全球空气处理机组市场概览

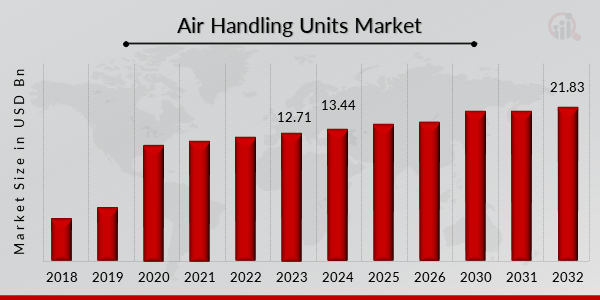

p2023 年,空气处理机组市场规模为 127.1 亿美元。预计到 2032 年,空气处理机组市场规模将从 2024 年的 134.4 亿美元增长到 218.3 亿美元,预测期内(2024 - 2032 年)的复合年增长率 (CAGR) 为 5.50%。

空气处理机组 (AHU),有时也称为空气处理器,是建筑物和工业设施中使用的供暖、通风和空调 (HVAC) 系统的重要组成部分。其主要功能是循环和调节空气,以保持舒适的室内环境。空气处理机组 (AHU) 通常用于商业建筑、医院、工厂、数据中心和其他设施。

来源:二手资料研究、一手资料研究、MRFR 数据库和分析师评论

空气处理机组市场趋势

ul

-

人口增长和城市化推动空调需求,从而推动空气处理机组市场的发展。

p人口激增是零售、商业和住宅建筑需求增长的主要因素。城市市场正在建造混合用途建筑,包括商业或零售建筑以及住宅公寓和共管公寓。空置的仓库和空置建筑正在被翻新,并改建成新的商业和住宅空间供租户使用。这进一步强调了开发商试图从建筑设计和设施的角度了解租户的需求,以确保高入住率。

这些因素直接推动了对高效空调系统(包括空气处理机组)的需求。根据世界银行的数据,2015 年城市人口为 39.6 亿,到 2020 年将增加到 43.6 亿。城市人口的急剧增长导致暖通空调系统需求在一年内增长。预计在预测期内,这种情况将持续下去,从而导致空气处理机组需求增加。

对清洁安全的工作环境的需求推动了空气处理机组市场的发展。

p消费者对保持良好室内空气质量益处的认识不断提高,也推动了市场的发展。空气处理机组 (AHU) 可以筛选出可能导致不同临床疾病和呼吸问题(包括慢性阻塞性肺病 (COPD)、缺血性心脏病、哮喘和肺癌)的有害空气毒素。消费者对技术的健康益处和认识正在不断提高,这刺激了对暖通空调 (HVAC) 系统的需求。这反过来又导致预测期内空气处理机组市场高速增长。

大多数消费者都很清楚建筑物和房屋对优质空气的需求。因此,提高空气质量意识正在推动空气处理机组市场的增长机会。工业化的兴起是空气处理机组市场的关键驱动力。工业领域对现代技术的需求不断增长,导致人们采用节能的暖通空调系统。工业部门主要在亚太地区持续增长,预计这将刺激对空气处理机组的需求。政府在风险投资方面的举措预计将进一步发展全球工业部门。中国、美国和印度等多个国家正积极推动政府援助,以发展本国的工业部门。

物联网在空气处理机组中的快速转型正推动空气处理机组市场蓬勃发展。

p物联网 (IoT) 解决了将空气处理机组 (AHU)/暖通空调 (HVAC) 系统连接到互联网以实现信息共享的问题。它收集信息,将其存储在云端,进一步开发活动以提高生产力,并运行有预见性的支持计划。它还能以经济高效的方式通过互联网监控、控制和诊断 AHU 和 HVAC 系统。此外,物联网还能降低

