Medical Electronics Market Summary

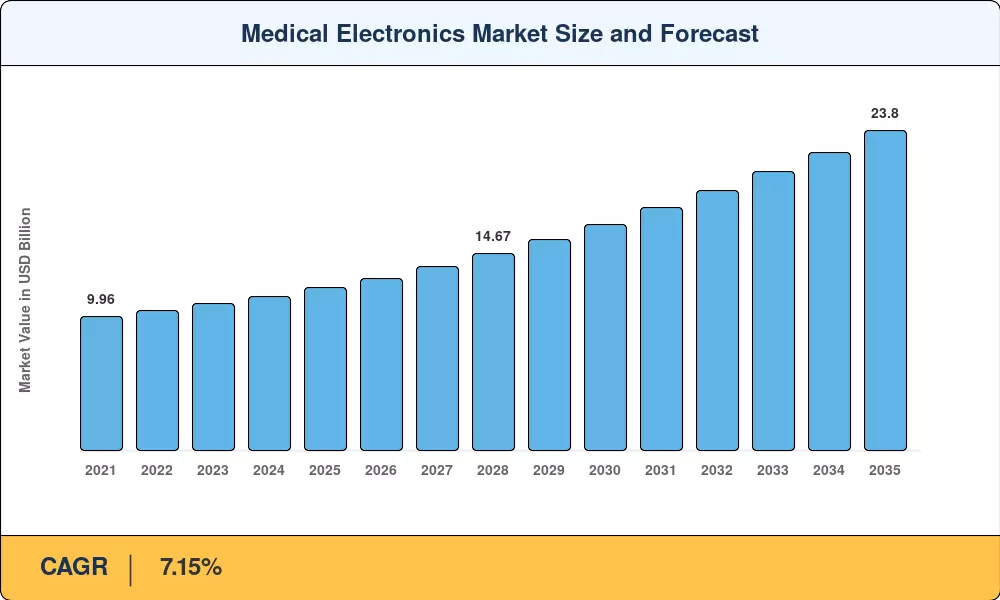

The Global Medical Electronics Market size was valued at USD 12.10 Billion in 2025, and the market is projected to grow from USD 12.78 Billion in 2026 to USD 23.80 Billion by 2035, registering a CAGR of 7.15% during the forecast period 2026–2035. Two converging forces underpin this trajectory: the FDA's 2024 cybersecurity guidance [1], which compels OEMs to redesign connected devices with embedded software bills of materials, and the broader reimbursement pivot toward value-based care models that reward continuous monitoring over episodic imaging. Together, these policy and payment shifts are unlocking fresh capital allocation toward sensor-dense, AI-ready platforms.

Legacy analog instrumentation is gradually being replaced by digitally integrated systems, using edge-computing modules coupled with cloud analytics. From 2023 through 2025, the U.S. Department of Health and Human Services is providing approximately USD 1.5 billion in grants for digital health interoperability [2] to speed the move from isolated bedside monitors to standards-compliant, networked systems. Helium shortage is simultaneously pushing MRI procurement funds to low-cryogen magnet platforms, offering disruptive chances for zero-boil-off technology development.

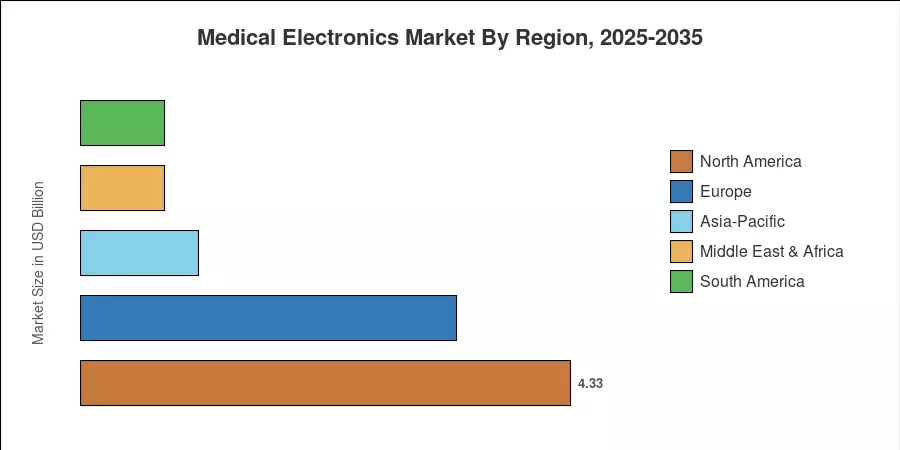

North America accounts for 35.8% of the medical electronics market, driven by high per capita spending on devices and developed hospital IT infrastructure. Asia-Pacific is the fastest-growing area, with a CAGR of 8.62%, due to hospital-construction plans in China and India and expanding middle-class demand for outpatient diagnostics. Europe remains in second position with a share of roughly 27.4%, driven by national digitization mandates in Germany and France. Vertical integration of supply chains will continue to fuel consolidation of the competitive landscape, with medtech incumbents acquiring semiconductor-focused start-ups.

Key Report Takeaways

• By Product Type

- Diagnostic imaging accounted for 42.5% of the medical electronics market revenue in 2025, reflecting sustained hospital capital expenditure on CT and MRI upgrades.

- Wearables and implantables are projected to expand at an 11.52% CAGR through 2035, driven by RPM adoption and AI-enabled biosensors.

• By Component

- Sensors and MEMS held a 34.6% share of the medical electronics market in 2025, benefiting from miniaturization and multi-analyte integration.

- Power management ICs are gaining relevance as battery-powered wearable designs prioritize ultra-low standby draw.

• By End User

- Hospitals and clinics represented 47.9% of 2025 spending, though home-healthcare channels are forecast to post a 9.68% CAGR to 2035.

• By Geography

- North America led the medical electronics market with 35.8% of 2025 revenues.

- Asia-Pacific is forecast to register the strongest growth at 8.62% CAGR, led by India and China.

Medical Electronics Market Size and Forecast (2021–2035)

Market Research Future uses a triangulated approach that combines bottom-up revenue aggregation from OEM filings, top-down macro-indicator modeling (healthcare expenditure-to-GDP ratios, device import/export statistics) and primary interviews with procurement executives and semiconductor vendors. Historical numbers (2021-2024) are extracted from certified corporate records. Forecast predictions (2026-2035) are based on a steady CAGR, anchored to the 2026 base.