Neuroprosthetics Market Summary

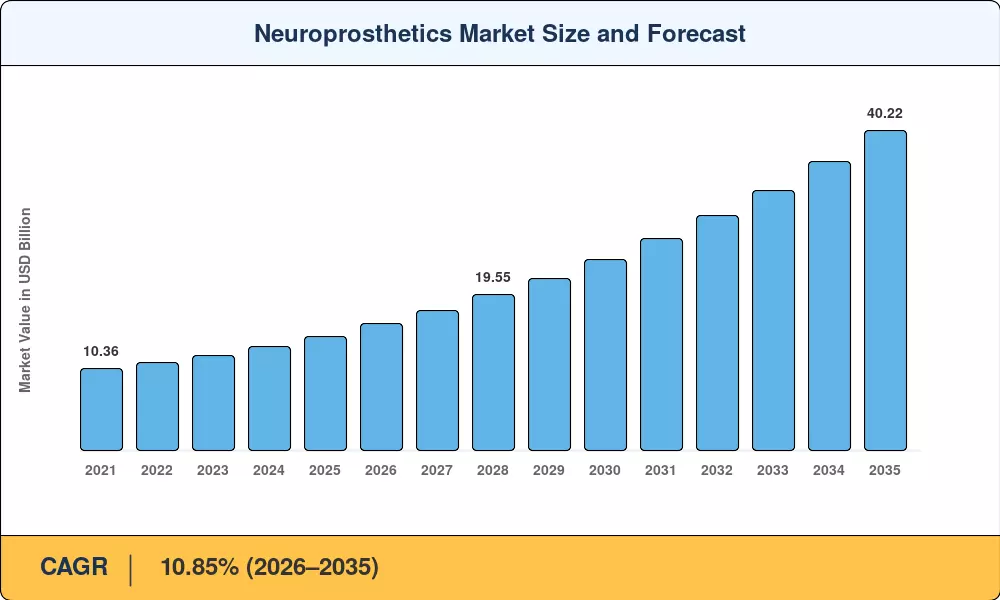

The Global Neuroprosthetics Market size was valued at USD 14.35 Billion in 2025, and the market is projected to grow from USD 15.91 Billion in 2026 to USD 40.22 Billion by 2035, registering a CAGR of 10.85% during the forecast period 2026–2035. Two forces are accelerating demand simultaneously: the FDA granted a record 23 Breakthrough Device designations to neuromodulation platforms between 2023 and 2025, while CMS expanded Medicare reimbursement codes for spinal-cord and deep-brain stimulation procedures, lowering the out-of-pocket barrier for patients over 65 [1][2].

The technological backbone of the Neuroprosthetics Market is shifting from open-loop stimulation hardware toward closed-loop adaptive platforms that adjust therapy parameters in real time using on-device machine-learning algorithms. Miniaturized system-on-chip designs, flexible polymer electrode arrays, and hermetic titanium micro-packaging now enable devices that last 12–15 years between surgical revisions — roughly double the lifespan of implants approved a decade ago. Venture capital directed at neurotechnology startups averaged USD 1.5 billion per year since 2023, signaling strong commercial conviction in paralysis-recovery and treatment-resistant depression applications [3][4].

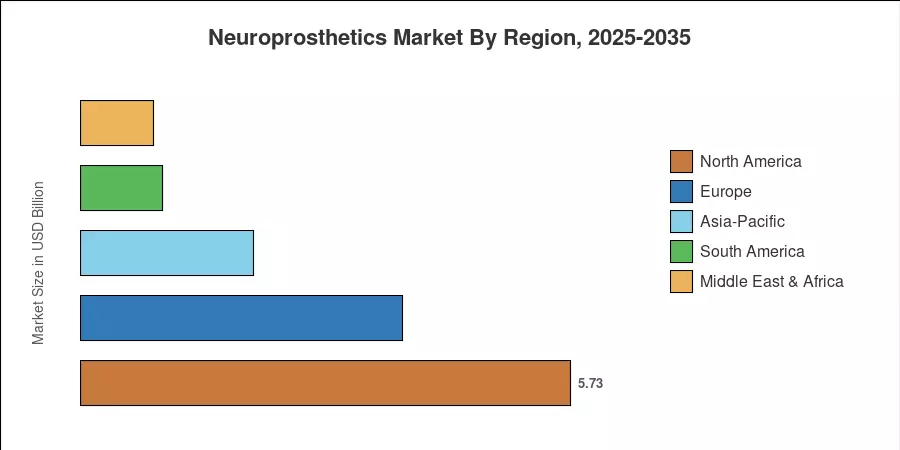

North America commanded roughly 39.9% of the Neuroprosthetics Market in 2025, anchored by the US reimbursement ecosystem and a dense clinical-trial infrastructure. Asia-Pacific represents the fastest-growing geography at a 14.09% CAGR through 2035, fueled by rising neurosurgery capacity in China, India, and South Korea. Europe holds the second-largest position with approximately 26.2% share, driven by CE-MDR regulatory harmonization and strong public-health funding across Germany, France, and the Nordics. The decade ahead will test whether supply chains for biocompatible materials can scale at the same pace as clinical demand.

Key Report Takeaways

• By Type

- Output neuroprosthetics accounted for approximately 51.5% of the Neuroprosthetics Market in 2025, reflecting dominant demand for motor and sensory restoration systems.

• By Component

- Implantable devices represented a 58.6% share of the Neuroprosthetics Market in 2025, underpinned by surgeon preference for fully internalized stimulation platforms.

- Software and algorithm platforms are forecast to expand at a 13.2% CAGR through 2035, the fastest-growing component category.

• By Technique

- Deep brain stimulation led all techniques with a 33.9% share of the Neuroprosthetics Market in 2025, supported by established Parkinson's disease protocols.

• By Application

- Motor-disorder treatments captured 46.1% of the Neuroprosthetics Market in 2025, the largest application segment.

- Cognitive and psychiatric applications are set to grow at an 11.88% CAGR to 2035, reflecting expanded indications for depression and OCD.

• By End User

- Hospitals managed 55.7% of the Neuroprosthetics Market in 2025, though ambulatory and home-care settings are growing fastest at a 13.74% CAGR.

• By Region

- Asia-Pacific is expanding at a 14.09% CAGR — the highest among all regions — driven by government neuroscience initiatives in China and India.

Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from company financials, regulatory filings, and procedural volume databases, then applies a triangulated bottom-up and top-down methodology calibrated against third-party benchmarks for the Neuroprosthetics Market. Forecast projections assume continuation of current reimbursement trends and a stable regulatory approval cadence.