全球燃料电池动力系统市场概览:

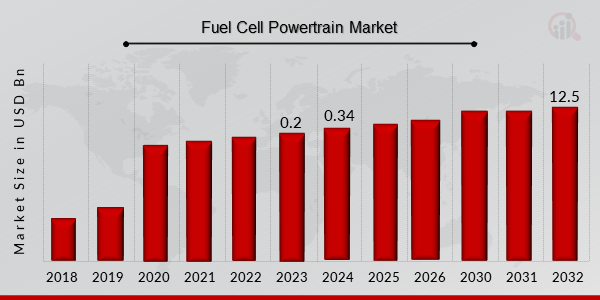

p2023 年燃料电池动力系统市场规模为 2 亿美元。预计燃料电池动力系统市场规模将从 2024 年的 3.4 亿美元增长到 2032 年的 125 亿美元,预测期内(2024 - 2032 年)的复合年增长率 (CAGR) 为 56.80%。对低排放汽车的需求不断增长和汽车续航里程不断扩大、技术进步导致燃料电池成本降低以及汽油和柴油成本上升是推动市场增长的主要市场驱动力。

重点介绍燃料电池动力系统市场的主要趋势

p全球推动脱碳和清洁能源移动的重大转变正在推动燃料电池动力系统市场的发展。随着主要经济体的政府和监管机构实施严格的排放标准和采用零排放汽车的激励措施,氢动力燃料电池汽车 (FCV) 的发展正在加速。

关键进展在提高燃料电池系统的效率、耐用性和成本效益方面也发挥着重要作用。膜电极组件、双极板和储氢系统的创新有助于降低每千瓦的总成本,使燃料电池更适合大众市场部署。此外,汽车制造商、燃料电池堆供应商和氢气生产商之间的合作正在简化价值链并鼓励标准化。

随着适用于不同车辆类别的模块化和可扩展动力总成架构的出现,初创企业和老牌企业正在进一步拓宽应用潜力。然而,生产成本高、加油基础设施不发达和氢气采购等挑战仍然存在。尽管存在这些障碍,燃料电池动力总成市场仍将稳步增长,预计未来十年市场将出现强劲增长,尤其是在亚太地区和欧洲。这一增长归功于全球利益相关者对绿色氢能生产和长期可持续发展目标的投资。

来源:二手资料研究、一手资料研究、MRFR 数据库和分析师评论

燃料电池动力系统市场趋势

ul

-

燃油经济性的提高和续航里程的增加正在推动市场增长。

p与 ICE 汽车相比,FCEV 具有更高的燃油效率。根据美国能源部的数据,FCEV 的燃油效率约为每加仑汽油当量 (MPGge) 63 英里,而 ICE 汽车的燃油效率在高速公路上为 29 MPGge。通过混合动力,FCEV 的燃油效率可提高 3.2%。FCEV 在城市道路上的燃油效率约为 55 MPGge,而 ICE 汽车的燃油效率为 20 MPGge。此外,柴油的能量密度 (45.5 MJ/kg) 低于汽油 (45.8 MJ/kg)。与汽油或柴油相比,氢的能量密度约为 120 MJ/kg,大约高出三倍。充满电后,FCEV 和 BEV 的行驶里程差异很大。虽然 BEV 在电池充满电的情况下通常可以行驶约 110 英里,但 FCEV 无需加油即可行驶约 300 英里。本田 Clarity 在美国环保署 (EPA) 的驾驶评分中位居美国零排放汽车之首。它每次充电可行驶 366 英里。燃料电池动力系统市场将受到燃料电池电动汽车 (FCEV) 需求增长以及燃油经济性和续航里程提升的推动,从而推动

空气动力汽车市场的收入增长。为了应对全球日益严重的污染水平,各国政府正在加大对燃料电池等替代能源的投入。根据美国环保署的数据,2015 年交通运输行业是美国温室气体排放的第二大来源,占美国排放量的 27%。各国政府正在投资、支持并推动燃料电池的应用。例如,印度石油天然气部 (MoPNG) 透露,计划于 2021 年 3 月在德里阿格拉、古吉拉特邦(团结雕像)等旅游景点的燃料电池汽车展览的两个地方建造太阳能加氢站。除了燃料电池技术的进步外,还必须建设能够支持氢动力交通要求的强大基础设施。

燃料电池动力总成市场细分洞察:

h3

燃料电池动力总成组件洞察 p基于组件,全球

汽车灵活燃料发动机市场细分包括燃料电池、电池、驱动和储氢系统。燃料电池部分在预测期内的复合年增长率最高,拥有最大的市场份额。燃料电池系统是 FCEV 最重要和最昂贵的部件之一。燃料电池构成了燃料电池系统,其成本约占 FCEV 总价的 60%。因此,FCEV 销量的增长正在推动对燃料电池系统的需求和市场的增长。燃料电池动力系统功率输出洞察

