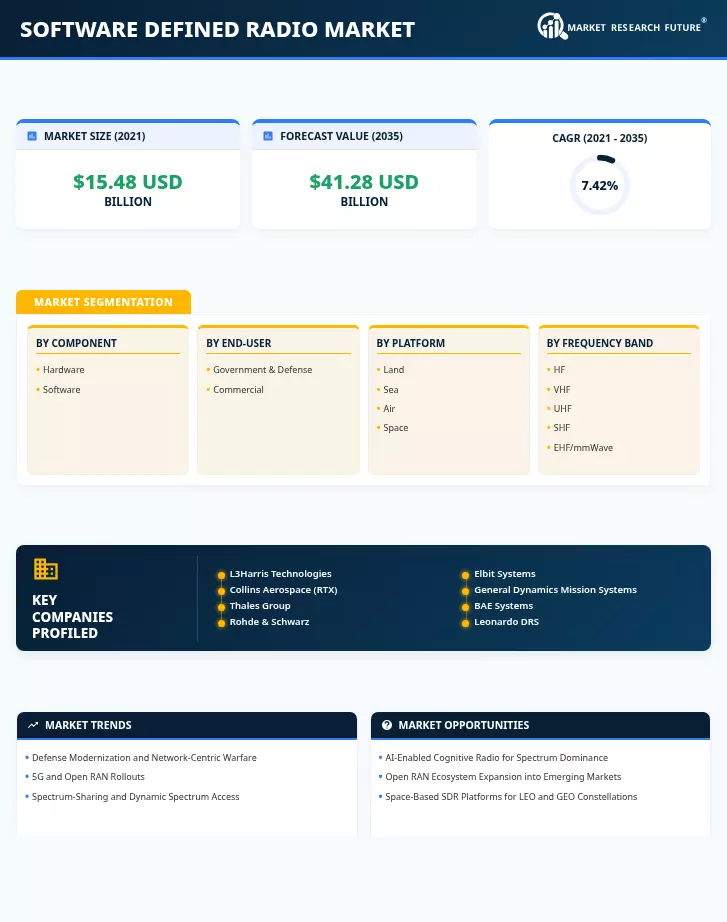

Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| Component | Hardware, Software | Hardware (58.9% share, 2025) | Software (8.1% CAGR) |

| End-User | Government & Defense, Commercial | Government & Defense (62.2% share, 2025) | Commercial (8.7% CAGR) |

| Platform | Land, Sea, Air, Space | Land (42.1% share, 2025) | Space (8.6% CAGR) |

| Frequency Band | HF, VHF, UHF, SHF, EHF/mmWave | VHF (45.6% share, 2025) | EHF/mmWave (9.1% CAGR) |

| Geography | North America, Europe, Asia-Pacific, South America, MEA | North America (35.5% share, 2025) | Asia-Pacific (9.3% CAGR) |

Market Segmentation Overview

By Component

| Sub-Segment | Key Trend |

| Hardware | GaN-on-SiC power amplifiers replacing GaAs; ruggedized COTS modules gaining traction; multi-channel RF front-ends for MIMO |

| Software | Waveform-as-a-service licensing models; containerized waveform apps; virtualized RAN functions reaching field maturity |

Hardware encompasses RF transceivers, antenna subsystems, digital signal processing radio boards, power amplifiers, and enclosures. The shift toward modular open-architecture designs — such as the U.S. Army's CMOSS/SOSA standard — is accelerating hardware interchangeability across vendors. Software includes waveform libraries, spectrum management applications, cryptographic middleware, and network management tools. Subscription-based delivery models are expanding the software revenue pool within the Software Defined Radio Market.

By End-User

| Sub-Segment | Key Trend |

| Government & Defense | JADC2 and coalition interoperability mandates; ESSOR and TCS mega-programs; electronic warfare integration |

| Commercial | Open RAN deployment acceleration; private 5G campus networks; CBRS dynamic spectrum access |

Government and defense buyers prioritize waveform agility, TEMPEST compliance, and multi-domain interoperability. Commercial adopters focus on cost efficiency, rapid time-to-service, and multi-vendor flexibility enabled by reconfigurable radio platforms.

By Platform

| Sub-Segment | Key Trend |

| Land | Manpack radios with integrated MANET; vehicular hub nodes for mobile ad hoc networks |

| Sea | Shipboard integrated communications suites; submarine ELF/VLF SDR upgrades |

| Air | Airborne SIGINT pods; UAV wideband datalinks; cognitive electronic warfare systems |

| Space | LEO constellation software-reprogrammable payloads; inter-satellite link SDR terminals |

Land platforms dominate current spending due to the sheer volume of dismounted and vehicular radios fielded by armies worldwide. Space is the breakout segment as satellite operators invest in cognitive radio systems that adapt frequency plans and modulation in orbit.

By Frequency Band

| Sub-Segment | Key Trend |

| High Frequency (HF) | Resurgence for long-range BLOS military communications; ALE 3G adoption |

| Very High Frequency (VHF) | Core tactical ground comms band; narrowband-to-wideband migration underway |

| Ultra High Frequency (UHF) | Military SATCOM uplinks; public safety P25/TETRA digital migration |

| Super High Frequency (SHF) | Wideband SATCOM trunking; high-data-rate point-to-point links |

| EHF/mmWave | 5G FR2 commercial rollouts; military LPI/LPD secure links; sub-THz 6G research |

VHF remains the workhorse band for ground-force tactical communications, but the EHF/mmWave segment is accelerating as both defense and commercial users adopt millimeter-wave SDR technology applications for high-throughput, jam-resistant connectivity.