Integrated Vehicle Health Management Market Summary

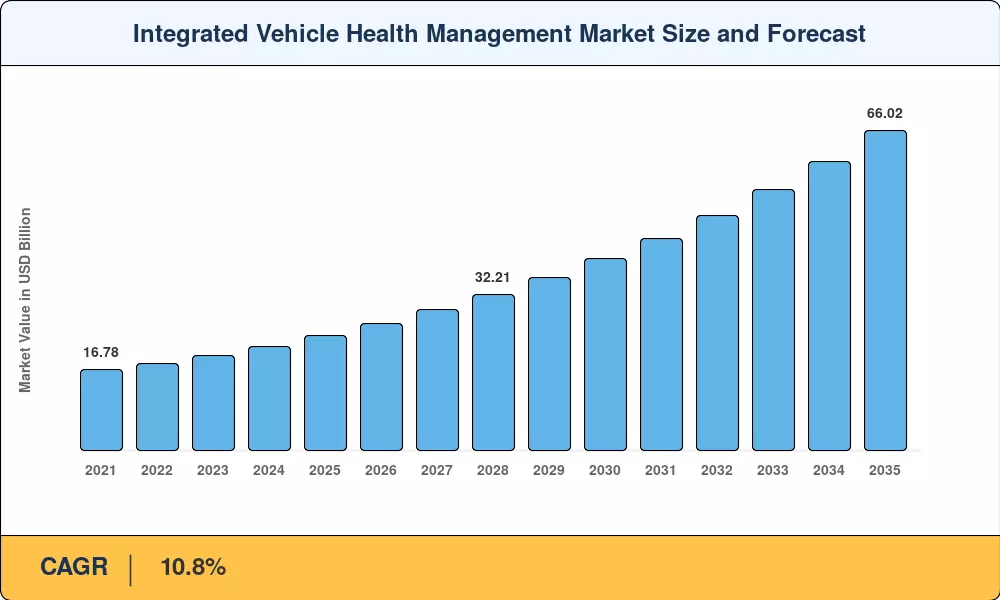

The Integrated Vehicle Health Management Market reached an estimated USD 23.68 Billion in 2025 and is projected to grow from USD 26.24 Billion in 2026 to USD 66.02 Billion by 2035, registering a compound annual growth rate of 10.8% across the forecast window. Two forces are accelerating this trajectory: mandatory on-board diagnostics regulations expanding from emissions monitoring to full powertrain telemetry across the EU and China, and fleet operators embedding uptime guarantees into e-commerce logistics contracts that penalize unplanned downtime at rates exceeding USD 500 per hour per vehicle [1].

Legacy scheduled-maintenance regimes — built around fixed mileage intervals and paper-based service records — are giving way to cloud-native health platforms that fuse sensor streams, edge computing, and machine-learning inference to predict component degradation weeks before failure. Automakers allocated over USD 4.2 Billion collectively toward connected-vehicle software platforms during 2023–2024, signaling a structural shift from hardware margin capture to recurring software subscription revenue [2]. Secure over-the-air update architectures compliant with ISO/SAE 21434 cybersecurity standards are becoming table-stakes for new model launches.

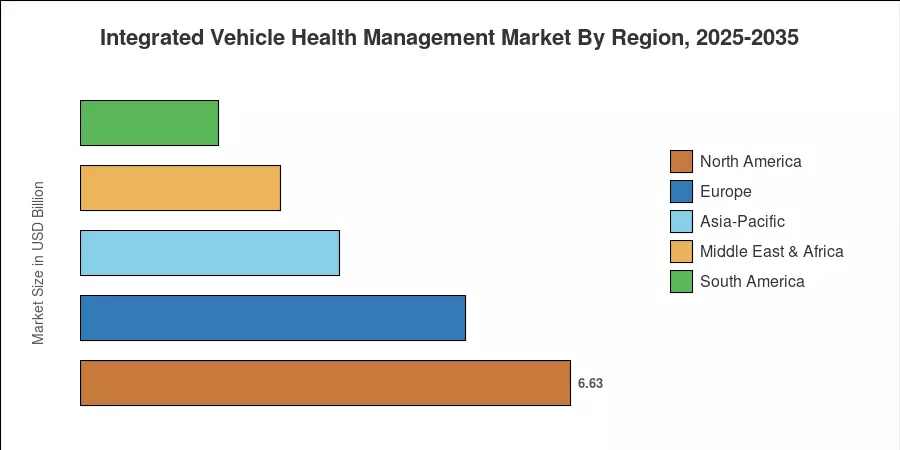

Asia-Pacific leads the Integrated Vehicle Health Management Market with approximately 35.4% of global revenue in 2024, driven by China's massive EV production base and India's commercial fleet digitization push. The region also registers the fastest expansion, posting a 14.8% CAGR through 2035. North America holds the second-largest share at roughly 28%, anchored by connected-truck mandates and aftermarket telematics adoption. Europe follows at approximately 22%, with regulatory momentum from Euro 7 and the EU Cyber Resilience Act shaping deployment timelines through 2030 and beyond [3].

Key Report Takeaways

• By Offering

- Hardware components — sensors, ECUs, gateways — accounted for roughly 58.8% of total Integrated Vehicle Health Management Market revenue in 2024, reflecting the sensor-dense architectures required for high-fidelity diagnostics.

- Software platforms are the fastest-growing offering category in the Integrated Vehicle Health Management Market, projected to expand at a 13.7% CAGR through 2035.

• By Channel

- OEM service centers captured approximately 44.9% of channel revenue in 2024, leveraging proprietary data access and warranty integration.

- Remote diagnostics platforms are on track for a 16.5% CAGR, driven by fleet telematics adoption.

• By Application

- Predictive maintenance held a leading 33.7% share of the Integrated Vehicle Health Management Market in 2024.

- Driver monitoring applications are advancing at an 18.1% CAGR through 2035, reflecting a regulatory push for in-cabin safety.

• By End-User

- OEMs represented 38.2% of end-user spending in the Integrated Vehicle Health Management Market during 2024.

- Service providers are set to expand at a 15.8% CAGR as third-party telematics platforms gain ground.

• By Vehicle Type

- Passenger vehicles represented about 48.4% of the Integrated Vehicle Health Management Market in 2024.

- Medium and heavy commercial vehicles are poised for a 13.1% CAGR through 2035.

• By Region

- Asia-Pacific commanded a 35.4% share of the Integrated Vehicle Health Management Market in 2024 and leads forecast growth at a 14.8% CAGR.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on a triangulated methodology combining bottom-up OEM hardware shipment tracking, top-down software licensing revenue analysis, and validated fleet telematics subscription data across 42 countries. Historical figures reflect actual reported revenues, while forecast projections apply the calibrated 10.8% CAGR with adjustments for regulatory milestones and technology adoption inflection points.