-

EXECUTIVE SUMMARY

-

MARKET INTRODUCTION

-

DEFINITION

-

SCOPE OF THE STUDY

-

RESEARCH OBJECTIVE

-

MARKET STRUCTURE

-

RESEARCH METHODOLOGY

-

OVERVIEW

-

DATA FLOW

- Data Mining Process

-

PURCHASED DATABASE:

-

SECONDARY SOURCES:

- Secondary Research data flow:

-

PRIMARY RESEARCH:

- Primary Research Data Flow:

- Primary Research: Number of Interviews conducted

-

APPROACHES FOR MARKET SIZE ESTIMATION:

- Revenue Analysis Approach

-

DATA FORECASTING

- Data forecasting Type

-

DATA MODELING

- microeconomic factor analysis:

- Data modeling:

-

TEAMS AND ANALYST CONTRIBUTION

-

MARKET DYNAMICS

-

INTRODUCTION

-

DRIVERS

- Rising Cancer & Chronic Disease Prevalence

- Growing Adoption of Targeted Therapies and Precision Medicine

- Technological Advances

- Increasing Drug–Diagnostic Co-Development & Regulatory Approvals

-

RESTRAINTS

- High Cost & Capital Investment for CDx Development and Testing

- Regulatory Complexity and Varied Approval Pathways

- Limited Reimbursement, Uneven Access & Awareness

-

OPPORTUNITIES

- Expansion beyond oncology into other therapeutic areas

- Growth in bioinformatics, software & services supporting CDx

-

MARKET FACTOR ANALYSIS

-

PORTER'S FIVE FORCES MODEL

- Threat of New Entrants

- BARGAINING POWER OF SUPPLIERS

- Threat of Substitutes

- Bargaining Power of Buyers

- Intensity of Rivalry

-

IMPACT ANALYSIS OF COVID-19

- Disruption in Diagnostic Testing and Oncology Procedures

- Supply Chain Disruptions

- Changes in Patient Behavior and Clinical Workflows

- Impact on R&D and Innovation

-

COMPANION DIAGNOSTIC ANALYSIS FOR KEYTRUDA, TECENTRIQ, AND LIBTAYO

-

PDL1 SALES DATA GLOBALLY, 2019-2035 (USD MILLION)

-

MARKET SHARE BY DRUG GLOBAL, REGIONAL AND COUNTRY LEVEL 2024 (%)

- GLOBAL MARKET SHARE BY DRUG, 2024 (%)

- North America MARKET SHARE BY DRUG, 2024 (%)

- Europe MARKET SHARE BY DRUG, 2024 (%)

- ASIA-PACIFIC MARKET SHARE BY DRUG, 2024 (%)

-

MARKET SHARE BY CLONE GLOBAL, REGIONAL AND COUNTRY LEVEL 2024 (%)

- GLOBAL MARKET SHARE BY clone, 2024 (%)

- North America MARKET SHARE BY CLONE, 2024 (%)

- EUROPE MARKET SHARE BY CLONE, 2024 (%)

- ASIA-PACIFIC MARKET SHARE BY CLONE, 2024 (%)

-

QUALITATIVE ANALYSIS OF PD-L1 TESTING CUT-OFFS

-

PDL1 SALES DATA GLOBALLY, (2019-2035), BY APPLICATION

-

PRICING ANALYSIS, 2024 (USD)

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY TEST TYPE

-

OVERVIEW

-

HER2 TESTING

-

PD-1 TESTING

-

EGFR MUTATION TESTING

-

ALK REARRANGEMENT TESTING

-

OTHERS

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY PRODUCTS & SERVICES

-

OVERVIEW

-

ASSAYS, REAGENTS & KITS

-

INSTRUMENTS/SYSTEMS

-

SOFTWARE & SERVICES

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY

-

OVERVIEW

-

POLYMERASE CHAIN REACTION (PCR)

-

NEXT-GENERATION SEQUENCING (NGS)

-

IMMUNOHISTOCHEMISTRY (IHC)

-

FLUORESCENCE IN-SITU HYBRIDIZATION (FISH)

