Customer Analytics Market Summary

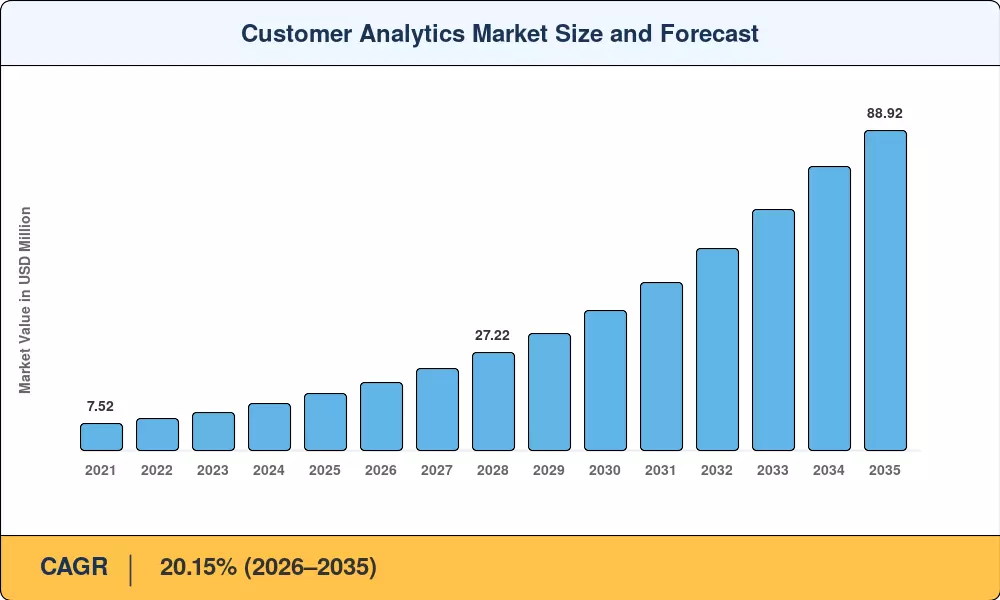

The Customer Analytics Market reached an estimated USD 15.86 billion in 2025, with the forecast period beginning at USD 18.85 billion in 2026 and projected to climb to USD 88.92 billion by 2035, reflecting a compound annual growth rate of 20.15% across the 2026–2035 window. Two catalysts are accelerating adoption: enterprises now allocate over 65% of their marketing technology budgets toward analytics-first platforms, and stricter data-governance mandates such as the EU Digital Markets Act are forcing brands to build first-party data capabilities rather than rely on third-party cookies [2]. Customer Analytics Market growth is anchored in a fundamental business shift — organizations that once measured campaign ROI quarterly now demand real-time customer behavior analysis delivered within minutes.

Legacy batch-processing data warehouses and static CRM dashboards are giving way to cloud-native analytics stacks powered by AI-driven customer segmentation tools and streaming-data architectures. According to IDC, global spending on customer-experience analytics platforms surpassed USD 9.4 billion in 2024, up 22% year over year. Predictive customer lifetime value modeling has moved from experimental pilot to production deployment inside Fortune 500 marketing operations, with Salesforce reporting that 58% of enterprise clients activated at least one predictive scoring module in 2024 [4].

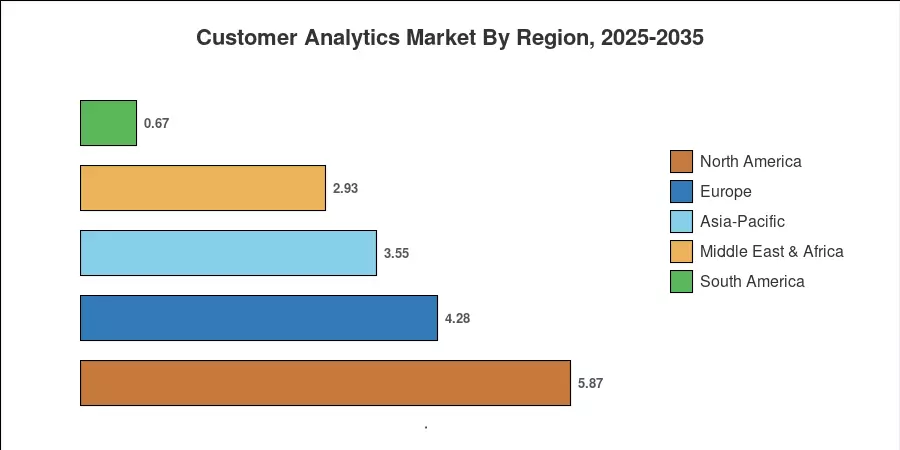

North America commands roughly 37% of the global Customer Analytics Market revenue, backed by Silicon Valley platform economics and early enterprise AI adoption Asia-Pacific is the fastest-growing region at a projected CAGR exceeding 22%, driven by India's digital-payments boom and China's super-app ecosystems. Europe holds the second-largest share, near 27%, underpinned by GDPR-driven demand for a compliant personalization engine for customer data solutions. As omnichannel commerce matures, the Customer Analytics Market is poised to become the backbone of every customer-facing function from acquisition through retention.

Key Report Takeaways

• By Deployment

- Cloud-based deployments captured approximately 65% of Customer Analytics Market revenue in 2025, reflecting the dominance of scalable, pay-as-you-go architectures that minimize capital expenditure

• By Solution

- Cloud-based deployments captured approximately 65% of Customer Analytics Market revenue in 2025, reflecting the dominance of scalable, pay-as-you-go architectures that minimize capital expenditure

- AI-augmented analytics modules are forecast to grow at a CAGR of 25.6% through 2035, making them the fastest-expanding solution category as enterprises invest in customer churn prediction analytics

- Dashboard and reporting tools accounted for USD 4.48 billion in 2025 revenue, serving as the entry point for organizations beginning their analytics journey

• By Organization Size

- Large enterprises controlled roughly 67% of the Customer Analytics Market in 2025, leveraging dedicated data-science teams and multi-year platform contracts

- Small and medium enterprises are growing at an annual rate near 20.8%, enabled by self-service AI-driven customer segmentation tools delivered through cloud marketplaces

• By Service

- Large enterprises controlled roughly 67% of the Customer Analytics Market in 2025, leveraging dedicated data-science teams and multi-year platform contracts

- Managed services represented approximately 58% of service revenue in 2025, as organizations outsource model maintenance and data-pipeline operations

- Small and medium enterprises are growing at an annual rate near 20.8%, enabled by self-service AI-driven customer segmentation tools delivered through cloud marketplaces

• By Region

- North America leads the Customer Analytics Market at roughly 37% global share, driven by mature digital advertising ecosystems and high per-capita martech spending

- Asia-Pacific is projected to register the highest CAGR of approximately 22.4%, fueled by rapid mobile-commerce adoption in India and Southeast Asia

- Europe contributed an estimated USD 4.28 billion in 2025, with GDPR compliance fueling demand for privacy-centric analytics platforms

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up revenue modeling from vendor disclosures, top-down cross-referencing against enterprise IT spending benchmarks from IDC and Gartner, and primary interviews with 120+ analytics decision-makers across verticals.