Mesotherapy Market Summary

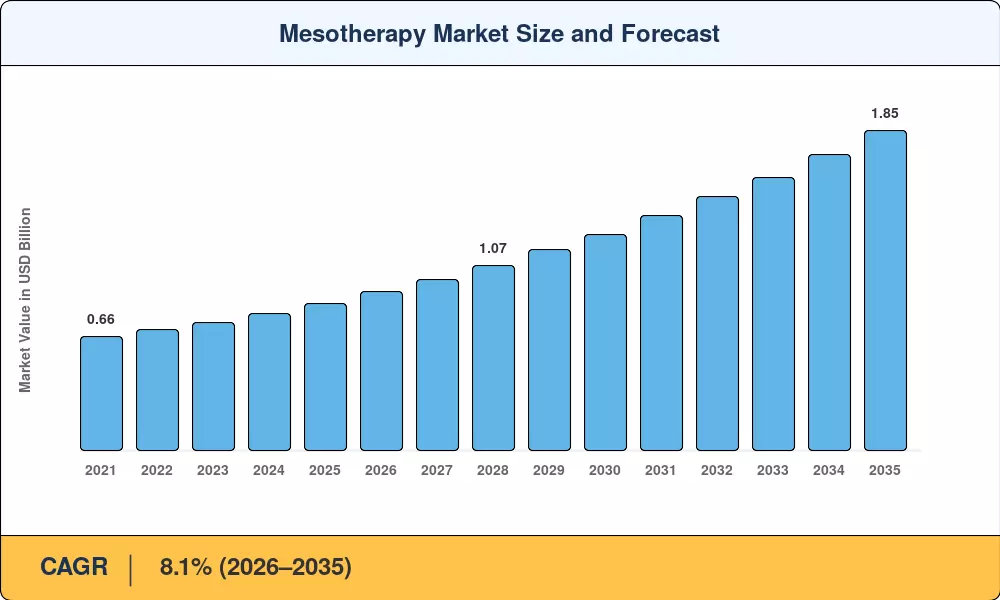

The Global Mesotherapy Market size was valued at USD 0.85 Billion in 2025, and the market is projected to grow from USD 0.92 Billion in 2026 to USD 1.85 Billion by 2035, registering a CAGR of 8.1% during the forecast period 2026–2035. This acceleration is anchored in two converging forces: a global consumer pivot toward minimally invasive cosmetic procedures and a regulatory environment that is gradually standardizing injectable aesthetic protocols across the EU and North America [2]. Rising disposable incomes in emerging economies have also expanded the addressable patient pool beyond traditional high-income demographics.

The technology landscape underpinning the mesotherapy market is shifting rapidly. Legacy manual syringe techniques are giving way to sensor-equipped injector guns and needle-free electroporation platforms that deliver active ingredients with sub-millimeter precision [3]. Manufacturers investing in AI-guided dosing algorithms and real-time feedback systems are commanding premium pricing — a trend that mirrors the broader medtech push toward device-centric care pathways. Meanwhile, the emergence of stem-cell–derived exosome cocktails is marking a departure from purely chemical formulations toward biologically active ingredient systems [4].

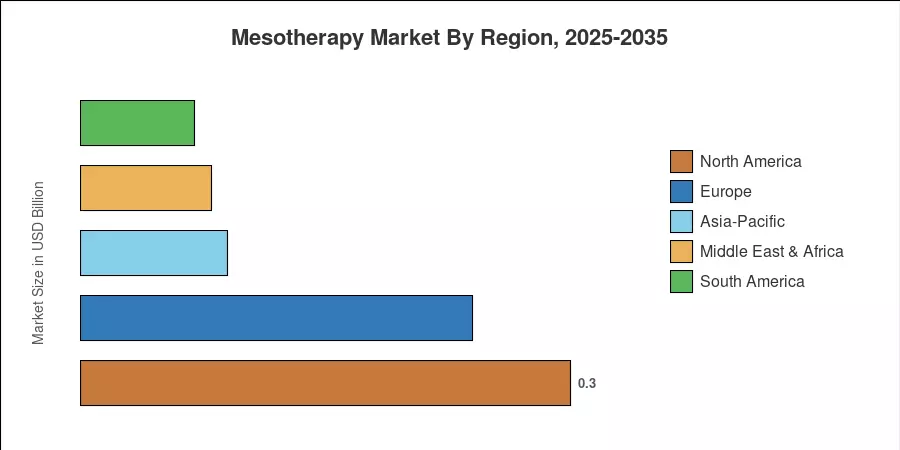

North America holds the dominant position in the mesotherapy market, accounting for roughly 35% of global revenue in 2024, underpinned by high per-capita aesthetic spending and an established network of dermatology clinics and MedSpas. Asia-Pacific is the fastest-growing region at a projected 10.2% CAGR through 2035, driven by expanding middle-class populations in China, India, and South Korea [5]. Europe remains the second-largest contributor, with France and Italy serving as innovation hubs for injectable cocktail formulations. The decade ahead will be defined by platform convergence — combining device intelligence, bioactive ingredients, and recurring treatment protocols into integrated service offerings.

Key Report Takeaways

• By Product Type & Device

- Dermal fillers captured approximately 44.1% revenue share of the mesotherapy market in 2024, reflecting strong demand for volumizing and hydration treatments.

- Mesotherapy devices are poised to expand at an 11.3% CAGR through 2035 as clinics transition to precision-driven hardware platforms.

- Solutions and cocktails remain the broadest product category by SKU count, with hyaluronic acid–based formulations leading ingredient preference.

• By Application

- The mesotherapy market for skin rejuvenation applications held a 58.1% share in 2024, well ahead of hair restoration and body contouring verticals.

• By End-User

- The mesotherapy market for skin rejuvenation applications held a 58.1% share in 2024, well ahead of hair restoration and body contouring verticals.

- MedSpas and aesthetic centers are posting the fastest end-user growth at a 12.1% CAGR, as consumers seek premium, spa-like treatment environments.

• By Region

- North America contributed roughly USD 0.30 billion in mesotherapy market revenue in 2024, sustained by established reimbursement-adjacent cash-pay models.

- Asia-Pacific is forecast to expand at a 10.2% CAGR, with South Korea and China driving adoption through K-beauty and medical tourism channels.

Market Size and Forecast (2021–2035)

Market Research Future estimates are derived from a combination of primary interviews with clinic operators and device manufacturers, secondary analysis of regulatory filings, and triangulation against publicly benchmarked datasets. All figures are expressed in USD Billion at constant 2025 exchange rates.