Recovered Carbon Black Market Summary

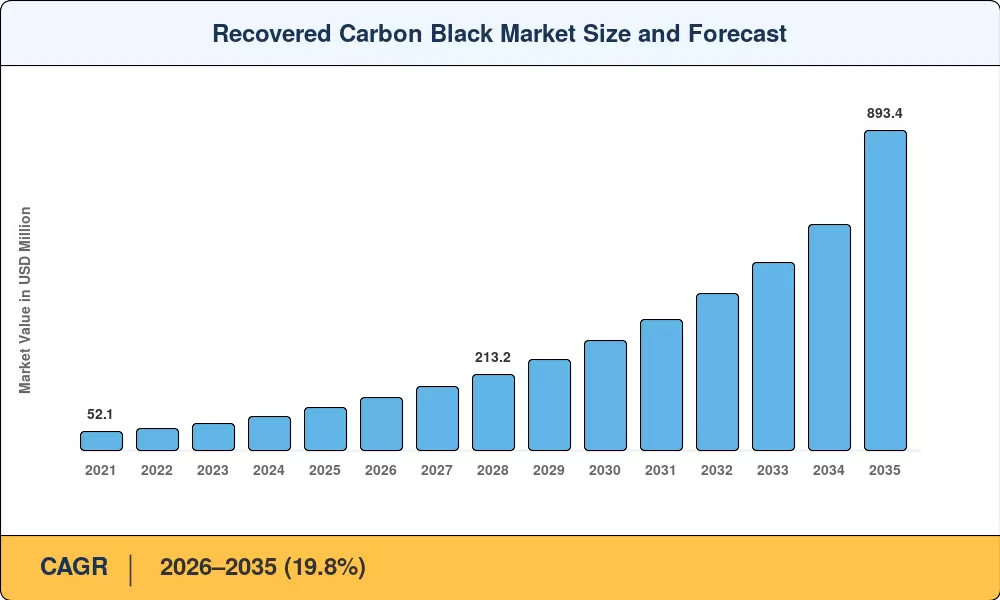

The Recovered Carbon Black Market reached an estimated 121.25 kilotons in 2025 and is projected to register 148.50 kilotons in 2026 before climbing to approximately 893.40 kilotons by 2035, reflecting a 19.8% CAGR across the forecast window. This trajectory is anchored in two converging forces: the European Union's End-of-Life Tires Directive mandating minimum recycled content in new tire compounds, and a widening cost gap between virgin carbon black—now averaging USD 1,250/ton on a delivered basis—and pyrolysis carbon black priced 20–30% lower [2]. OEM sustainability pledges from major automakers, including Michelin's target of 40% sustainable materials by 2030, are converting regulatory pressure into firm offtake contracts that de-risk capital expenditure for pyrolysis plant developers [3].

Technology transformation in the Recovered Carbon Black Market is centered around continuous pyrolysis systems that can generate ASTM-grade reclaimed carbon black in an attempt to replace the traditional landfill and incinerator disposal of end-of-life tires. Between 2023 and 2025, $1.8 billion in committed capital was announced for new and expanded pyrolysis facilities globally. Thermal cracking reactors are increasingly being coupled with advanced post-treatment units, such as pelletizing, micronizing and surface activation, to produce specialty grades for plastics compounding and conductive ink applications [4]. Gasification routes are rare but are drawing pilot-stage investment in Japan and South Korea for syngas co-production.

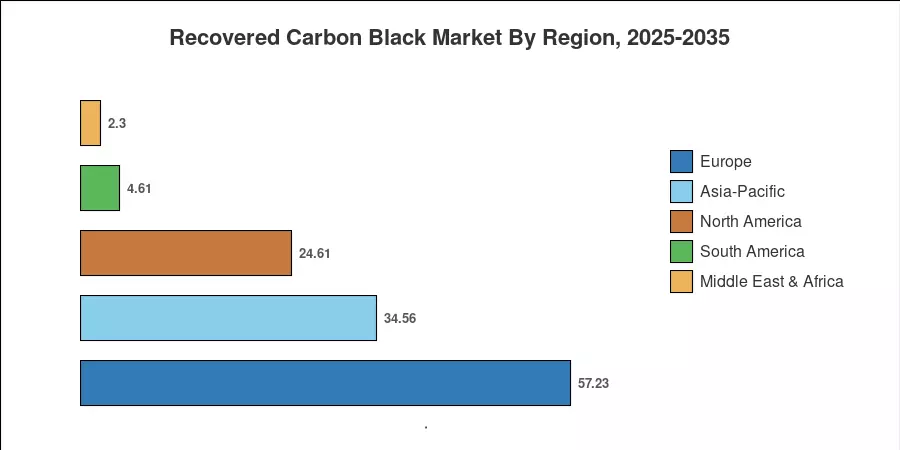

Europe, with around 47.2% of the worldwide volume, enjoys the advantage of a dense tire collecting infrastructure and advantageous Extended Producer Responsibility schemes in Germany, France and the Nordic states. North America is anticipated to be the fastest developing market with an estimated CAGR of 20.3% because to a surge of greenfield pyrolysis projects coming up in the U.S. Gulf Coast and Ontario that are scheduled to attain steady-state output by 2028. Asia-Pacific accounts for the second greatest proportion, with China leading the way as it seeks to formalize its fragmented tire recycling industry under increased enforcement of environmental legislation [5]. As circular economy materials are included in an increasing number of procurement specifications, the Recovered Carbon Black Market is positioned to move from a supply-constrained specialty to a mainstream commodity channel.

Key Report Takeaways

• By Grade

- Rubber-grade rCB accounted for 75.1% of volume in 2025, driven by tire manufacturer adoption of sustainable rubber additives in retread and new tire compounds

- Specialty/conductive-grade rCB is forecast to expand at a 21.2% CAGR through 2035, as demand for eco-friendly carbon materials in 5G shielding and EV battery components accelerates

• By Production Technology

- Pyrolysis technology controlled an estimated 95.8% of output in 2025, reinforcing its dominance in the Recovered Carbon Black Market and confirming that capacity—not demand—remains the binding constraint

- Gasification and other production technologies collectively held the remaining share but are gaining traction for syngas co-production in Asian markets

• By Application

- Tires represented approximately 76.3% of the Recovered Carbon Black Market in 2025, underpinned by OEM mandates for recycled industrial materials in tire compounds

- Plastics and other applications are expected to grow at a combined 22.5% CAGR as pyrolysis carbon black achieves parity with N600–N700 virgin grades

• By End-User Industry

- Automotive commanded the largest end-user share at roughly 77.4% in 2025

- Industrial end users are projected to expand at 20.4% CAGR through 2035 as printing, packaging, and construction sectors adopt recovered filler materials

• By Region

- Europe held 47.2% of the Recovered Carbon Black Market in 2025

- North America is expected to pace growth at 20.3% CAGR, with the U.S. and Canada leading new plant commissioning

Market Size and Forecast (2021–2035)

Market Research Future (MRFR) market sizing relies on bottom-up plant-capacity audits, along with top-down demand modeling based on tire production quantities, cross-checked with trade data, business disclosures, and regulatory filings. Historical statistics (2021-2024) are actual reported output, the 2025 base year is a blend of H1 actuals and H2 estimations, and the 2026-2035 prediction applies a calibrated compound growth trajectory that incorporates stated capacity expansions, permitting timelines and offtake agreement visibility.