-

OTHERS

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY INDICATION

-

OVERVIEW

-

CANCER

-

NEUROLOGICAL DISORDERS

-

CARDIOVASCULAR DISORDERS

-

INFECTIOUS DISEASES

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY END USER

-

OVERVIEW

-

BIOPHARMACEUTICAL AND BIOTECHNOLOGY COMPANIES

-

CROS AND CDMOS

-

OTHERS

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY REGION

-

OVERVIEW

-

NORTH AMERICA

- US

- CANADA

-

EUROPE

- GERMANY

- france

- UK

- ITALY

- Spain

- Denmark

- Finland

- Iceland

- Norway

- Sweden

- Rest of Europe

-

ASIA-PACIFIC

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

-

COMPETITIVE LANDSCAPE

-

INTRODUCTION

-

MARKET SHARE ANALYSIS, 2024

-

COMPETITOR DASHBOARD

-

PUBLIC PLAYERS STOCK SUMMARY

-

COMPARATIVE ANALYSIS: KEY PLAYERS FINANCIAL

-

KEY DEVELOPMENTS & GROWTH STRATEGIES

- Product/service launch

- acquisition

- Accreditation

- Collaboration/ Partnership

-

COMPANY PROFILES

-

QIAGEN

- COMPANY OVERVIEW

- FINANCIAL OVERVIEW

- products OFFERed

- KEY DEVELOPMENTS

- SWOT ANALYSIS

- KEY STRATEGIES

- products OFFERed

- SWOT ANALYSIS

-

BIOMÉRIEUX

- COMPANY OVERVIEW

- FINANCIAL OVERVIEW

- products OFFERed

- KEY DEVELOPMENTS

- SWOT ANALYSIS

- KEY STRATEGIES

-

LEICA BIOSYSTEMS NUSSLOCH GMBH

- COMPANY OVERVIEw

- FINANCIAL OVERVIEW

- products OFFERed

- KEY DEVELOPMENTS

- KEY STRATEGIES

-

NG BIOTECH

- COMPANY OVERVIEW

- FINANCIAL OVERVIEW

- products OFFERed

- KEY STRATEGIES

-

THERMO FISHER SCIENTIFIC INC.

- COMPANY OVERVIEW

- FINANCIAL OVERVIEW

- products OFFERed

- KEY DEVELOPMENTs

- SWOT ANALYSIS

- Key Strategy

-

ILLUMINA, INC.

- COMPANY OVERVIEW

- FINANCIAL OVERVIEW

- PRODUCTS OFFERed

- KEY DEVELOPMENTS

- KEY STRATEGIES

-

AGILENT TECHNOLOGIES, INC.

- COMPANY OVERVIEW

- FINANCIAL OVERVIEW

- PRODUCTS OFFERED

- KEY DEVELOPMENTS

- SWOT ANALYSIS

- KEY STRATEGIES

-

FOUNDATION MEDICINE INC. (F. HOFFMANN-LA ROCHE LTD )

- COMPANY OVERVIEW

- FINANCIAL OVERVIEW

- productS OFFERED

- KEY DEVELOPMENTs

- KEY STRATEGIES

-

MYRIAD GENETICS, INC.

- COMPANY OVERVIEW

- FINANCIAL OVERVIEW

- productS OFFERED

- KEY DEVELOPMENTs

- KEY STRATEGIES

-

DATA CITATIONS

-

-

LIST OF TABLES

-

QFD MODELING FOR MARKET SHARE ASSESSMENT

-

COMPANION DIAGNOSTIC ANALYSIS FOR KEYTRUDA, TECENTRIQ, AND LIBTAYO

-

PDL1 SALES DATA GLOBALLY, 2019-2035 (USD MILLION)

-

PD-L1 TESTING CUT-OFFS

-

PDL1 SALES DATA GLOBALLY, (2019-2035), BY APPLICATION

-

PRICING ANALYSIS, 2024 (USD)

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2024 & 2035 (USD MILLION)

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2024 & 2035 (TEST VOLUME)

-

GLOBAL COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TEST TYPE, 2024 & 2035 (USD MILLION)

-

GLOBAL COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TEST TYPE, 2024 & 2035 (TEST VOLUME)

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY PRODUCT & SERVICES, 2024 & 2035 (USD MILLION)

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2024 & 2035 (USD MILLION)

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2024 & 2035 (USD MILLION)

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY END USER, 2024 & 2035 (USD MILLION)

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY REGION, 2019-2035 (USD MILLION)

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY REGION, 2019-2035 (TEST VOLUME)

-

NORTH AMERICA COMPANION DIAGNOSTICS MARKET, BY COUNTRY, 2019-2035 (USD MILLION)

-

NORTH AMERICA: COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-2035 (USD MILLION)

-

NORTH AMERICA: COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-2035 (TEST VOLUME)

