Platform as a Service Market Summary

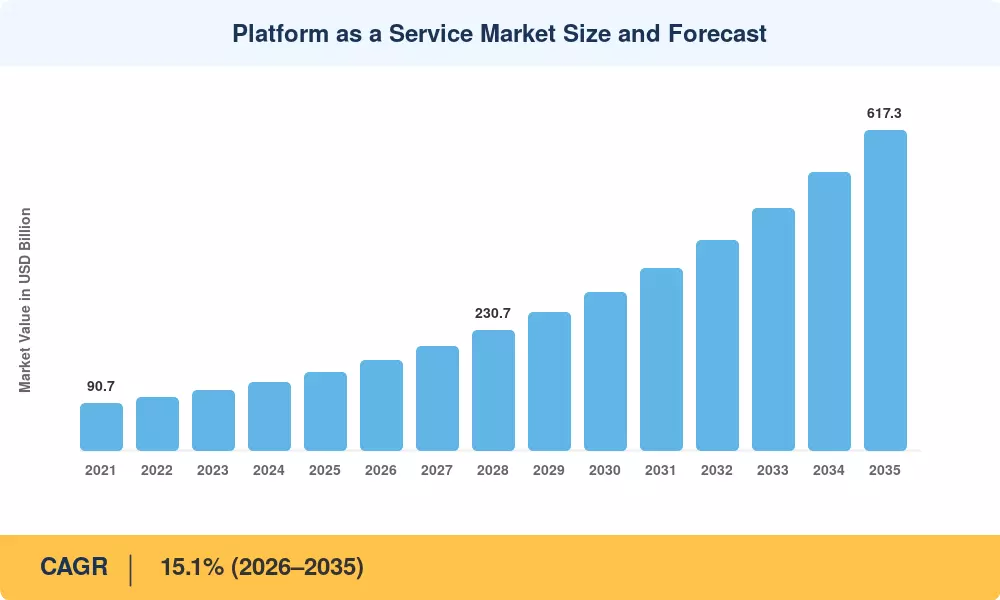

The Platform as a Service Market reached an estimated USD 150.80 Billion in 2025 and is projected to grow from USD 174.10 Billion in 2026 to USD 617.30 Billion by 2035, registering a CAGR of 15.1% during the forecast period (2026–2035). Enterprise commitments to cloud-first strategies — including the U.S. Federal Cloud Smart mandate and the EU's EUR 7.5 Billion Digital Europe Programme — have injected measurable urgency into platform adoption cycles [1]. Over 94% of enterprises now consume at least one cloud service, and roughly nine in ten pursue multi-cloud architectures to hedge against single-vendor risk [2].

The transformation underway replaces monolithic, on-premise middleware stacks with composable, API-driven platforms that compress development timelines from months to days. In 2024 alone, hyperscalers collectively allocated more than USD 160 Billion in capital expenditure toward cloud infrastructure, with a growing share directed at platform-layer services that embed AI model training, serverless compute, and event-driven integration natively [3]. Regulatory catalysts such as India's MeitY Cloud-First Policy and Japan's Digital Garden City initiative have further broadened addressable demand beyond traditional IT-heavy industries.

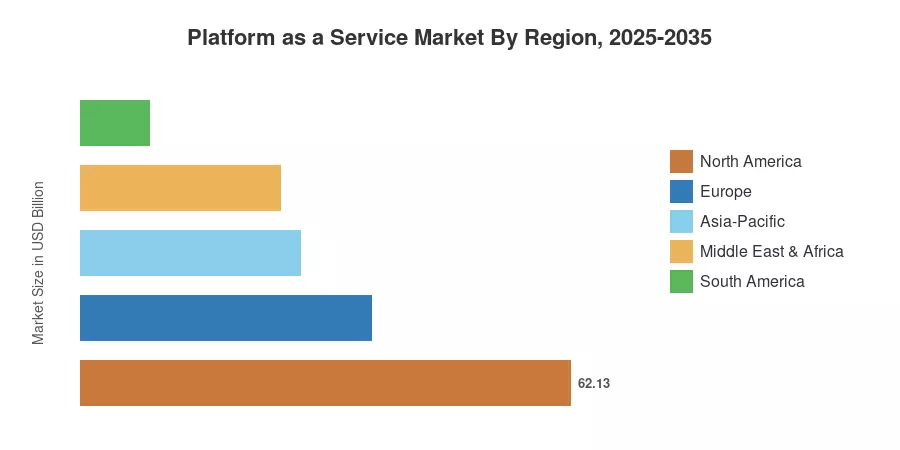

North America commanded roughly 41.2% of Platform as a Service Market revenue in 2025, buoyed by hyperscaler concentration and early enterprise maturity. Asia-Pacific is the fastest-growing geography, forecast to expand at an 18.5% CAGR through 2035 as manufacturers, banks, and government agencies across China, India, and ASEAN modernize legacy estates [4]. Europe holds the second-largest share at approximately 24.5%, driven by GDPR-compliant sovereign cloud programs and pan-European data-space initiatives. The next decade will see PaaS evolve from a developer convenience into the default operating layer for enterprise software.

Key Report Takeaways

• By Type

- Database PaaS captured approximately 48.1% of the Platform as a Service Market in 2025, reflecting its role as the backbone for transaction-heavy and analytics workloads across financial services and e-commerce.

- Integration PaaS is forecast to advance at a 21.0% CAGR through 2035, propelled by demand for real-time data orchestration across hybrid and multi-cloud estates.

• By Deployment

- Public PaaS accounted for roughly 69.2% of Platform as a Service Market revenue in 2025, as organizations prioritize rapid provisioning and elastic scaling.

- Hybrid PaaS is projected to record a 22.0% CAGR over the forecast period, reflecting regulated industries' need to balance control with agility.

• By Organization Size

- SMEs are expanding PaaS adoption at a 19.2% CAGR, leveraging pay-as-you-go economics to compete with larger incumbents.

• By End-User Industry

- Financial services led Platform as a Service Market end-user demand in 2025 with a 25.7% revenue share, deploying PaaS for compliance automation and real-time risk analytics.

- Healthcare is set to grow at an 18.3% CAGR through 2035, driven by telemedicine expansion and patient-data interoperability mandates.

• By Region

- North America held 41.2% of global revenue in 2025.

- Asia-Pacific is forecast to register the highest regional CAGR at 18.5% through 2035.

Market Size and Forecast (2021–2035)

Market Research Future derives historical values from vendor revenue disclosures, hyperscaler earnings reports, and third-party IT spending surveys. Forecast projections apply a bottom-up build across segments, calibrated against macroeconomic indicators (GDP growth, enterprise IT budgets) and validated through primary interviews with CIOs and cloud architects.