Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

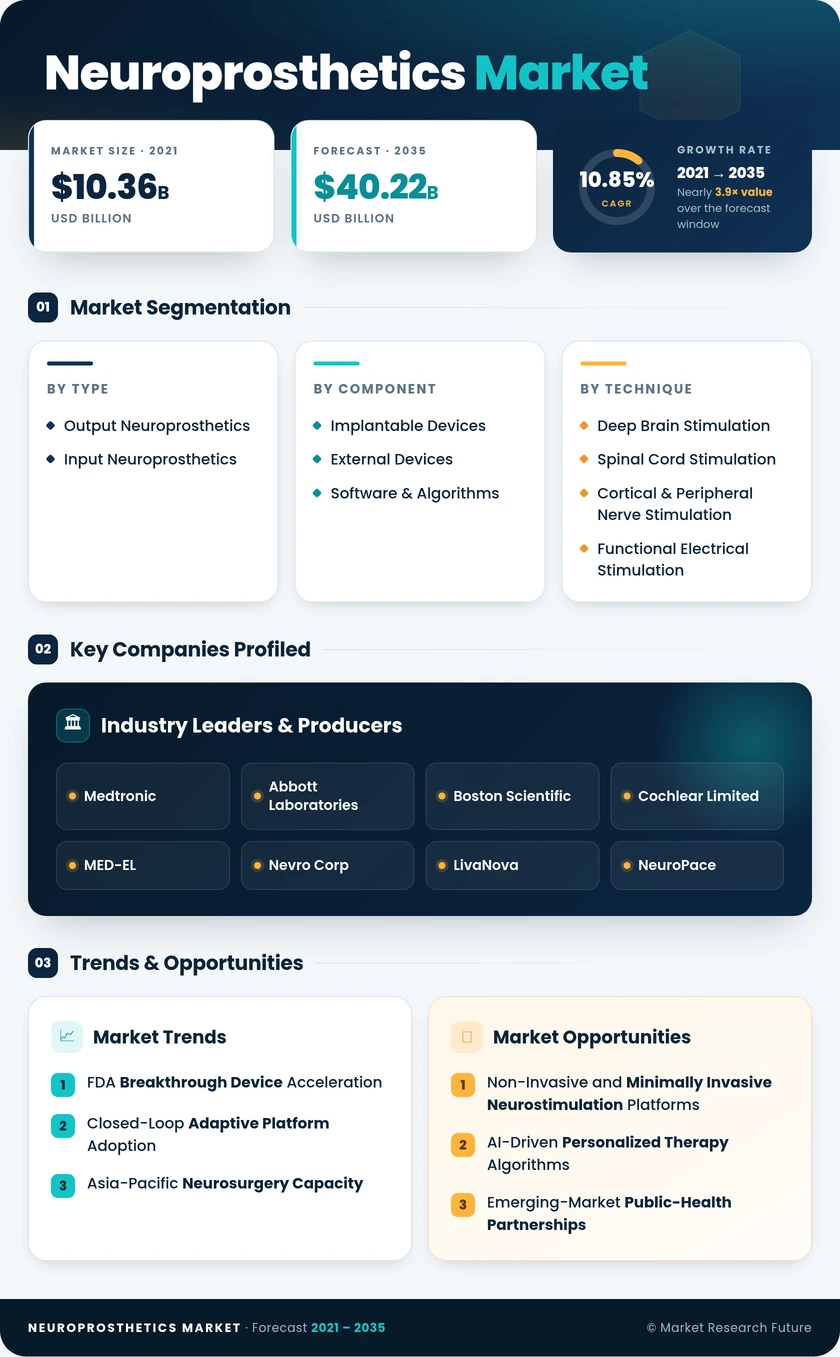

| By Type | Output Neuroprosthetics, Input Neuroprosthetics | Output Neuroprosthetics | Input Neuroprosthetics |

| By Component | Implantable Devices, External Devices, Neuroprosthetics Market & Algorithms | Implantable Devices | Neuroprosthetics Market & Algorithms |

| By Technique | Deep Brain Stimulation, Spinal Cord Stimulation, Cortical & Peripheral Nerve Stimulation, Functional Electrical Stimulation | Deep Brain Stimulation | Cortical & Peripheral Nerve Stimulation |

| By Application | Motor Disorders, Auditory Disorders, Visual Disorders, Cognitive & Psychiatric Disorders | Motor Disorders | Cognitive & Psychiatric Disorders |

| By End User | Hospitals, Ambulatory Surgical Centers, Home Care & Remote Monitoring | Hospitals | Home Care & Remote Monitoring |

Market Segmentation Overview

By Type

| Sub-Segment | Key Trend |

| Output Neuroprosthetics | Established dominance via DBS, cochlear, and SCS platforms; incremental innovation in electrode design |

| Input Neuroprosthetics | Rapid growth driven by brain-computer interface decoding advances and paralysis-recovery applications |

Output neuroprosthetics remain the revenue backbone due to decades of clinical validation in Parkinson's, hearing loss, and chronic pain. Input neuroprosthetics are emerging as the higher-growth frontier, fueled by academic-to-commercial translation of neural-recording technologies.

By Component

| Sub-Segment | Key Trend |

| Implantable Devices | Titanium micro-packaging and flexible electrode arrays extending device lifespans beyond 12 years |

| External Devices | Non-invasive transcranial stimulators and wearable neuromodulation units are expanding outpatient use |

| Neuroprosthetics Market & Algorithms | AI-based closed-loop therapy optimization creating recurring SaaS revenue streams |

Implantable devices continue to lead by revenue share, though software platforms are attracting disproportionate venture investment as OEMs pursue recurring-revenue business models.

By Technique

| Sub-Segment | Key Trend |

| Deep Brain Stimulation | Directional leads and sensing-enabled IPGs are improving targeting precision for Parkinson's and tremor |

| Spinal Cord Stimulation | High-frequency and burst waveforms replacing traditional tonic stimulation in pain management |

| Cortical & Peripheral Nerve Stimulation | FDA-cleared responsive cortical systems for epilepsy and emerging depression indications |

| Functional Electrical Stimulation | Rehabilitation-focused surface and implanted FES systems for stroke and spinal injury recovery |

Deep brain stimulation anchors the technique landscape with the largest installed patient base globally. Cortical and peripheral nerve stimulation represent the fastest-growing category as new psychiatric and neurological indications receive regulatory clearance.

By Application

| Sub-Segment | Key Trend |

| Motor Disorders | Parkinson's, essential tremor, and dystonia — the largest patient pool with established reimbursement |

| Auditory Disorders | Pediatric and adult cochlear implantation is expanding through emerging-market subsidy programs |

| Visual Disorders | Retinal and cortical visual prostheses advancing through clinical trials for retinitis pigmentosa |

| Cognitive & Psychiatric Disorders | Treatment-resistant depression and OCD entering pivotal-trial phase with closed-loop platforms |

Motor disorders command the largest share due to well-defined surgical protocols and broad payer coverage. Cognitive and psychiatric disorders represent the most significant growth opportunity as clinical evidence strengthens across depression and anxiety indications.

By End User

| Sub-Segment | Key Trend |

| Hospitals |