全球角膜塑形镜市场概览

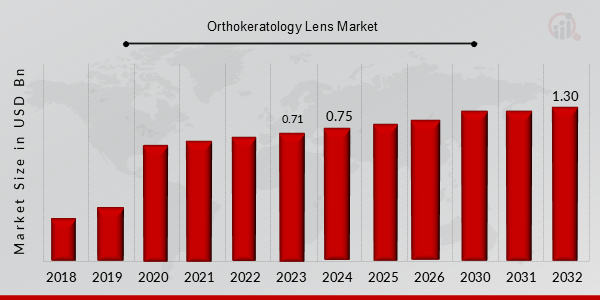

p角膜塑形镜市场在 2023 年的价值为 7.1 亿美元,预计将从 2024 年的 8 亿美元增长到 2032 年的 13 亿美元,预测期内(2024 - 2032 年)的复合年增长率为 6.60%。屈光不正患病率的不断上升,远视、近视、散光等疾病诊断率的不断上升,以及主要参与者研发活动的不断加强,是推动角膜塑形镜市场份额增长的关键市场驱动力。

角膜塑形镜市场趋势

ul

p角膜塑形镜是一种特殊的透气性镜片,适合所有年龄段,专为角膜重塑而设计。这些镜片可以在夜间佩戴,避免患者在白天佩戴眼镜或

隐形眼镜。最近的几项研究发现,角膜塑形治疗是减缓儿童近视发展的有效方法之一。一些国家的医疗保健专业人士也将这些镜片称为日间角膜塑形镜。目前有多种视力矫正手术可用于治疗近视和散光等屈光不正,例如屈光性晶状体置换术、LASIK 和准分子激光角膜切削术 (PRK)。然而,这些手术的一些副作用,例如干眼症、瘙痒、眩光模糊、视力下降以及夜间灯光周围的光晕,导致人们使用这些手术的比例下降。例如,2020 年的一篇文章指出,20% 至 40% 的 LASIK 患者在术后会出现干眼症和瘙痒症状,20% 的 LASIK 患者在夜间难以看清对比度、眩光和灯光周围的光晕。

影响儿童选择角膜塑形镜的一个重要因素是他们矫正屈光不正的选项有限。另一个导致儿童越来越多地使用这些镜片的因素是他们白天不再需要佩戴隐形眼镜和眼镜。此外,技术的进步使得镜片的配戴变得更加便捷,这有助于提高公众对镜片的认知度和接受度,从而推动角膜塑形镜市场的复合年增长率。例如,专业隐形眼镜制造商 Scotlens 于 2021 年 9 月与 Avizor 合作,推出了全新的角膜塑形镜开箱体验,以提高公众对该产品的认知度。因此,主要市场参与者批准的产品数量和产品发布数量不断增加,以及这些镜片的技术发展和优势不断增强,预计将推动角膜塑形镜市场在非手术屈光不正矫正手术中的收入增长机会。

来源:初步研究、二次研究、MRFR 数据库和分析师评论

角膜塑形镜市场细分洞察

h3

角膜塑形镜材料洞察 p根据材料,角膜塑形镜市场细分包括有机硅丙烯酸酯、氟硅丙烯酸酯和氟碳丙烯酸酯。 2022 年,硅丙烯酸酯细分市场占据了大部分份额,贡献了约 44-49% 的角膜塑形镜市场收入。硅树脂具有高度的柔韧性,使其成为一种流行的隐形眼镜材料。氟丙烯酸酯的高折射率和其他优势推动了硅丙烯酸酯镜片的生产。因此,预计硅丙烯酸酯角膜塑形镜的各种优势将促进该细分市场的增长。美国食品药品监督管理局 (FDA) 对用于治疗屈光不正的角膜塑形镜的批准增加,以及镜片设计和材料的技术进步,预计将推动全球市场的增长。

