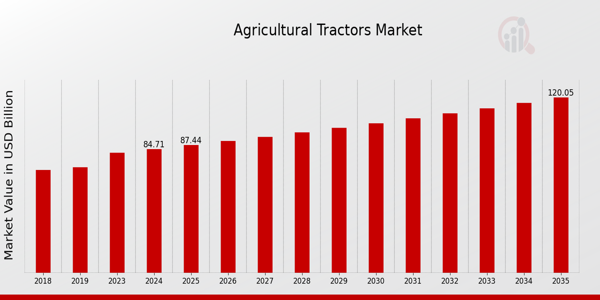

What is the current valuation of the Agricultural Tractors Market as of 2024?

The Agricultural Tractors Market was valued at 84.71 USD Billion in 2024.

What is the projected market valuation for the Agricultural Tractors Market in 2035?

The market is projected to reach a valuation of 120.04 USD Billion by 2035.

What is the expected CAGR for the Agricultural Tractors Market during the forecast period 2025 - 2035?

The expected CAGR for the Agricultural Tractors Market during the forecast period 2025 - 2035 is 3.22%.

Which companies are considered key players in the Agricultural Tractors Market?

Key players in the market include John Deere, CNH Industrial, AGCO Corporation, Kubota Corporation, Mahindra & Mahindra, Yanmar Co Ltd, SDF Group, Deutz-Fahr, and Tafe.

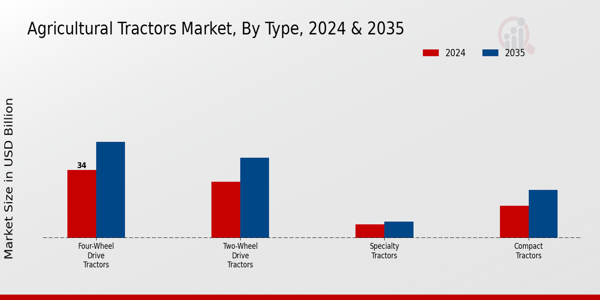

What are the market segments based on tractor type and their valuations?

The market segments include Two-Wheel Drive Tractors valued at 25.0 to 35.0 USD Billion, Four-Wheel Drive Tractors at 30.0 to 45.0 USD Billion, Compact Tractors at 15.0 to 20.0 USD Billion, and Specialty Tractors at 14.71 to 20.04 USD Billion.

How does the Agricultural Tractors Market perform in terms of application segments?

In terms of application, the market segments include Harvesting valued at 25.0 to 35.0 USD Billion, Tilling at 15.0 to 20.0 USD Billion, and Row Crop at 22.71 to 33.04 USD Billion.

What are the engine types used in agricultural tractors and their market valuations?

The engine types include Internal Combustion Engines valued at 60.0 to 85.0 USD Billion, Electric Engines at 15.0 to 25.0 USD Billion, and Hybrid Engines at 9.71 to 10.04 USD Billion.

What horsepower categories are present in the Agricultural Tractors Market?

Horsepower categories include Less than 40 HP valued at 15.0 to 20.0 USD Billion, 40-100 HP at 40.0 to 60.0 USD Billion, and Above 100 HP at 29.71 to 40.04 USD Billion.

What trends are influencing the growth of the Agricultural Tractors Market?

Trends influencing growth include advancements in engine technology, increasing demand for efficient farming practices, and the rising adoption of electric and hybrid engines.

How does the Agricultural Tractors Market compare to previous years?

The market shows a positive trajectory, with a valuation increase from 84.71 USD Billion in 2024 to a projected 120.04 USD Billion by 2035.