倉庫管理システム市場 概要

MRFRの分析によると、倉庫管理システム(WMS)市場規模は2024年に43.9億米ドルと推定されています。WMS業界は2025年に48.32億米ドルから2035年までに126.1億米ドルに成長すると予測されており、2025年から2035年の予測期間中に年平均成長率(CAGR)は10.07%となる見込みです。

主要な市場動向とハイライト

倉庫管理システム(WMS)市場は、技術の進歩と変化する消費者の需要により、 substantialな成長が見込まれています。

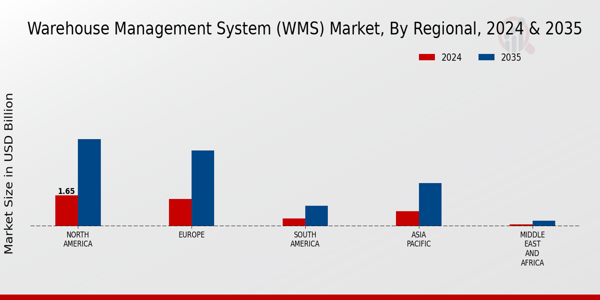

- 北米は倉庫管理システムの最大市場であり、高度な物流ソリューションに対する堅調な需要を反映しています。アジア太平洋地域は急速な工業化と増加する電子商取引活動に後押しされ、最も成長している市場として浮上しています。クラウドベースのソリューションが市場を支配しており、企業が柔軟な展開オプションを求める中でハイブリッドシステムが注目を集めています。電子商取引の需要の高まりとサプライチェーンの最適化への注力が、WMS市場の拡大を促進する主要な要因です。

市場規模と予測

| 2024 Market Size | 4.39億ドル |

| 2035 Market Size | 126.1億ドル |

| CAGR (2025 - 2035) | 10.07% |

主要なプレーヤー

SAP(ドイツ)、Oracle(アメリカ)、Manhattan Associates(アメリカ)、Blue Yonder(アメリカ)、Infor(アメリカ)、HighJump(アメリカ)、Softeon(アメリカ)、TECSYS(カナダ)、Epicor(アメリカ)