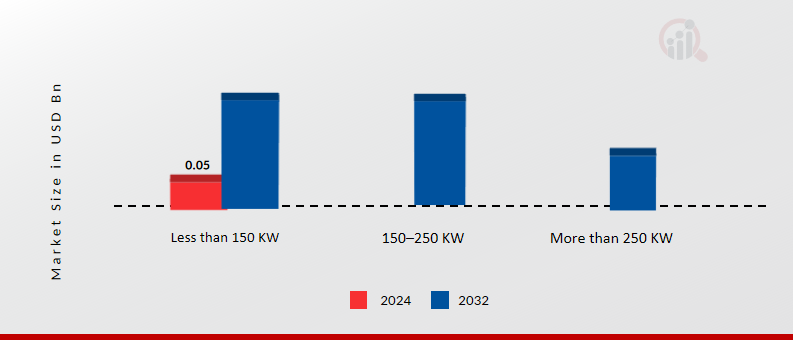

p根据功率输出,全球汽车灵活燃料发动机市场细分包括低于 150 千瓦、150-250 千瓦和高于 250 千瓦。2022 年,低于 150 千瓦的细分市场占据了市场主导地位,预计这种主导地位将持续整个预测期。大多数燃料电池电动汽车,尤其是作为乘用车销售的汽车,功率输出低于 150 千瓦。例如,最畅销的燃料电池汽车之一丰田 Mirai 就配备了一台可产生 128 千瓦电力的电机。因此,预计在不久的将来,对燃料电池乘用车的需求不断增长将推动类别的扩张。

图 1:按功率输出划分的燃料电池动力系统市场,2024 年和2032 年(十亿美元)

p

来源:二手资料研究、一手资料研究、MRFR 数据库和分析师评论

燃料电池动力系统车辆类型洞察

p根据车辆类型,全球汽车灵活燃料发动机市场细分包括乘用车、轻型商用车 (LCV)、公共汽车和卡车。乘用车类别在 2022 年占据市场主导地位,预计在整个预测期内将经历最快的复合年增长率。燃料电池动力系统市场的很大一部分来自乘用车。除了汽车制造商努力推出新款燃料电池乘用车以满足全球日益增长的绿色出行需求外,丰田 Mirai、现代 NEXO 等燃料电池乘用车的日益普及预计将在预测期内刺激该细分市场的增长。

燃料电池动力系统区域洞察

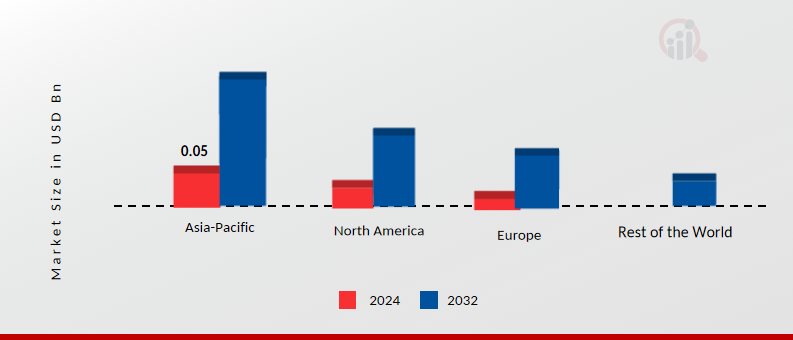

p按地区划分,本研究提供了北美、欧洲、亚太地区和世界其他地区的市场洞察。由于亚太地区对乘用车和节能汽车的需求不断增长,预计该地区将成为最大的市场。燃料电池动力系统市场的一些主要参与者都位于该地区,包括电装株式会社、上海燃料电池汽车动力系统有限公司和斗山株式会社。尽管该地区的市场相关企业数量少于北美和欧洲,但大多数燃料电池汽车的销量都来自该地区。现代 NEXO 和丰田 Mirai 是最受欢迎的两款车型,2021 年的销量分别为 8,900 辆和 17,940 辆。 2021 年,韩国占据了现代 NEXO 销量的近 92%,而日本则销售了大部分丰田 Mirai。

此外,市场报告中研究的主要国家包括美国、加拿大、德国、法国、英国、意大利、西班牙、中国、日本、印度、澳大利亚、韩国和巴西。

图 2:2024 年燃料电池动力系统市场份额(按地区划分)(单位:十亿美元)

p

来源:二手资料研究、一手资料研究、MRFR 数据库和分析师评论

2022 年,北美拥有占比第二大。由于加州对燃料电池电动汽车(FCEV)的需求不断增长,市场正在不断扩大。雪佛龙美国公司和岩谷美国公司(ICA)同意于2022年2月在加州建造30座加氢站。据加州空气资源委员会(CARB)称,该州将拥有超过176座加氢站,可容纳约25万辆燃料电池汽车。因此,目标地区的市场扩张受到氢能基础设施建设和零排放汽车需求增长的推动。

