Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

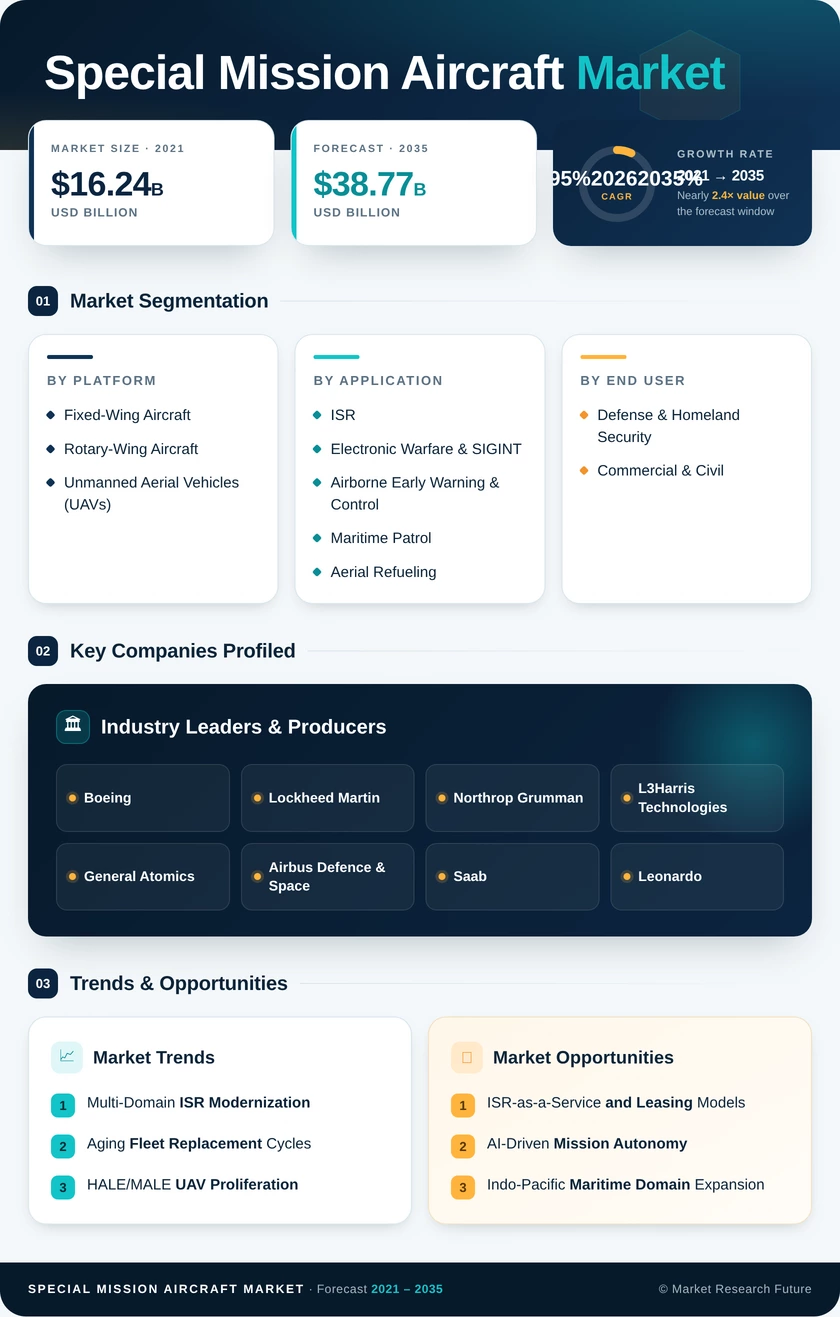

| By Platform | Fixed-Wing Aircraft; Rotary-Wing Aircraft; Unmanned Aerial Vehicles (UAVs) | Fixed-Wing Aircraft (42.5% share, 2025) | UAVs (13.15% CAGR) |

| By Application | ISR; Electronic Warfare & SIGINT; Airborne Early Warning & Control; Maritime Patrol; Aerial Refueling | ISR (59.2% share, 2025) | Electronic Warfare & SIGINT (9.55% CAGR) |

| By End User | Defense & Homeland Security; Commercial & Civil | Defense & Homeland Security (56.1% share, 2025) | Commercial & Civil (8.35% CAGR) |

| By Geography | North America; Europe; Asia-Pacific; South America; Middle East & Africa | North America (44.5% share, 2025) | Asia-Pacific (9.15% CAGR) |

Market Segmentation Overview

By Platform

| Sub-Segment | Key Trend |

| Fixed-Wing Aircraft | Multi-role MPA and AEW&C platforms dominate fleet procurement, driven by range and endurance advantages for maritime and overland ISR missions |

| Rotary-Wing Aircraft | Anti-submarine warfare and search-and-rescue missions sustain demand; naval helicopter upgrades in Europe and Asia-Pacific accelerate through 2030 |

| Unmanned Aerial Vehicles (UAVs) | HALE and MALE UAVs rapidly replace manned ISR sorties; export orders from allied nations fuel double-digit CAGR growth through 2035 |

Fixed-wing platforms remain the backbone of the special mission aircraft market, but unmanned systems are closing the gap as operating economics and mission endurance increasingly favor autonomous and remotely piloted alternatives across all geographic theaters.

By Application

| Sub-Segment | Key Trend |

| Intelligence, Surveillance & Reconnaissance (ISR) | Multi-sensor fusion, AI-enabled processing at the tactical edge, and persistent coverage requirements sustain the largest share of market spending |

| Electronic Warfare & SIGINT | Advanced IADS proliferation and GPS-denial threats drive accelerating investment in standoff jamming and cyber-electromagnetic platforms |

| Airborne Early Warning & Control | NATO AWACS retirement and Indo-Pacific AEW fleet builds create a generational replacement cycle through the early 2030s |

| Maritime Patrol | Submarine threat growth, EEZ enforcement mandates, and coast guard modernization expand the addressable customer base beyond traditional navies |

| Aerial Refueling | Tanker fleet recapitalization in the U.S. and Europe, coupled with multi-role tanker-transport concepts, sustain steady demand |

ISR applications anchor overall market spending, while electronic warfare and SIGINT missions represent the highest-growth application category as contested electromagnetic environments become the operational norm.

By End User

| Sub-Segment | Key Trend |

| Defense & Homeland Security | Force modernization, counter-terrorism ISR, and integrated air defense drive the majority of global procurement budgets |

| Commercial & Civil | ISR-as-a-service, disaster response, environmental monitoring, and border security missions expand the civilian operator base |

Defense agencies remain the primary buyers, but commercial and civil operators are the fastest-growing end-user category as leasing and service-based models lower the cost of entry for non-military customers.