-

NORTH AMERICA: COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-2035 (USD MILLION)

-

NORTH AMERICA: COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-2035 (TEST VOLUME)

-

NORTH AMERICA: COMPANION DIAGNOSTICS MARKET, BY PRODUCT & SERVICES, 2019-2035 (USD MILLION)

-

NORTH AMERICA: COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-2035 (USD MILLION)

-

NORTH AMERICA: COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-2035 (USD MILLION)

-

NORTH AMERICA: COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-2035 (USD MILLION)

-

US: COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-2035 (USD MILLION)

-

US: COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-2035 (TEST VOLUME)

-

US: COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-2035 (USD MILLION)

-

US: COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-2035 (TEST VOLUME)

-

US: COMPANION DIAGNOSTICS MARKET, BY PRODUCT & SERVICES, 2019-2035 (USD MILLION)

-

US: COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-2035 (USD MILLION)

-

US: COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-2035 (USD MILLION)

-

US: COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-2035 (USD MILLION)

-

CANADA: COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-2035 (USD MILLION)

-

CANADA: COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-2035 (TEST VOLUME)

-

CANADA: COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-2035 (USD MILLION)

-

CANADA: COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-2035 (TEST VOLUME)

-

CANADA: COMPANION DIAGNOSTICS MARKET, BY PRODUCT & SERVICES, 2019-2035 (USD MILLION)

-

CANADA: COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-2035 (USD MILLION)

-

CANADA: COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-2035 (USD MILLION)

-

CANADA: COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-2035 (USD MILLION)

-

EUROPE: COMPANION DIAGNOSTICS MARKET, BY COUNTRY, 2019-2035 (USD MILLION)

-

EUROPE COMPANION DIAGNOSTICS MARKET, BY COUNTRY, 2019-H-2035 (TEST VOLUME)

-

EUROPE COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (USD MILLION)

-

EUROPE COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (TEST VOLUME)

-

EUROPE COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (USD MILLION)

-

EUROPE COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (TEST VOLUME)

-

EUROPE COMPANION DIAGNOSTICS MARKET, BYPRODUCT & SERVICES, 2019-H-2035 (USD MILLION)

-

EUROPE COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-H-2035 (USD MILLION)

-

EUROPE COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-H-2035 (USD MILLION)

-

EUROPE COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-H-2035 (USD MILLION)

-

GERMANY COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (USD MILLION)

-

GERMANY COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (TEST VOLUME)

-

GERMANY COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (USD MILLION)

-

GERMANY COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (TEST VOLUME)

-

GERMANY COMPANION DIAGNOSTICS MARKET, BYPRODUCT & SERVICES, 2019-H-2035 (USD MILLION)

-

GERMANY COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-H-2035 (USD MILLION)

-

GERMANY COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-H-2035 (USD MILLION)

-

GERMANY COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-H-2035 (USD MILLION)

-

FRANCE COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (USD MILLION)

-

FRANCE COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (TEST VOLUME)

-

FRANCE COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (USD MILLION)

-

FRANCE COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (TEST VOLUME)

-

FRANCE COMPANION DIAGNOSTICS MARKET, BYPRODUCT & SERVICES, 2019-H-2035 (USD MILLION)

-

FRANCE COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-H-2035 (USD MILLION)

-

FRANCE COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-H-2035 (USD MILLION)

-

FRANCE COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-H-2035 (USD MILLION)

-

UK COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (USD MILLION)

-

UK COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (TEST VOLUME)

-

UK COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (USD MILLION)

-

UK COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (TEST VOLUME)

-

UK COMPANION DIAGNOSTICS MARKET, BYPRODUCT & SERVICES, 2019-H-2035 (USD MILLION)

-

UK COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-H-2035 (USD MILLION)

-

UK COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-H-2035 (USD MILLION)

-

UK COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-H-2035 (USD MILLION)

-

ITALY COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (USD MILLION)

-

ITALY COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (TEST VOLUME)

-

ITALY COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (USD MILLION)

-

ITALY COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (TEST VOLUME)

-

ITALY COMPANION DIAGNOSTICS MARKET, BYPRODUCT & SERVICES, 2019-H-2035 (USD MILLION)

-

ITALY COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-H-2035 (USD MILLION)

-

ITALY COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-H-2035 (USD MILLION)

-

ITALY COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-H-2035 (USD MILLION)

-

SPAIN COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (USD MILLION)

