Functional Water Market Summary

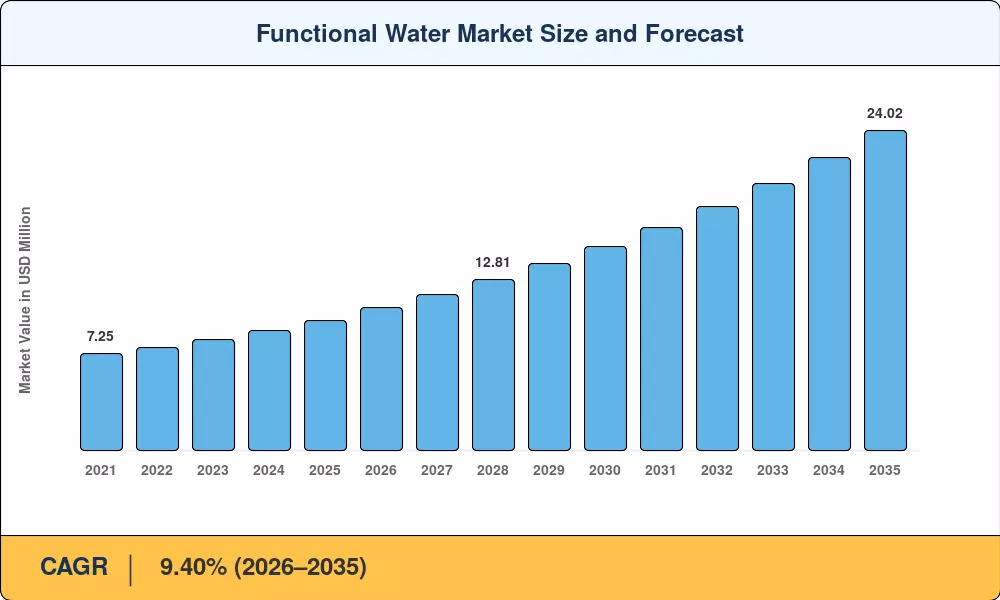

The functional water market reached USD 9.78 Billion in 2025 and is projected to grow from USD 10.70 Billion in 2026 to USD 24.02 Billion by 2035, registering a CAGR of 9.40% during the forecast period. Rising consumer preference for beverages that deliver targeted health benefits — immunity support, digestive wellness, cognitive performance — has transformed what was once a niche hydration segment into a mainstream wellness category. Government-backed preventive healthcare campaigns across North America and the EU, combined with an estimated USD 4.2 Billion in private-label functional beverage investments since 2023, have accelerated category expansion [2].

The technology transformation in the functional water market centers on advanced formulation science. Legacy single-nutrient waters are giving way to multi-functional blends featuring electrolyte and vitamin-infused water, adaptogenic botanicals, and bioavailable mineral complexes. Hydrogen-enriched water has emerged as a high-growth niche backed by clinical research into antioxidant and anti-inflammatory properties [3]. Brand owners are leveraging cold-fill aseptic processing and microencapsulation technologies to preserve ingredient efficacy without artificial preservatives, responding to clean-label demand that now influences over 62% of purchase decisions in the functional beverage aisle [4].

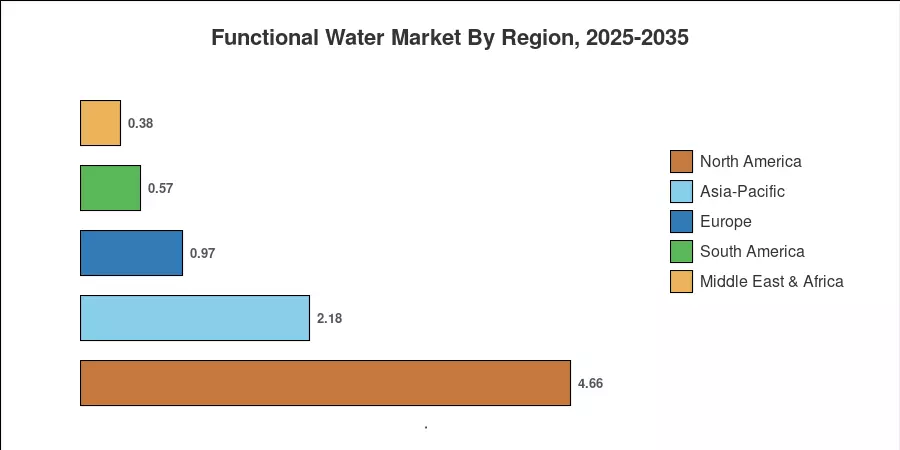

North America commands roughly 47.6% of the global functional water market revenue, driven by deep retail penetration and robust DTC infrastructure. Europe is the fastest-growing region at an estimated 9.9% CAGR through 2035, propelled by tightening sugar-tax regulations that redirect consumption toward flavored and enhanced water alternatives Asia-Pacific holds the second-largest share, where alkaline ionized water enjoys a strong cultural affinity in Japan and South Korea. As smart water health benefits gain mainstream visibility through social media and influencer channels, the global functional water market is poised for sustained double-digit expansion in several sub-segments through the next decade.

Key Report Takeaways

• By Product Type

- Vitamin-fortified water captured approximately 38.2% of the functional water market share in 2025, reflecting strong consumer appetite for daily-dose convenience beverages that deliver electrolyte and vitamin infused water benefits in a single serving

- Electrolyte/mineral water is forecast to grow at a 10.6% CAGR through 2035, supported by sports nutrition crossover and post-workout hydration trends

- Protein-infused water is carving a niche within the functional water market, particularly among gym-going demographics seeking low-calorie recovery options

• By Distribution Channel

- Supermarkets and hypermarkets accounted for USD 5.85 Billion in functional water sales during 2025, anchored by dedicated wellness aisles and private-label programs

- Online retail channels are projected to register the fastest CAGR of 10.8% through 2035, benefiting from subscription models and direct-to-consumer flavored and enhanced water brands

• By Region

- North America dominated the functional water market with a 47.6% revenue share in 2025

- Europe is forecast to expand at a 9.9% CAGR from 2026 to 2035, with alkaline ionized water gaining traction in Germany and the Nordic countries

Functional Water Market Size and Forecast (2021–2035)

MRFR's market sizing integrates top-down revenue tracking from 85+ manufacturer filings with bottom-up retail audit data across 32 countries. Historical figures (2021–2024) are validated against trade association reports, while the forecast (2026–2035) applies econometric modeling calibrated to category-specific demand elasticities and regulatory scenarios.