欧洲的燃料电池动力总成市场占据第三大市场份额。主要的原始设备制造商(OEM)投入了大量资金来改进这项技术,包括丰田、福特、本田、通用、现代、大众、戴姆勒和宝马。为了满足日益增长的客户期望,燃料电池已广泛应用于乘用车。目前,一些大型企业正在积极投资并在道路上测试这些技术。例如,宝马集团于2021年6月宣布,已开始测试搭载氢燃料电池动力系统的车辆;宝马I Hydrogen Next的原型车将接受一系列参数的评估,包括可靠性、安全性和效率。此外,德国燃料电池动力系统市场占有最大市场份额,而英国燃料电池动力系统市场是欧洲地区增长最快的市场。

燃料电池动力系统主要市场参与者及竞争洞察

p行业领先企业正在投入大量资金进行研发,以丰富其产品组合,这将刺激燃料电池动力系统市场的进一步增长。市场参与者也在采取各种战略行动,以扩大其全球影响力。重要的市场发展包括推出新产品、签订合同、并购、增加投资以及与其他组织的合作。空气动力汽车行业必须提供价格合理的产品,才能在更加残酷的市场环境中蓬勃发展。

全球燃料电池动力系统行业制造商为客户谋福利并扩大市场规模而采用的主要商业策略之一是本地制造,以降低运营成本。近年来,燃料电池动力系统行业取得了一些最大的增长。燃料电池动力系统市场的主要参与者包括 AVID Technology Ltd(英国)、Brown Machine Group(美国)、Ballard Power Systems(加拿大)、Ceres Power(英国)、Delphi Technologies(英国)、Cummins(美国)、ITM Power Manufacturings(英国)、Denso Corporation(日本)、Bloom Energy(美国)、Robert Bosch(德国)和 SFC Energy(德国)。质子交换膜 (PEM) 燃料电池产品由巴拉德电力系统公司 (Ballard Electricity Systems Inc.) 开发和生产,面向便携式电力、物料搬运、重型动力(包括公交车和有轨电车应用)以及工程服务等多个市场。迄今为止,巴拉德已设计并交付了超过 400 兆瓦的燃料电池设备。杰弗里·巴拉德 (Geoffrey Ballard)、基思·普拉特 (Keith Prater) 和保罗·霍华德 (Paul Howard) 于 1979 年在巴拉德研究公司 (Ballard Research Inc.) 旗下创立了巴拉德公司,致力于高能锂电池的研发。巴拉德于 1989 年开始投资 PEM 燃料电池技术开发,并已为全球众多顶级产品制造商提供 PEM 燃料电池产品。巴拉德与潍柴动力于 2018 年达成战略合作协议。潍柴动力以 1.63 亿美元收购了巴拉德 19.9% 的股份。巴拉德和潍柴计划为中国市场提供卡车、客车和叉车的燃料电池系统。

2017年至2020年,德尔福科技一直作为一家独立汽车制造商运营,直至被博格华纳公司收购。德尔福汽车(原通用汽车的一个部门)更名为安波福(Aptiv),并将其动力总成和售后市场相关业务剥离给一家独立公司——德尔福科技股份有限公司(Delphi Technologies PLC),德尔福科技公司由此诞生。这家市值45亿美元的公司开始在纽约证券交易所交易,股票代码为之前的德尔福汽车(DLPH)。2017年12月6日,德尔福科技被纳入标准普尔中型股400指数。该公司业务涵盖乘用车和商用车领域,提供燃烧系统、电气化产品、软件和控制系统,并通过全球售后市场网络参与车辆维护。

燃料电池动力总成市场的主要公司包括

ul

- ITM Power Manufacturings(英国)

h2

燃料电池动力总成行业发展 p2024年,巴拉德公司获得加拿大太平洋堪萨斯城铁路公司(CPKC)的12台燃料电池发动机的后续订单,以增强其现有的氢动力机车车队,用于定期调车和本地货运服务。

Hydroplane Ltd于2022年6月宣布,将采取一项计划通过可改装现有通用航空飞机的氢燃料电池技术实现飞行脱碳。此外,该公司还公布了其最近完成的一轮融资,该轮融资来自不愿透露姓名的天使投资者,金额未披露为 200 万美元。

Scots 正在与大型电池制造厂 Battery Cell Specialist 合作,计划于 2022 年 6 月开发更先进的氢动力超级跑车和重型货车。

Bloom Energy 与法拉利合作,在 75 年内引领全球豪华汽车行业走向 2030 年碳中和,时间是 2022 年 6 月。该公司还在法拉利位于意大利马拉内罗不断扩建的制造工厂安装了 1 兆瓦 (MW) 的 Bloom 固体氧化物燃料电池。

2022 年 5 月,Ballard Power Systems 与 Wisdom Motor Company Limited、Temple Water Group 和 Bravo Transport Services Limited 建立战略合作伙伴关系,以加速在香港采用商用燃料电池电动汽车 (FCEV)。

燃料电池动力总成市场细分:

h3

燃料电池动力总成部件展望 ul

h3

燃料电池动力总成驱动类型展望 ul

h3

燃料电池动力总成功率输出展望 ul

h3

燃料电池动力系统车型展望 ul

h3

燃料电池动力系统区域展望 ul