-

SPAIN COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (TEST VOLUME)

-

SPAIN COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (USD MILLION)

-

SPAIN COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (TEST VOLUME)

-

SPAIN COMPANION DIAGNOSTICS MARKET, BYPRODUCT & SERVICES, 2019-H-2035 (USD MILLION)

-

SPAIN COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-H-2035 (USD MILLION)

-

SPAIN COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-H-2035 (USD MILLION)

-

SPAIN COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-H-2035 (USD MILLION)

-

DENMARK COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (USD MILLION)

-

DENMARK COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (TEST VOLUME)

-

DENMARK COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (USD MILLION)

-

DENMARK COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (TEST VOLUME)

-

DENMARK COMPANION DIAGNOSTICS MARKET, BYPRODUCT & SERVICES, 2019-H-2035 (USD MILLION)

-

DENMARK COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-H-2035 (USD MILLION)

-

DENMARK COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-H-2035 (USD MILLION)

-

DENMARK COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-H-2035 (USD MILLION)

-

FINLAND COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (USD MILLION)

-

FINLAND COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (TEST VOLUME)

-

FINLAND COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (USD MILLION)

-

FINLAND COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (TEST VOLUME)

-

FINLAND COMPANION DIAGNOSTICS MARKET, BYPRODUCT & SERVICES, 2019-H-2035 (USD MILLION)

-

FINLAND COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-H-2035 (USD MILLION)

-

FINLAND COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-H-2035 (USD MILLION)

-

FINLAND COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-H-2035 (USD MILLION)

-

ICELAND COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (USD MILLION)

-

ICELAND COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (TEST VOLUME)

-

ICELAND COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (USD MILLION)

-

ICELAND COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (TEST VOLUME)

-

ICELAND COMPANION DIAGNOSTICS MARKET, BYPRODUCT & SERVICES, 2019-H-2035 (USD MILLION)

-

ICELAND COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-H-2035 (USD MILLION)

-

ICELAND COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-H-2035 (USD MILLION)

-

ICELAND COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-H-2035 (USD MILLION)

-

NORWAY COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (USD MILLION)

-

NORWAY COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (TEST VOLUME)

-

NORWAY COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (USD MILLION)

-

NORWAY COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (TEST VOLUME)

-

NORWAY COMPANION DIAGNOSTICS MARKET, BYPRODUCT & SERVICES, 2019-H-2035 (USD MILLION)

-

NORWAY COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-H-2035 (USD MILLION)

-

NORWAY COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-H-2035 (USD MILLION)

-

NORWAY COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-H-2035 (USD MILLION)

-

SWEDEN COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (USD MILLION)

-

SWEDEN COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (TEST VOLUME)

-

SWEDEN COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (USD MILLION)

-

SWEDEN COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (TEST VOLUME)

-

SWEDEN COMPANION DIAGNOSTICS MARKET, BYPRODUCT & SERVICES, 2019-H-2035 (USD MILLION)

-

SWEDEN COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-H-2035 (USD MILLION)

-

SWEDEN COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-H-2035 (USD MILLION)

-

SWEDEN COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-H-2035 (USD MILLION)

-

REST OF EUROPE COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (USD MILLION)

-

REST OF EUROPE COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-H-2035 (TEST VOLUME)

-

REST OF EUROPE COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (USD MILLION)

-

REST OF EUROPE COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (TEST VOLUME)

-

REST OF EUROPE COMPANION DIAGNOSTICS MARKET, BYPRODUCT & SERVICES, 2019-H-2035 (USD MILLION)

-

REST OF EUROPE COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-H-2035 (USD MILLION)

-

REST OF EUROPE COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-H-2035 (USD MILLION)

-

REST OF EUROPE COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-H-2035 (USD MILLION)

-

ASIA-PACIFIC COMPANION DIAGNOSTICS MARKET, BY COUNTRY, 2019-2035 (USD MILLION)

-

ASIA-PACIFIC COMPANION DIAGNOSTICS MARKET, BY COUNTRY, 2019-2035 (TEST VOLUME)

-

ASIA-PACIFIC COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-2035 (USD MILLION)

-

ASIA-PACIFIC COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-2035 (TEST VOLUME)

-

ASIA-PACIFIC COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING , BY TYPE, 2019-H-2035 (USD MILLION)

-

ASIA-PACIFIC COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (TEST VOLUME)

