Immunofluorescence Assay Market Summary

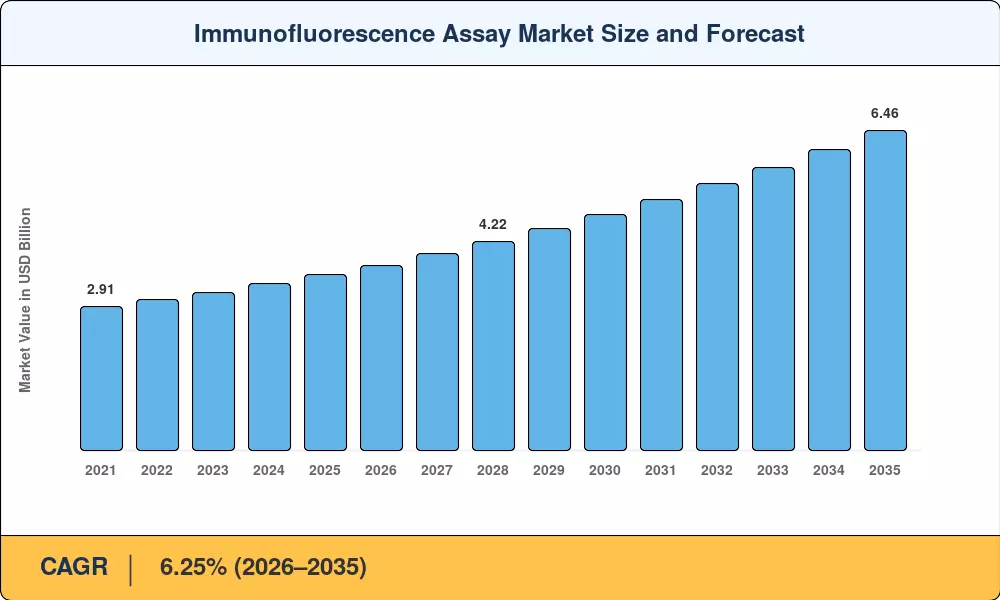

The Global Immunofluorescence Assay Market size was valued at USD 3.55 Billion in 2025, and the market is projected to grow from USD 3.74 Billion in 2026 to USD 6.46 Billion by 2035, registering a CAGR of 6.25% during the forecast period 2026–2035. Two catalysts sit behind that trajectory: the FDA's 2024 final rule on laboratory-developed test (LDT) oversight, which is pushing laboratories toward validated commercial assay kits [1], and a surge in government-backed infectious-disease surveillance budgets that exceeded USD 4.2 billion globally in 2024 [2]. Together, these forces are pulling the Immunofluorescence Assay Market away from fragmented, in-house workflows and toward standardized, commercially supported platforms.

A technology transition is reshaping the competitive landscape. Legacy manual fluorescence microscopes — instruments that have anchored pathology labs for decades — are giving way to AI-enabled digital pathology systems capable of automated pattern recognition and whole-slide imaging. The European Commission's Horizon Europe program allocated over EUR 380 million to digital diagnostics research between 2023 and 2025, accelerating adoption across EU reference laboratories [3]. This shift is not merely incremental; it redefines throughput benchmarks and positions the Immunofluorescence Assay Market at the intersection of diagnostics and computational biology.

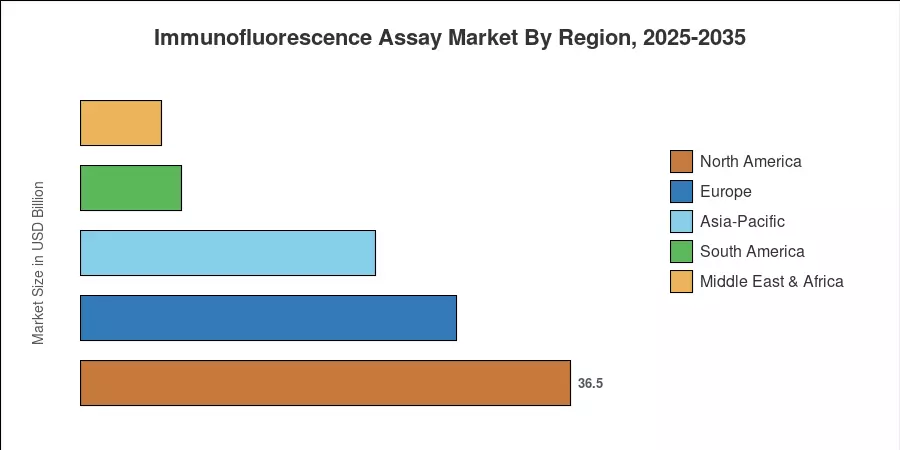

North America held approximately 36.5% of the Immunofluorescence Assay Market in 2025, anchored by the United States' dense network of CLIA-certified laboratories and robust reimbursement pathways. Asia-Pacific is the fastest-growing region, projected to expand at a 7.65% CAGR through 2035, fueled by China's hospital modernization campaign and India's Ayushman Bharat laboratory expansion. Europe commands the second-largest share at roughly 28%, with Germany and France leading in autoimmune diagnostics adoption. The decade ahead will reward vendors that pair reagent quality with digital integration and regulatory agility.

Key Report Takeaways

• By Product

- Reagents and kits captured roughly 56.5% of the Immunofluorescence Assay Market revenue in 2025, reflecting the consumables-driven recurring-revenue model that dominates clinical laboratory procurement.

- Instruments are forecast to register the highest segment CAGR at 7.35% through 2035, driven by capital-equipment replacement cycles and the shift toward automated slide-processing platforms.

• By Application

- Infectious-disease testing accounted for approximately 41.5% of the Immunofluorescence Assay Market in 2025, supported by post-pandemic respiratory pathogen surveillance mandates.

- Cancer diagnostics and research represent the fastest-growing application, with a projected 7.10% CAGR through 2035 as companion-diagnostic protocols expand.

• By Region

- North America maintained its dominant position in the Immunofluorescence Assay Market, with a 36.5% share in 2025 underpinned by payer coverage and high test volumes.

- Asia-Pacific is set to grow at a 7.65% CAGR, the quickest of any region, driven by large-scale public-health infrastructure investment across China and India.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology integrates bottom-up revenue modeling from over 60 reagent and instrument manufacturers, cross-referenced against publicly reported laboratory volumes, import/export databases, and payer claims data. Historical values (2021–2024) rely on audited financial disclosures and verified procurement records, while the forecast period (2026–2035) applies a demand-supply equilibrium model calibrated to macroeconomic indicators, disease-prevalence trends, and regulatory timelines.