Specialty Films Market Summary

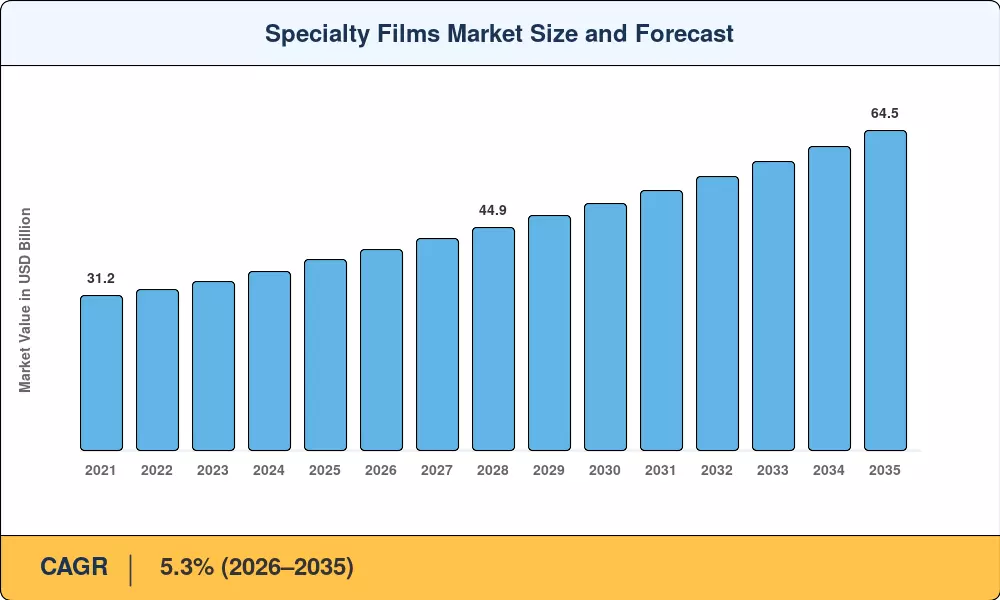

The Specialty Films Market reached an estimated USD 38.5 billion in 2025 and is projected to grow from USD 40.5 billion in 2026 to USD 64.5 billion by 2035, registering a CAGR of 5.3% during the forecast period (2026–2035). This growth trajectory reflects intensifying demand for high-performance films across packaging, electronics, and transportation end-use sectors. Tighter sustainability mandates — including the EU's Single-Use Plastics Directive and expanding extended producer responsibility (EPR) programs in North America — are compelling converters to adopt advanced packaging films with superior recyclability and barrier properties [1].

A generational shift in material science is reshaping the Specialty Films Market landscape. Legacy single-layer commodity films are giving way to multilayer film products engineered for precise oxygen transmission, moisture control, and UV resistance. Capital expenditures in functional polymer films production lines exceeded USD 4.2 billion globally in 2024, with major resin producers investing heavily in bio-based polyester and nylon extrusion platforms [2]. Regulatory pressure from REACH and FDA compliance frameworks continues to accelerate this transition toward barrier film materials that deliver performance without per- and polyfluoroalkyl substances (PFAS).

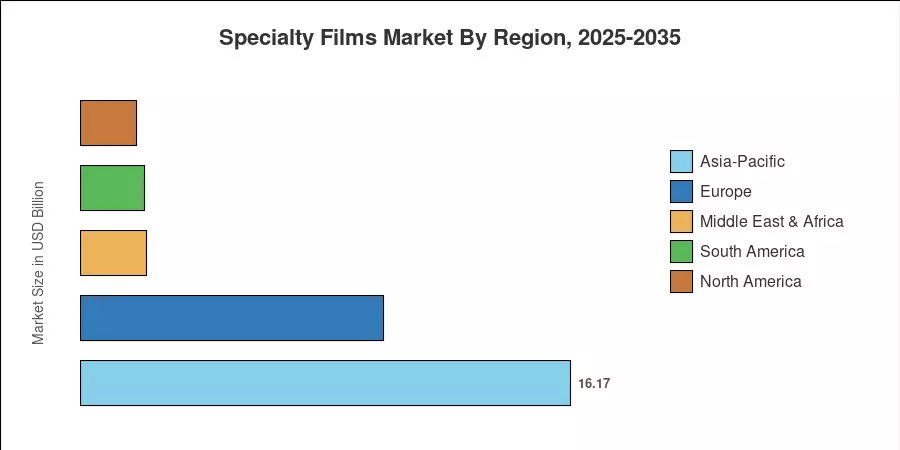

Asia-Pacific commands the largest share of the Specialty Films Market at approximately 42% of global revenue, driven by China's packaging sector and India's electronics manufacturing expansion. The region also represents the fastest-growing region, with a projected CAGR of 6.1%. Europe holds the second-largest position at roughly 26% share, supported by circular economy legislation and automotive lightweighting initiatives. North America rounds out the top three, where flexible film materials demand in pharmaceutical and food packaging continues to climb steadily through 2035.

Key Report Takeaways

• By Resin Type

- Polyester resin holds the largest share of the Specialty Films Market at approximately 32%, driven by demand in flexible packaging and electrical insulation applications

- Polyolefin films are projected to grow at a CAGR of 6.0%, the fastest among resin segments, fueled by cost-effective protective film coatings in industrial applications

- Fluoropolymer films command the highest per-unit pricing due to specialized use in semiconductor and aerospace applications

• By Function

- Barrier function films account for over 35% of total revenue in the Specialty Films Market, reflecting the dominance of food and pharmaceutical packaging demand

- Conduction and insulation films are expanding rapidly as EV battery manufacturing and 5G infrastructure scale globally

• By Region

- Asia-Pacific dominates the Specialty Films Market with a 42% revenue share and is simultaneously the fastest-growing region

- North America is projected to reach USD 12.8 billion by 2035, underpinned by the reshoring of electronics manufacturing

- Europe's circular economy mandates are accelerating the adoption of recyclable multilayer film products

Market Size and Forecast (2021–2035)

MRFR's market sizing combines bottom-up revenue aggregation from 120+ film converters and resin suppliers with top-down validation against trade association production volume data. Historical figures draw on customs trade databases, company filings, and regional polymer consumption statistics, while forecast estimates integrate macroeconomic inputs and regulatory scenario modeling.