暖通空调系统的持续维护和维修成本。物联网允许访问 AHU 和 HVAC 系统的实时性能数据并进行准确解读。例如,支持物联网的建筑可以提前向设施管理人员发出任何运行异常的预警,并进行远程诊断和调整,从而通过最大限度地减少系统故障来节省成本。此外,商业或住宅建筑中的空气处理机组 (AHU) 和暖通空调 (HVAC) 系统消耗的能源最多。在这些应用中实施物联网将有助于节省成本、进行预测性维护、控制舒适度并提升建筑性能。物联网与 AHU 和暖通空调系统的融合为该行业的发展提供了机遇。

空气处理机组市场细分洞察

h3

空气处理机组类型洞察 p空气处理机组市场根据类型细分为组合式屋顶机组、模块化机组和定制机组。其中,组合式屋顶机组预计将在预测期内占据空气处理机组市场收入的主导地位。组合式屋顶机组在一个紧凑的单元中包含提供调节空气所需的所有组件。一体式屋顶空气处理机组 (AHU) 在零售和工业物业中非常受欢迎。由于这些机组安装在屋顶,因此无需像其他类型的 AHU 那样担心需要额外空间来安装。

Effect Insights 的空气处理机组

p空气处理机组市场细分,根据效果,可分为单效和双效。其中,双效机组在基准年市场中占据主导地位,预计在预测期内也将占据主导地位。双效空气处理机组是一个完整的模块化冷却解决方案。它为任何环境提供高性能、节能的解决方案,并且用户可以完全控制其场所内外的气流。

按容量洞察划分的空气处理机组

p空气处理机组市场细分,基于效果,市场细分为高达 5000 立方米/小时、5000 立方米/小时 - 15000 立方米/小时和高于 15000 立方米/小时。其中,高达 5000 立方米/小时的细分市场在基准年市场中占据主导地位,并且预计在预测期内也将占据主导地位。

按应用洞察划分的空气处理机组

p空气处理机组市场细分,基于应用,市场细分为工业、住宅和商业。其中,商业部门在基准年市场中占据主导地位,预计在预测期内也将占据主导地位。

空气处理机组区域洞察

p按地区,该研究将空气处理机组市场细分为北美、欧洲、亚太地区、中东和非洲以及拉丁美洲。亚太地区规模庞大的空气处理机组行业很可能使该地区成为全球最大的空气处理机组扩张市场。亚太地区正经历快速的城市化和人口增长,导致建筑活动增加。商业和住宅建筑以及基础设施项目的建设推动了对暖通空调 (HVAC) 系统的需求,从而推动了空气处理机组 (AHU) 的需求。这些设备对于维持新建建筑的室内空气质量和温度控制至关重要。

不断扩张的商业部门,包括办公楼、购物中心、酒店和数据中心,需要高效的暖通空调系统来提供舒适且可控的室内环境。空气处理机组是这些系统不可或缺的组成部分,可确保适当的空气循环、过滤和温度调节。亚太地区是工业增长的中心,制造设施、工厂和生产车间在该地区迅速扩张。这些工业设施需要空气处理机组 (AHU) 来控制空气质量、湿度和温度,以保障生产流程、员工舒适度和产品质量。

空气处理机组主要市场参与者及竞争洞察

p主要市场参与者正在投入大量资金进行研发,以扩大其产品线,这将有助于空气处理机组市场进一步增长。市场参与者还采取了一系列战略举措来扩大其全球影响力,包括推出新产品、签订合同、并购、增加投资以及与其他组织的合作。空气处理机组市场行业的竞争对手必须提供具有成本效益的产品,才能在竞争日益激烈、市场不断增长的环境中扩张和生存。

全球空气处理机组行业制造商为使客户受益并扩大空气处理机组市场而采用的主要业务策略之一是合作和收购。空气处理机组市场竞争激烈且高度分散,为国内及非正规企业提供了巨大的潜在机遇。一些主要参与者包括:Systemair(瑞典)、大金工业(日本)、特灵(爱尔兰)、开利公司(美国)、江森自控(爱尔兰)、基伊埃集团(德国)、Flakt集团(德国)、伦诺克斯国际(美国)、Sabiana(意大利)和VTS集团(卢森堡)。为了扩大全球影响力和客户群,主要公司正专注于收购和产品创新。