-

ASIA-PACIFIC COMPANION DIAGNOSTICS MARKET, BYPRODUCT & SERVICES, 2019-H-2035 (USD MILLION)

-

ASIA-PACIFIC COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-H-2035 (USD MILLION)

-

ASIA-PACIFIC COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-H-2035 (USD MILLION)

-

ASIA-PACIFIC COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-H-2035 (USD MILLION)

-

INDIA COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-2035 (USD MILLION)

-

INDIA COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-2035 (TEST VOLUME)

-

INDIA COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING , BY TYPE, 2019-H-2035 (USD MILLION)

-

INDIA COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (TEST VOLUME)

-

INDIA COMPANION DIAGNOSTICS MARKET, BYPRODUCT & SERVICES, 2019-H-2035 (USD MILLION)

-

INDIA COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-H-2035 (USD MILLION)

-

INDIA COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-H-2035 (USD MILLION)

-

INDIA COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-H-2035 (USD MILLION)

-

JAPAN COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-2035 (USD MILLION)

-

JAPAN COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-2035 (TEST VOLUME)

-

JAPAN COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING , BY TYPE, 2019-H-2035 (USD MILLION)

-

JAPAN COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (TEST VOLUME)

-

JAPAN COMPANION DIAGNOSTICS MARKET, BYPRODUCT & SERVICES, 2019-H-2035 (USD MILLION)

-

JAPAN COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-H-2035 (USD MILLION)

-

JAPAN COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-H-2035 (USD MILLION)

-

JAPAN COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-H-2035 (USD MILLION)

-

SOUTH KOREA COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-2035 (USD MILLION)

-

SOUTH KOREA COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-2035 (TEST VOLUME)

-

SOUTH KOREA COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING , BY TYPE, 2019-H-2035 (USD MILLION)

-

SOUTH KOREA COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (TEST VOLUME)

-

SOUTH KOREA COMPANION DIAGNOSTICS MARKET, BYPRODUCT & SERVICES, 2019-H-2035 (USD MILLION)

-

SOUTH KOREA COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-H-2035 (USD MILLION)

-

SOUTH KOREA COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-H-2035 (USD MILLION)

-

SOUTH KOREA COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-H-2035 (USD MILLION)

-

AUSTRALIA COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-2035 (USD MILLION)

-

AUSTRALIA COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-2035 (TEST VOLUME)

-

AUSTRALIA COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (USD MILLION)

-

AUSTRALIA COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (TEST VOLUME)

-

AUSTRALIA COMPANION DIAGNOSTICS MARKET, BYPRODUCT & SERVICES, 2019-H-2035 (USD MILLION)

-

AUSTRALIA COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-H-2035 (USD MILLION)

-

AUSTRALIA COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-H-2035 (USD MILLION)

-

AUSTRALIA COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-H-2035 (USD MILLION)

-

REST OF ASIA-PACIFIC COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-2035 (USD MILLION)

-

REST OF ASIA-PACIFIC COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2019-2035 (TEST VOLUME)

-

REST OF ASIA-PACIFIC COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING , BY TYPE, 2019-H-2035 (USD MILLION)

-

REST OF ASIA-PACIFIC COMPANION DIAGNOSTICS MARKET, FOR PD-1 TESTING, BY TYPE, 2019-H-2035 (TEST VOLUME)

-

REST OF ASIA-PACIFIC COMPANION DIAGNOSTICS MARKET, BYPRODUCT & SERVICES, 2019-H-2035 (USD MILLION)

-

REST OF ASIA-PACIFIC COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2019-H-2035 (USD MILLION)

-

REST OF ASIA-PACIFIC COMPANION DIAGNOSTICS MARKET, BY INDICATION, 2019-H-2035 (USD MILLION)

-

REST OF ASIA-PACIFIC COMPANION DIAGNOSTICS MARKET, BY END USER, 2019-H-2035 (USD MILLION)

