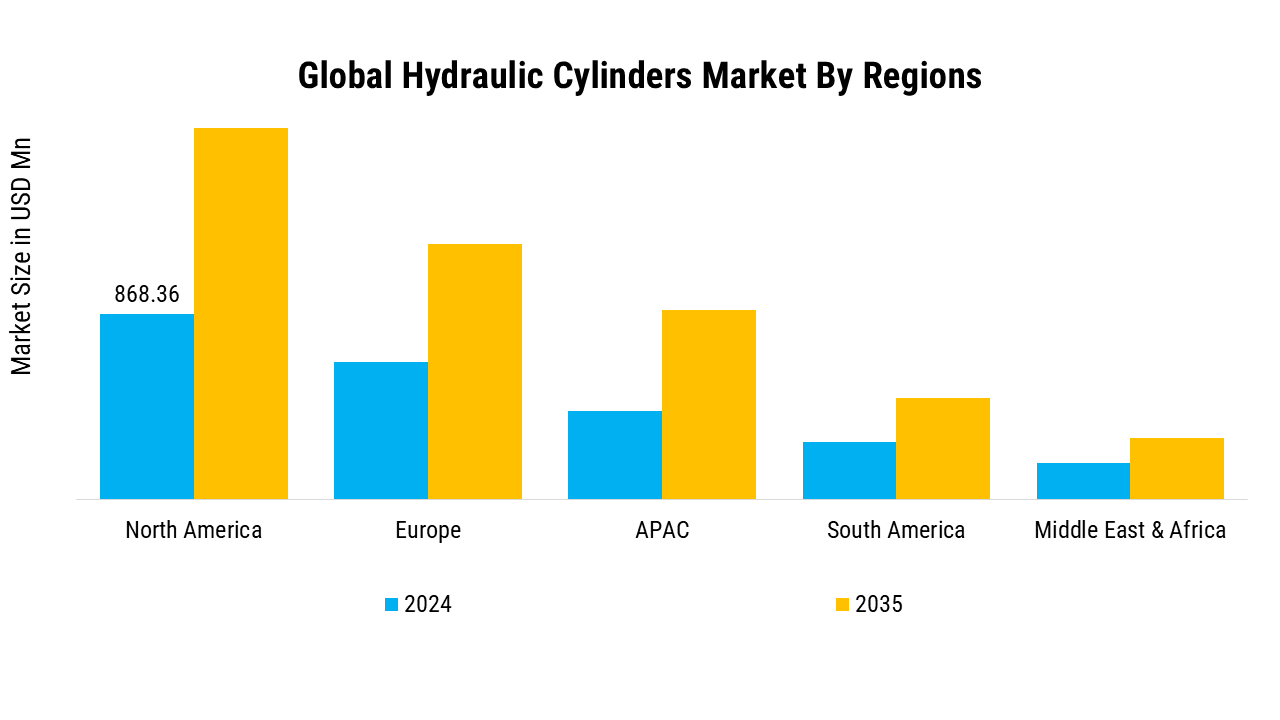

North America leads in the Wound Gel Market size, accounting for over 36.64% of the global revenue in 2024, underpinned by a mature, high‑spend healthcare system. Chronic‑wound prevalence—especially diabetes‑related ulcers and pressure sores—supports strong demand in hospitals, outpatient clinics, and home‑care settings. North America’s Wound Gel Market growth is driven by high chronic wound prevalence, advanced healthcare infrastructure, and increasing adoption of premium wound management technologies.

- According to the Centers for Disease Control and Prevention, diabetes and obesity prevalence continue to rise across the United States, increasing risks associated with diabetic foot ulcers and chronic wounds. Expanding use of advanced wound care products, strong reimbursement frameworks, and rising surgical procedures are accelerating wound gel adoption throughout North America.

Advanced infrastructure, continuous innovation in hydrogel and antimicrobial gel technologies, and favorable reimbursement for premium advanced‑wound‑care products further consolidate North America’s leadership role. The U.S. alone represents the largest national market, with a projected CAGR of about 5.8% through the mid‑2030s driven by rising surgical volumes and value‑based care models that emphasize faster healing and reduced complications.

Europe: Strong Production high rates of chronic wounds

Europe Wound Gel Market size was valued at USD 711.06 Million in 2024, making it the second-largest regional market with a 30% share. An aging population, high rates of chronic wounds, and strong government support for advanced wound‑care solutions sustain demand for high‑performance gels, including antimicrobial and bioactive variants. Europe’s Wound Gel Market is expanding due to aging populations, increasing chronic wound incidence, and strong government support for advanced wound care technologies.

Strict regulatory frameworks ensure product quality and safety, which builds clinician and payer confidence, while increasing home‑health and outpatient‑center use expand the settings where wound gels are deployed. European countries are also at the forefront of integrating digital‑wound‑assessment tools and AI‑driven care pathways with advanced gel therapy, reinforcing their position as a premium‑care hub.

- The World Health Organization reports a rapidly aging European population with growing chronic disease burdens requiring long-term wound management solutions. Increasing adoption of antimicrobial gels, expansion of outpatient wound care services, and integration of digital wound assessment technologies are strengthening advanced wound care demand across Germany, France, and the United Kingdom.

Asia Pacific: Rising diabetes prevalence

Asia‑Pacific (APAC) is projected to grow at the fastest CAGR of about 5.6–5.7%, making it the key growth engine over the next decade. Rising diabetes prevalence, a rapidly aging population, expanding surgical volumes, and improving healthcare infrastructure—especially in China, Japan, and India—drive adoption of hydrogel and antimicrobial wound gels.

Medical‑tourism‑oriented private hospitals and rising healthcare expenditure further support penetration of premium products, while price‑sensitive public‑sector and rural settings rely on simpler, cost‑effective gels.

South America: Rising urbanization, and increasing diabetes

South America is characterized by gradual market expansion, with Brazil and Mexico as the main growth poles. Improving healthcare systems, rising urbanization, and increasing diabetes and obesity rates are expanding the pool of chronic‑wound patients eligible for advanced gel‑based therapy.

However, affordability and reimbursement constraints limit the penetration of high‑end antimicrobial and bioactive gels, pushing manufacturers to offer more cost‑optimized portfolios and hybrid‑pricing models to capture volume. Altogether, regional dynamics show a clear split: North America and Europe lead in value and innovation, APAC drives volume and growth, and MEA and South America represent emerging frontiers with rising but uneven adoption.

Middle East & Africa: Rising surgical and diabetic‑wound cases

Middle East and Africa (MEA) is a nascent but gradually expanding region, with countries such as Saudi Arabia and the UAE leading the sub‑regional market. Growing healthcare spending, government investment in hospital capacity, and a rising number of surgical and diabetic‑wound cases are lifting demand for advanced wound gels, though access remains uneven and often skewed toward urban centers.

The MEA market is expected to grow at a moderate pace, supported by efforts to localize product offerings and build distribution networks that can penetrate underserved areas.