角膜塑形镜应用洞察

p应用将角膜塑形镜市场数据分为近视、远视和其他。近视细分市场在 2022 年占据了市场主导地位,并且很可能在 2022-2030 年预测期内成为增长最快的细分市场。近视在世界各地的儿童和老年人中越来越普遍,患者选择非侵入性技术而非屈光手术,这推动了近视市场的增长。根据《眼科与视觉科学研究》杂志的数据,全球约有19亿人患有近视,占全球人口的近27.08%。未来几年,近视将成为全球永久性失明的主要因素之一。由于儿童近视患病率较高,角膜塑形镜在儿童中很受欢迎。据世界卫生组织预测,到 2050 年,52.13% 的人将患有近视。角膜塑形镜有助于减缓近视的发展,尤其是对儿童而言,同时促进细分市场的增长。

2022 年 1 月:

角膜塑形镜最终用户洞察

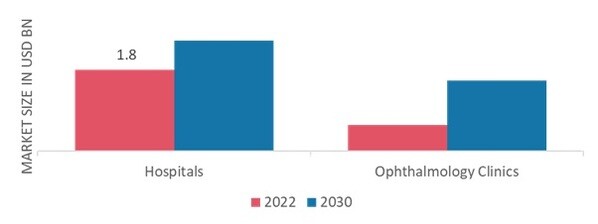

根据最终用户,全球角膜塑形镜行业已细分为医院和眼科诊所。医院在 2022 年占据了最突出的细分市场收入份额。由于青光眼和白内障等眼部疾病的发病率不断上升,医院对角膜塑形镜的投资机会不断增加,从而推动了市场的增长。由于先进的治疗设施,医院对角膜塑形镜的采用率不断提高,预计将进一步推动该细分市场的增长。然而,全球不同医院对角膜塑形镜的使用情况可能存在差异,这限制了市场的扩张。此外,一些医院正在开设针对多种屈光疾病的综合眼科中心,预计这将加速该细分市场的增长。

图 2:角膜塑形镜市场(按最终用户划分),2023 年及以后2032(十亿美元) strong来源:初步研究、二次研究、MRFR 数据库和分析师评论

strong来源:初步研究、二次研究、MRFR 数据库和分析师评论

预计在整个预测期内,角膜塑形镜行业在眼科诊所领域的复合年增长率将显著提高。人们更喜欢眼科诊所,因为患者费用低。视力丧失患者数量的增加预计将增加对眼科诊所的需求。新兴经济体中眼科医生数量的增加预计将增加对眼科诊所的需求,从而促进该领域的增长。此外,在一些服务欠缺经济体的眼科诊所中,越来越多地能够获得先进的眼科相关技术解决方案,预计将推动该领域的增长。全球眼科诊所日益激烈的竞争预计将在未来几年推动对角膜塑形镜的需求。

角膜塑形镜区域洞察

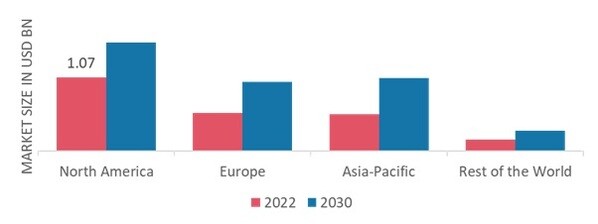

按地区划分,该研究提供了对北美、欧洲、亚太地区和世界其他地区的市场洞察。北美角膜塑形镜市场在 2022 年的规模为 10.7 亿美元,预计在研究期间将呈现显著的复合年增长率。角膜塑形镜的最新进展、夜间角膜塑形镜的推出以及灵活性和选择性是推动北美市场增长的一些因素。视力障碍病例的增加,加上加拿大和美国角膜塑形镜使用率的增加,预计将在整个地区创造大量增长机会。此外,强生视力、库博光学和博士伦等美国主要市场参与者预计将在未来几年提升其在该地区角膜塑形镜市场的份额。例如,2021 年 4 月,强生视力与 Menicon 达成合作,将后者的专业知识与强生视力的视野、科技和能力相结合,以应对儿童近视病例不断增加的问题。作为合作的一部分,Menicon 将开发治疗性隐形眼镜,而 JJ Vision 将专注于扩大新产品的范围。