-

PRODUCT/SERVICE LAUNCH

-

ACQUISITION/EXPANSION

-

ACCREDITATION

-

COLLABORATION/ PARTNERSHIP

-

QIAGEN: PRODUCTS AND SERVICES OFFERED

-

QIAGEN: KEY DEVELOPMENTS

-

BIO-TECHNE: PRODUCTS AND SERVICES OFFERED

-

BIOMÉRIEUX: PRODUCTS AND SERVICES OFFERED

-

BIOMÉRIEUX: PRODUCTS OFFERED

-

LEICA BIOSYSTEMS NUSSLOCH GMBH: PRODUCTS OFFERED

-

LEICA BIOSYSTEMS NUSSLOCH GMBH: PRODUCTS OFFERED

-

NG BIOTECH: PRODUCTS OFFERED

-

THERMO FISHER SCIENTIFIC INC.: PRODUCTS AND SERVICES OFFERED

-

THERMO FISHER SCIENTIFIC INC.: KEY DEVELOPMENTS

-

ILLUMINA, INC.: PRODUCTS AND SERVICES OFFERED

-

ILLUMINA, INC.: KEY DEVELOPMENTS

-

AGILENT TECHNOLOGIES, INC.: PRODUCTS AND SERVICES OFFERED

-

AGILENT TECHNOLOGIES, INC.: KEY DEVELOPMENTS

-

FOUNDATION MEDICINE INC. (F. HOFFMANN-LA ROCHE LTD ): PRODUCTS AND SERVICES OFFERED

-

MYRIAD GENETICS, INC.: PRODUCTS AND SERVICES OFFERED

-

MYRIAD GENETICS, INC.: KEY DEVELOPMENTS

-

LIST OF FIGURES

-

GLOBAL COMPANION DIAGNOSTICS MARKET: STRUCTURE

-

GLOBAL COMPANION DIAGNOSTICS MARKET: MARKET GROWTH AFFECTING FACTOR ANALYSIS (2019-2035)

-

GLOBAL COMPANION DIAGNOSTICS MARKET DRIVER: IMPACT ANALYSIS

-

GLOBAL COMPANION DIAGNOSTICS MARKET RESTRAINT: IMPACT ANALYSIS

-

PORTER'S FIVE FORCES ANALYSIS: GLOBAL COMPANION DIAGNOSTICS MARKET

-

GLOBAL MARKET SHARE ANALYSIS: BY DRUG, 2024

-

NORTH AMERICA MARKET SHARE ANALYSIS: BY DRUG, 2024

-

US MARKET SHARE ANALYSIS: BY DRUG, 2024

-

EUROPE MARKET SHARE ANALYSIS: BY DRUG, 2024

-

GERMANY MARKET SHARE ANALYSIS: BY DRUG, 2024

-

UK MARKET SHARE ANALYSIS: BY DRUG, 2024

-

ASIA-PACIFIC MARKET SHARE ANALYSIS: BY DRUG, 2024

-

CHINA MARKET SHARE ANALYSIS: BY DRUG, 2024

-

INDIA MARKET SHARE ANALYSIS: BY DRUG, 2024

-

JAPAN MARKET SHARE ANALYSIS: BY DRUG, 2024

-

GLOBAL MARKET SHARE ANALYSIS: BY CLONE, 2024

-

NORTH AMERICA MARKET SHARE ANALYSIS: BY CLONE, 2024

-

US MARKET SHARE ANALYSIS: BY CLONE, 2024

-

EUROPE MARKET SHARE ANALYSIS: BY CLONE, 2024

-

GERMANY MARKET SHARE ANALYSIS: BY CLONE, 2024

-

UK MARKET SHARE ANALYSIS: BY CLONE, 2024

-

ASIA-PACIFIC MARKET SHARE ANALYSIS: BY CLONE, 2024

-

INDIA MARKET SHARE ANALYSIS: BY CLONE, 2024

-

JAPAN MARKET SHARE ANALYSIS: BY CLONE, 2024

-

GLOBAL COMPANION DIAGNOSTICS MARKET, TEST TYPE SEGMENT ATTRACTIVENESS, 2024 & 2035 (USD MILLION)

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY TEST TYPE, 2024 & 2035 (USD MILLION)

-

GLOBAL COMPANION DIAGNOSTICS MARKET SHARE (%), BY TEST TYPE, 2024

-

GLOBAL COMPANION DIAGNOSTICS MARKET, PRODUCT & SERVICES SEGMENT ATTRACTIVENESS, 2024 & 2035 (USD MILLION)

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY PRODUCT & SERVICES, 2024 & 2035 (USD MILLION)

-

GLOBAL COMPANION DIAGNOSTICS MARKET SHARE (%), BY PRODUCT & SERVICES, 2024

-

GLOBAL COMPANION DIAGNOSTICS MARKET, TECHNOLOGY SEGMENT ATTRACTIVENESS, 2024 & 2035 (USD MILLION)

