Digital Accessibility Software Market Summary

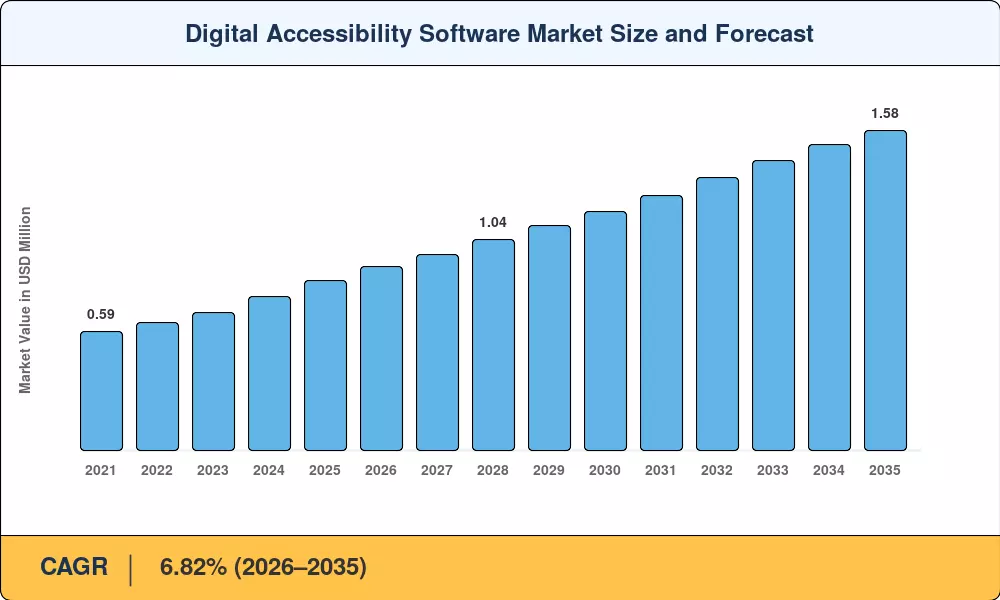

The digital accessibility software market reached an estimated USD 0.84 billion in 2025, with forecasts projecting the sector to grow from USD 0.91 billion in 2026 to USD 1.58 billion by 2035, registering a CAGR of 6.82% during the forecast period. Enforcement of the European Accessibility Act in June 2025 and the ISO adoption of WCAG 2.2 standards in October 2025 have reshaped procurement priorities across both public and private sectors, converting accessible design from a compliance checkbox into a revenue-qualifying criterion [2]. Subscription-based conformance monitoring has replaced periodic audits as the dominant delivery model, driven by ESG reporting mandates and government tender requirements that demand continuous proof of accessibility compliance.

Legacy manual audit workflows are giving way to cloud-native automated accessibility testing platforms that embed scans directly into CI/CD pipelines. AI-powered engines now propose real-time remediation for WCAG 2.1 web accessibility compliance tools violations, cutting fix cycles from weeks to hours [3]. Enterprise spending on ADA compliance digital accessibility solutions surpassed USD 320 million in North America alone during 2024, reflecting sustained investment in both tooling and human audit validation layers [4].

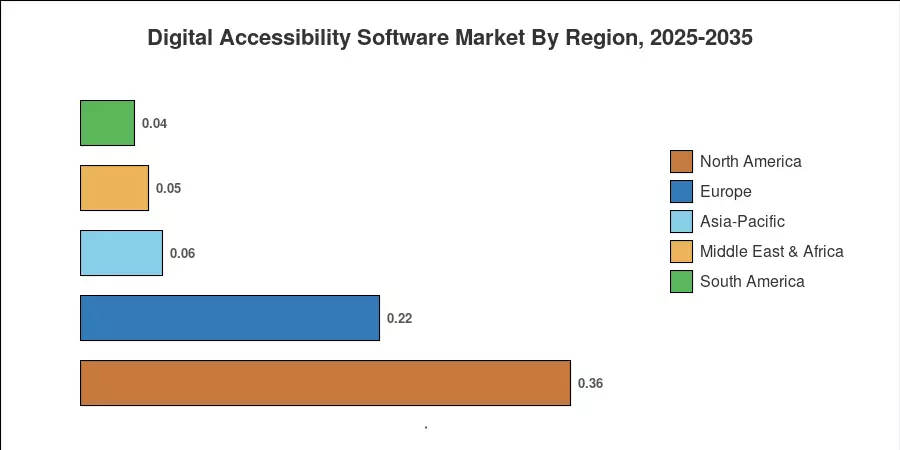

North America commands the largest share of the digital accessibility software market at approximately 42.6% of 2025 revenue, anchored by Section 508 mandates and active DOJ enforcement actions [5]. Asia-Pacific is the fastest-growing region, forecast to expand at a 7.72% CAGR as Japan, India, and Australia align private-sector procurement with mandatory accessibility guidelines Europe holds the second-largest position, with the EU Accessibility Act creating a unified compliance baseline across 27 member states. The convergence of regulatory pressure and AI-driven tooling positions this market for sustained double-digit growth in select verticals through 2035.

Key Report Takeaways

• By Type

- Website accessibility platforms captured roughly 38.7% of the digital accessibility software market share in 2025, driven by demand for WCAG 2.1 web accessibility compliance tools across enterprise portals and e-commerce storefronts

- Mobile and app accessibility suites are forecast to grow at a 7.92% CAGR through 2035, fueled by screen reader compatible digital content tools adoption on iOS and Android ecosystems

- Automated scan and audit tools accounted for approximately USD 0.21 billion in 2025 revenue, reflecting enterprise migration toward automated accessibility testing platforms

• By Deployment Mode

- Cloud-based solutions commanded 68.4% of 2025 deployments within the digital accessibility software market, as SaaS delivery enables continuous monitoring and real-time remediation

- Small and medium enterprises are advancing at a 7.08% CAGR, adopting accessible PDF and document creation tools to meet supplier diversity requirements from large buyers

• By Organization Size

- Small and medium enterprises are advancing at a 7.08% CAGR, adopting accessible PDF and document creation tools to meet supplier diversity requirements from large buyers

• By End-User Industry

- E-commerce and retail led end-user spending with 24.3% of 2025 revenue, as ADA compliance digital accessibility solutions become prerequisites for checkout flow certification

- The government and public sector segment is on track for a 7.93% CAGR through 2035, with Section 508 refreshes and EU procurement directives expanding scope

- Asia-Pacific is forecast to reach USD 0.38 billion by 2035, led by Japan's JIS X 8341 enforcement and India's Rights of Persons with Disabilities Act mandates

• By Region

- Asia-Pacific is forecast to reach USD 0.38 billion by 2035, led by Japan's JIS X 8341 enforcement and India's Rights of Persons with Disabilities Act mandates

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s proprietary estimation framework triangulates bottom-up vendor revenue data, top-down regulatory spending analysis, and demand-side enterprise surveys across 28 countries. Historical figures (2021–2024) draw on verified financial disclosures; the 2025 base year reflects preliminary full-year estimates; and the forecast period (2026–2035) applies a calibrated compound growth model adjusted for policy milestones and technology adoption curves.

.webp?v=1781696631)