此外,市场报告中研究的主要国家是美国、德国、加拿大、法国、英国、西班牙、意大利、日本、印度、澳大利亚、中国、韩国和巴西。

图 3:2023 年各地区角膜塑形镜市场份额 (%) strong来源:初步研究、二次研究、MRFR 数据库和分析师评论

strong来源:初步研究、二次研究、MRFR 数据库和分析师评论

欧洲角膜塑形镜市场占据第二大市场份额,这得益于该地区老年人口的增长以及人们倾向于不通过手术或传统眼镜矫正视力问题。此外,政府不断推出旨在提高高质量治疗可及性的举措,这也推动了该地区角膜塑形镜市场的需求。随着近视和老花眼等眼部疾病的流行,预计医务人员对角膜塑形镜的使用率将会增加。技术进步和获得 CE 认证的产品数量的增加预计将进一步促进该地区的增长。此外,德国角膜塑形镜市场占据最大市场份额,英国角膜塑形镜市场是欧洲地区增长最快的市场。

得益于 SEED 和 ProCornea 等先进产品的普及以及该地区老年人口的增长,预计亚太地区角膜塑形镜市场将在 2022 年至 2030 年间以最快的复合年增长率增长。此外,随着人们对眼部疾病认识的提高,以及该地区重要参与者的扩张和新业务的推出,预计将推动市场增长。例如,2020年12月,Menicon Alpha Corporation 的子公司成立了中国本土子公司阿尔法(无锡)有限公司,以扩大其在中国的角膜塑形镜销量和业务。此外,亚洲国家/地区眼科诊所和医院数量的不断增长,预计将在预测期内推动对角膜塑形镜的需求。此外,中国角膜塑形镜市场占有最大的市场份额,而印度角膜塑形镜市场是亚太地区增长最快的市场。

角膜塑形镜主要市场参与者及竞争洞察

由于全球范围内屈光不正的患病率不断上升,主要的市场参与者正致力于满足对这些角膜塑形镜治疗日益增长的需求。角膜塑形镜行业通过使用为每位患者特制的硬性镜片来改变角膜曲率,提供非手术性屈光不正矫正。行业参与者还在推行各种战略性市场发展计划,以扩大其全球影响力,包括推出新产品、签订合同、收购兼并、增加研发投入以及与其他组织的合作。

角膜塑形镜市场的主要参与者,包括 Menicon Co. Ltd、CooperVision Inc、Euclid Systems Corporation、Alcon Inc 等,正在大力投资研发,以生产高效且经济的角膜塑形镜。在当地生产这些镜片以降低运营成本是全球角膜塑形镜行业生产公司用来造福消费者并扩大市场领域的核心业务策略之一。

强生Johnson Vision (JJV) 是强生公司的子公司,由两个部门组成:强生视力保健(隐形眼镜)和强生手术视力。该公司提供的服务包括人工晶状体、超声乳化系统、激光视力矫正系统、粘弹剂、微型角膜刀以及用于白内障和屈光手术的相关产品。该公司在 24 个国家/地区开展业务,其产品销往约 60 个国家/地区。强生视力于 2021 年 5 月获得 FDA 批准,可用于生产用于近视管理的首款角膜塑形镜。

此外,CooperVision 是一家全球性隐形眼镜公司,为 130 多个国家的眼保健专业人士和镜片佩戴者提供服务。他们基于科学和技术进步创造了各种创新的软性隐形眼镜。它成立于 1980 年,总部位于美国加利福尼亚州。Cooper Companies Inc 收购了领先的角膜塑形镜制造商之一 CE GP Specialists Inc经销商,以拓展 CooperVision 的专业眼科护理业务,并解决近视日益严重和普遍的问题。

角膜塑形镜市场的主要公司包括

- Procornea Netherlands B.V.

- Euclid Systems Corporation

- Visioneering Technologies Inc

角膜塑形镜行业动态

2022 年 9 月:强生视力保健公司确认,美国 FDA 已批准 ACUVUE Abiliti 夜间治疗镜片(增强型,最高可达 6.00 屈光度)用于角膜塑形镜行业。

2022 年 6 月:

2022 年 4 月:

角膜塑形镜市场细分

角膜塑形镜材料展望

角膜塑形镜应用展望

角膜塑形镜终端用户展望

角膜塑形镜区域展望