What is the projected market valuation of the Automotive Digital Cockpit Market by 2035?

The Automotive Digital Cockpit Market is projected to reach a valuation of 460.7 USD Billion by 2035.

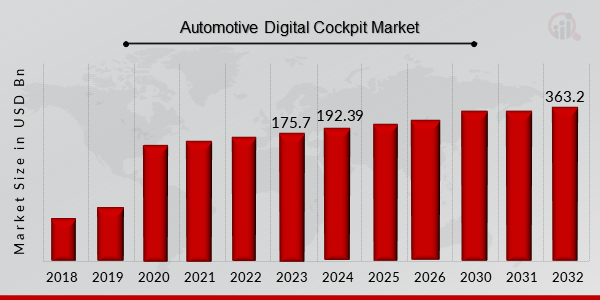

What was the market valuation of the Automotive Digital Cockpit Market in 2024?

In 2024, the Automotive Digital Cockpit Market was valued at 192.39 USD Billion.

What is the expected CAGR for the Automotive Digital Cockpit Market during the forecast period 2025 - 2035?

The expected CAGR for the Automotive Digital Cockpit Market during the forecast period 2025 - 2035 is 8.26%.

Which vehicle type segment is projected to have the highest valuation by 2035?

The Passenger Car segment is projected to reach a valuation of 230.0 USD Billion by 2035.

What are the projected valuations for the Digital Instrument Cluster Display Type segment by 2035?

The Digital Instrument Cluster Display Type segment is expected to reach a valuation of 100.0 USD Billion by 2035.

Which key players are leading the Automotive Digital Cockpit Market?

Key players in the Automotive Digital Cockpit Market include Continental AG, Denso Corporation, Harman International, and NVIDIA Corporation.

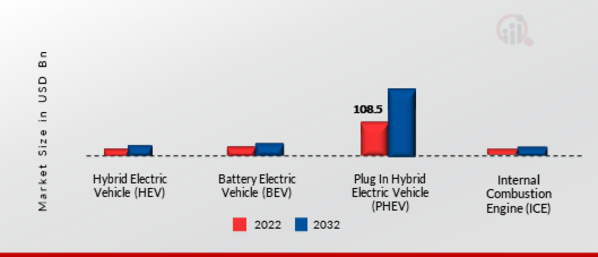

What is the projected valuation for the Battery Electric Vehicle (BEV) segment by 2035?

The Battery Electric Vehicle (BEV) segment is projected to reach a valuation of 150.0 USD Billion by 2035.

What is the expected valuation for the Camera-Based Driver Monitoring System segment by 2035?

The Camera-Based Driver Monitoring System segment is expected to reach a valuation of 160.7 USD Billion by 2035.

How does the Heavy Commercial Vehicle segment's valuation compare to the Light Commercial Vehicle segment by 2035?

By 2035, the Heavy Commercial Vehicle segment is projected to reach 160.7 USD Billion, while the Light Commercial Vehicle segment is expected to reach 70.0 USD Billion.

What is the projected valuation for the Internal Combustion Engine (ICE) segment by 2035?

The Internal Combustion Engine (ICE) segment is projected to reach a valuation of 180.7 USD Billion by 2035.