strong来源:二手资料研究、一手资料研究、MRFR 数据库和分析师评论

strong来源:二手资料研究、一手资料研究、MRFR 数据库和分析师评论  strong来源:二手资料研究、一手资料研究、MRFR 数据库和分析师评论

strong来源:二手资料研究、一手资料研究、MRFR 数据库和分析师评论 What is the current valuation of the Freight Trucking Market as of 2024?

The Freight Trucking Market was valued at approximately 3232.28 USD Billion in 2024.

What is the projected market size for the Freight Trucking Market by 2035?

The market is projected to reach around 5164.38 USD Billion by 2035.

What is the expected CAGR for the Freight Trucking Market during the forecast period 2025 - 2035?

The expected CAGR for the Freight Trucking Market during 2025 - 2035 is 4.35%.

Which companies are considered key players in the Freight Trucking Market?

Key players in the market include J.B. Hunt Transport Services, Schneider National, Knight-Swift Transportation Holdings, and others.

What are the main segments of the Freight Trucking Market by application?

The main segments by application include Freight Transportation, Logistics Services, Supply Chain Management, and E-commerce Delivery.

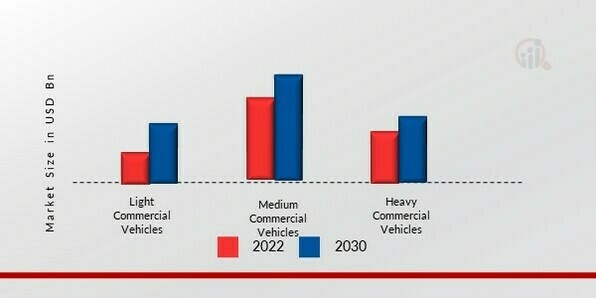

How does the Freight Trucking Market perform in terms of vehicle type segmentation?

The market segments by vehicle type include Heavy Duty Trucks, Medium Duty Trucks, Light Duty Trucks, and Refrigerated Trucks.

What fuel types are utilized in the Freight Trucking Market?

The market utilizes various fuel types, including Diesel, Natural Gas, Electric, and Hybrid.

What are the primary end-use segments in the Freight Trucking Market?

Primary end-use segments include Retail, Manufacturing, Construction, and Food and Beverage.

What service types are prevalent in the Freight Trucking Market?

Service types in the market include Dedicated Contract Carriage, Private Fleet, For-Hire Carrier, and Intermodal Transportation.

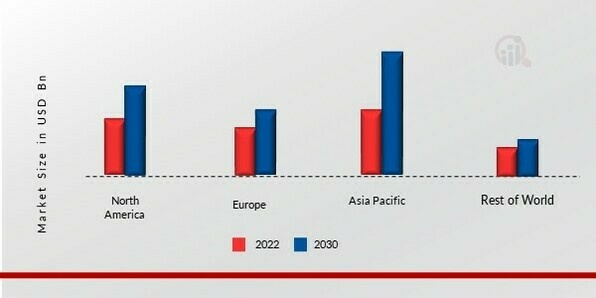

How does the Freight Trucking Market's growth compare across different segments?

The Freight Transportation segment is projected to grow from 1200.0 to 1900.0 USD Billion, indicating robust growth potential.