VTS集团:VTS集团是暖通空调(HVAC)行业先进设备的制造商之一。该公司提供通风、空调和供暖设备。该公司提供高质量的保修和保修后服务。该公司提供的产品包括空气处理机组、空调机组、供暖机组和风幕机。该公司还提供用于选择经欧洲认证的空气处理机组的软件。空气处理机组包括紧凑型吊顶式空调机组、紧凑型落地式空调机组、模块化空调机组、管道式空调设备、供暖机组、风幕机以及泵组等配件。公司业务遍及俄罗斯、欧洲、美国、中东和非洲以及亚太地区,员工人数超过 500 人。

Sabiana:Sabiana 是一家生产和设计用于空间空调设备的意大利公司。该公司为酒店、工厂、办公室、购物中心、医院和住宅建造系统和设备。该公司提供的产品包括单元加热器、辐射板、风机盘管、空气处理机组、回收装置、电子过滤器、不锈钢烟道、蒸发冷却器、辐射系统和其他产品。该公司的其他产品包括 Atlas STP 门帘、Energy Genius、Meltemi 门帘、Electra-Electromatic 电热单元加热器等。该公司开发了一种带有模块化单元的有源静电过滤器。

空气处理机组市场的主要公司包括

ul

h3

空气处理机组行业发展 p市场上最新的卫生型空气处理机组 HygenAir A+H,由 Colmac Coil Manufacturing, Inc. 于 2023 年 5 月推出。该公司声称,这款配件旨在提高加工室内环境的卫生水平,因为在这些环境中,消毒至关重要。该型号专为食品加工商设计,从而在满足美国农业部 (USDA) 的严格要求并确保质量的同时,提高了他们的安全性。

Edgetech Air Systems Pvt.先进的中央空调制造商开利公司(纽约证券交易所代码:CARR)于2023年5月在印度Central Vista项目中安装了智能空气处理机组。这些机组配备传感器、监视器、探测器等,能够及时收集性能数据,从而提高能源效率。

开利公司(纽约证券交易所代码:CARR)是开利全球公司旗下领先的智能气候控制系统和可再生能源解决方案提供商,于2023年9月推出了一系列适用于高温和超高温环境的热泵,适用于工业厂房、商业建筑以及区域供热。

特灵公司于2023年8月携其高科技垂直团队参加了在旧金山举办的SEMICON West展会,与其他行业领导者共同探讨全球微电子行业面临的重大挑战。

今年7月,Lennox公司公布了其在2023年经销商设计奖评选中取得的成就,其中包括创新产品、前沿设计和卓越的客户体验等,再次强调了其对行业的承诺。达到出色的输出。

2022 年 1 月:江森自控宣布推出适用于建筑物的 OpenBlue 室内空气质量即服务,通过创新的融资模式提供节能、交钥匙的清洁空气成果。

2022 年 1 月, 开利公司的 CIAT 部门正在推出其自动室内空气质量 (IAQ) 系统 Epure Dynamics,用于提供酒店、餐厅和酒吧等服务场所。

2021 年 12 月:特灵宣布推出新的数字室内环境质量 (IEQ) 管理解决方案。这些报告为建筑业主和设施管理人员提供了切实可行的见解,帮助他们打造更健康、更高效的室内空间,让居住者安心无忧。

空气处理机组市场细分

h3

空气处理机组类型展望 ul

h3

空气处理机组的影响展望 ul

h3

空气处理机组产能展望 ul

- 5000 立方米/小时 – 15000 立方米/小时

h3

空气处理机组应用展望 ul

h2

空气处理机组区域展望 ul