Population Health Management Size

Market Size Snapshot

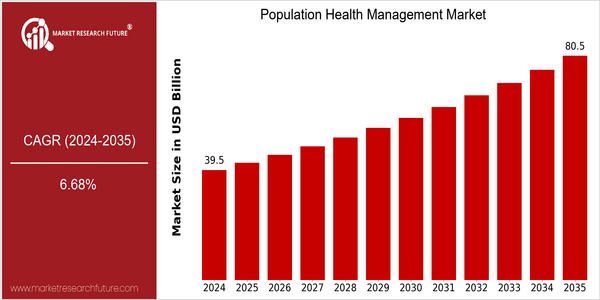

| Year | Value |

|---|---|

| 2024 | USD 39.52 Billion |

| 2035 | USD 80.5 Billion |

| CAGR (2025-2035) | 6.68 % |

Note – Market size depicts the revenue generated over the financial year

The population health management (PHM) market is poised to grow at a substantial rate. In 2024, it is estimated to be worth $39.52 billion, and it is expected to be worth $80.5 billion by 2035. This growth is based on a CAGR of 6.68% between 2025 and 2035. The growing emphasis on value-based care, combined with the rising prevalence of chronic diseases, is pushing health care organizations to adopt PHM solutions that can optimize the cost of care while improving outcomes. Further, advancements in data analytics, artificial intelligence, and telehealth are enabling more effective population health strategies, enabling health care organizations to better manage patient populations and improve care delivery. The leading companies in the PHM market, such as Cerner, Allscripts, and IBM Watson Health, are launching new products and entering strategic partnerships to expand their offerings and market share. Recent collaborations between these companies and other technology companies are expected to drive market growth and improve care delivery.

Regional Market Size

Regional Deep Dive

The population health management market is experiencing significant growth across regions, driven by the growing emphasis on value-based care, advancements in health care technology, and the need to improve patient outcomes. North America is characterized by a strong health care system and high penetration of digital health solutions. Europe is seeing a shift toward more integrated care models, while the Asia-Pacific region is rapidly expanding due to increasing health care spending and a rapidly aging population. Middle East and Africa are focused on improving access to and the quality of health care, while Latin America is leveraging technology to improve health data management and patient engagement.

Europe

- The European Union's Digital Health Initiative aims to standardize health data across member states, facilitating better population health management and interoperability among healthcare systems.

- Organizations such as NHS England are pioneering integrated care systems that focus on population health management, emphasizing preventive care and chronic disease management.

Asia Pacific

- Countries like Japan and Australia are increasingly adopting telehealth solutions as part of their population health management strategies, driven by the need to address aging populations and chronic diseases.

- The Indian government has launched the Ayushman Bharat scheme, which aims to provide comprehensive health coverage and improve health outcomes through effective population health management initiatives.

Latin America

- Brazil's Ministry of Health is promoting the use of digital health technologies to enhance population health management, particularly in remote and underserved areas.

- Mexico is seeing a rise in partnerships between public and private sectors to develop innovative population health management solutions, addressing the challenges of chronic diseases and healthcare access.

North America

- The U.S. government has implemented the Medicare Access and CHIP Reauthorization Act (MACRA), which incentivizes healthcare providers to adopt population health management strategies, thereby driving market growth.

- Key players like Cerner Corporation and Optum are investing heavily in AI and data analytics to enhance their population health management solutions, leading to improved patient outcomes and operational efficiencies.

Middle East And Africa

- The UAE's Ministry of Health and Prevention is implementing a national health strategy that emphasizes population health management to improve healthcare delivery and patient outcomes.

- In South Africa, the National Health Insurance (NHI) initiative is focused on enhancing access to healthcare services, which is expected to drive the adoption of population health management practices.

Did You Know?

“Approximately 80% of healthcare costs in the U.S. are attributed to chronic diseases, highlighting the critical need for effective population health management strategies.” — Centers for Disease Control and Prevention (CDC)

Segmental Market Size

The population health management market plays a crucial role in enhancing the health outcomes of a group of people. This market is currently experiencing a positive growth, mainly driven by the growing demand for individualized health care, the emergence of value-based care and the technological advancements in data analysis and telehealth solutions. The shift towards preventive care models and the need for improved chronic disease management are also expected to play a key role in the growth of the population health management market. At present, population health management solutions are being widely adopted by the leading companies in the United States and Europe. These solutions are mainly used for risk stratification, care management and patient engagement, especially in the management of chronic disease populations. In the recent past, the emergence of the CoViD-19 epidemic has also accelerated the adoption of digital health solutions. In addition, government mandates for interoperability and data sharing are also expected to drive the growth of this market. Artificial intelligence, machine learning and cloud-based platforms are playing a crucial role in the evolution of population health management strategies, enabling health care organizations to deliver more effective and efficient care.

Future Outlook

The population health management market is expected to grow at a CAGR of 6.77% from 2024 to 2035. This growth is based on the growing trend of value-based care, which encourages health care professionals to focus on patient outcomes rather than the number of services they provide. PHM solutions are expected to grow as the health care system moves toward more integrated care models. PHM solutions are expected to reach a penetration rate of over 60% in major health care markets by 2035, driven by the need to improve patient engagement and chronic disease management. In addition, technological innovations, such as the integration of artificial intelligence and big data, are expected to change the way health care professionals analyze population health data. These innovations will lead to more precise risk stratification and more personalized care plans, which will increase the effectiveness of the intervention. Also, government initiatives to promote health equity and reduce health disparities will further stimulate market growth. Telehealth and remote patient monitoring will also play an important role in the success of population health management. In addition, the development of population health management will help the health care system to meet the changing needs of different populations.

Leave a Comment