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY TECHNOLOGY, 2024 & 2035 (USD MILLION)

-

GLOBAL COMPANION DIAGNOSTICS MARKET SHARE (%), BY TECHNOLOGY, 2024

-

GLOBAL COMPANION DIAGNOSTICS MARKET, INDICATION SEGMENT ATTRACTIVENESS, 2024 & 2035 (USD MILLION)

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY INDICATION 2024 & 2035 (USD MILLION)

-

GLOBAL COMPANION DIAGNOSTICS MARKET SHARE (%), BY INDICATION, 2024

-

GLOBAL COMPANION DIAGNOSTICS MARKET, END USER SEGMENT ATTRACTIVENESS, 2024 & 2035 (USD MILLION)

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY END USER 2024 & 2035 (USD MILLION)

-

GLOBAL COMPANION DIAGNOSTICS MARKET SHARE (%), BY END USER, 2024

-

GLOBAL COMPANION DIAGNOSTICS MARKET, BY REGION, 2024 & 2035 (USD MILLION)

-

GLOBAL COMPANION DIAGNOSTICS MARKET SHARE (%), BY REGION, 2024

-

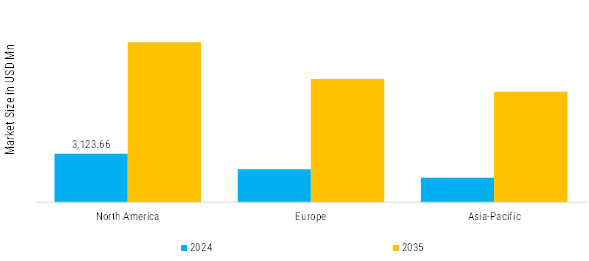

NORTH AMERICA MARKET ANALYSIS: COMPANION DIAGNOSTICS MARKET, 2019-2035 (USD MILLION)

-

NORTH AMERICA COMPANION DIAGNOSTICS MARKET, BY COUNTRY, 2024 & 2035 (USD MILLION)

-

NORTH AMERICA COMPANION DIAGNOSTICS MARKET SHARE (%), BY COUNTRY, 2024

-

EUROPE MARKET ANALYSIS: COMPANION DIAGNOSTICS MARKET, 2019-2035 (USD MILLION)

-

EUROPE: COMPANION DIAGNOSTICS MARKET, BY COUNTRY, 2024 & 2035 (USD MILLION)

-

EUROPE: COMPANION DIAGNOSTICS MARKET SHARE (%), BY COUNTRY, 2024

-

ASIA-PACIFIC MARKET ANALYSIS: COMPANION DIAGNOSTICS MARKET, 2019-2035 (USD MILLION)

-

ASIA-PACIFIC MARKET ANALYSIS: COMPANION DIAGNOSTICS MARKET, 2019-2035 (USD MILLION)

-

ASIA-PACIFIC COMPANION DIAGNOSTICS MARKET SHARE (%), BY COUNTRY, 2024

-

GLOBAL COMPANION DIAGNOSTICS MARKET PLAYERS: COMPETITIVE ANALYSIS, 2024

-

COMPETITOR DASHBOARD: GLOBAL COMPANION DIAGNOSTICS MARKET

-

QIAGEN: FINANCIAL OVERVIEW SNAPSHOT

-

QIAGEN: SWOT ANALYSIS

-

BIO-TECHNE: FINANCIAL OVERVIEW SNAPSHOT

-

BIO-TECHNE: SWOT ANALYSIS

-

BIOMÉRIEUX: FINANCIAL OVERVIEW SNAPSHOT

-

BIOMÉRIEUX: SWOT ANALYSIS

-

THERMO FISHER SCIENTIFIC INC.: FINANCIAL OVERVIEW SNAPSHOT

-

THERMO FISHER SCIENTIFIC INC.: SWOT ANALYSIS

-

ILLUMINA, INC.: FINANCIAL OVERVIEW SNAPSHOT

-

AGILENT TECHNOLOGIES, INC.: FINANCIAL OVERVIEW SNAPSHOT

-

Source: Annual Report, Press Releases, And MRFR Analysis

-

AGILENT TECHNOLOGIES, INC.: SWOT ANALYSIS

-

F. HOFFMANN-LA ROCHE LTD (FOUNDATION MEDICINE INC.): FINANCIAL OVERVIEW SNAPSHOT

-

MYRIAD GENETICS, INC.: FINANCIAL OVERVIEW SNAPSHOT

Leave a Comment