Sonobuoy Size

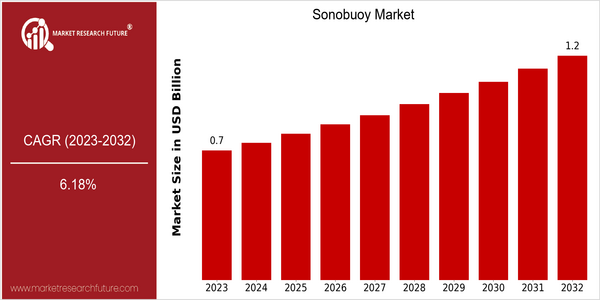

Market Size Snapshot

| Year | Value |

|---|---|

| 2023 | USD 0.7 Billion |

| 2032 | USD 1.2 Billion |

| CAGR (2024-2032) | 6.18 % |

Note – Market size depicts the revenue generated over the financial year

The global sonobuoy market is currently valued at approximately USD 0.7 billion in 2023 and is projected to reach USD 1.2 billion by 2032, reflecting a robust compound annual growth rate (CAGR) of 6.18% from 2024 to 2032. This growth trajectory indicates a steady increase in demand for sonobuoys, which are critical for anti-submarine warfare and maritime surveillance applications. The market's expansion can be attributed to rising geopolitical tensions, increased naval spending, and advancements in underwater acoustic technologies that enhance the operational capabilities of sonobuoys.

Several factors are driving this market growth, including the integration of advanced technologies such as artificial intelligence and machine learning in sonar systems, which improve detection accuracy and operational efficiency. Additionally, the growing emphasis on maritime security and the need for effective surveillance in coastal and offshore areas are propelling investments in sonobuoy systems. Key players in the industry, such as Raytheon Technologies, Thales Group, and Northrop Grumman, are actively engaging in strategic initiatives, including partnerships and product innovations, to enhance their market presence and meet the evolving demands of defense and security sectors.

Regional Market Size

Regional Deep Dive

The Sonobuoy Market is characterized by a growing demand for advanced underwater surveillance systems across various regions. In North America, particularly the United States, the market is driven by significant investments in defense and maritime security, with a focus on enhancing naval capabilities. Europe is witnessing a surge in collaborative defense initiatives among NATO countries, while the Asia-Pacific region is experiencing rapid technological advancements and increased military spending, particularly in countries like China and India. The Middle East and Africa are seeing a rise in maritime security concerns, prompting investments in sonobuoy technology. Latin America, while less prominent, is gradually recognizing the importance of underwater surveillance for its coastal security needs. Overall, the market dynamics are shaped by regional security challenges, technological innovations, and government policies aimed at enhancing maritime capabilities.

Europe

- The European Union has initiated collaborative defense projects aimed at standardizing sonobuoy technology among member states, enhancing interoperability and joint operational capabilities.

- Countries like the UK and France are increasing their defense budgets, leading to a rise in procurement of advanced sonobuoy systems to bolster their naval forces against potential threats in the North Atlantic.

Asia Pacific

- China's rapid naval expansion has led to increased investments in sonobuoy technology, with state-owned enterprises developing indigenous systems to enhance their maritime surveillance capabilities.

- India's recent defense procurement policies emphasize indigenous production of sonobuoys, with the government encouraging local manufacturers to develop advanced underwater surveillance systems.

Latin America

- Countries like Brazil are beginning to recognize the strategic importance of sonobuoys for monitoring their vast maritime territories, leading to initial investments in this technology.

- The region's growing focus on protecting natural resources, such as oil and gas reserves, is driving interest in advanced underwater surveillance systems, including sonobuoys.

North America

- The U.S. Navy has recently expanded its sonobuoy procurement programs, focusing on next-generation systems that enhance anti-submarine warfare capabilities, reflecting a strategic shift towards countering emerging threats.

- Key players like Raytheon Technologies and Lockheed Martin are investing in R&D to develop advanced sonobuoy technologies, including those that integrate artificial intelligence for improved data analysis and operational efficiency.

Middle East And Africa

- The Gulf Cooperation Council (GCC) countries are investing heavily in maritime security, leading to increased demand for sonobuoy systems to monitor their extensive coastlines and offshore resources.

- Regional conflicts and piracy concerns have prompted nations like Saudi Arabia and South Africa to enhance their naval capabilities, including the acquisition of advanced sonobuoy technology.

Did You Know?

“Sonobuoys can be deployed from aircraft, ships, or submarines, and they can operate autonomously for extended periods, providing real-time data on underwater activity.” — U.S. Navy Research and Development

Segmental Market Size

The Sonobuoy Market segment is currently experiencing stable growth, driven primarily by increasing defense budgets and the rising need for anti-submarine warfare capabilities. Key factors propelling demand include advancements in sonar technology and heightened maritime security concerns, particularly in regions like the Indo-Pacific, where naval tensions are escalating. Additionally, regulatory policies favoring enhanced naval capabilities further stimulate market interest.

Currently, the adoption stage of sonobuoys is in the scaled deployment phase, with notable contributions from companies like Raytheon and Northrop Grumman, which are leading in the development of advanced sonobuoy systems. Primary applications include anti-submarine warfare, maritime surveillance, and environmental monitoring, with the U.S. Navy and allied forces actively utilizing these technologies in various operations. Trends such as increased military collaborations and the push for sustainable defense solutions are catalyzing growth, while innovations in digital signal processing and miniaturization of components are shaping the segment's evolution.

Future Outlook

The Sonobuoy Market is poised for significant growth from 2023 to 2032, with a projected market value increase from $0.7 billion to $1.2 billion, reflecting a compound annual growth rate (CAGR) of 6.18%. This growth trajectory is driven by the increasing demand for advanced maritime surveillance and anti-submarine warfare capabilities, particularly among naval forces worldwide. As geopolitical tensions rise and maritime security becomes a priority, the adoption of sonobuoys is expected to expand, enhancing underwater detection and monitoring capabilities. By 2032, it is anticipated that the penetration of sonobuoy technology in military applications will reach approximately 30% of naval operations, up from current levels, indicating a robust integration into defense strategies.

Key technological advancements, such as the development of more sophisticated sonobuoy designs with enhanced data processing and communication capabilities, are expected to further propel market growth. Innovations in sensor technology and the integration of artificial intelligence for data analysis will improve the effectiveness and efficiency of sonobuoys, making them indispensable tools for modern naval operations. Additionally, supportive government policies and increased defense budgets in various countries will likely facilitate the procurement of advanced sonobuoy systems. As the market evolves, emerging trends such as the shift towards unmanned systems and the growing emphasis on multi-domain operations will shape the future landscape of the sonobuoy market, ensuring its relevance and expansion in the coming years.

Leave a Comment