Papaya Market Summary

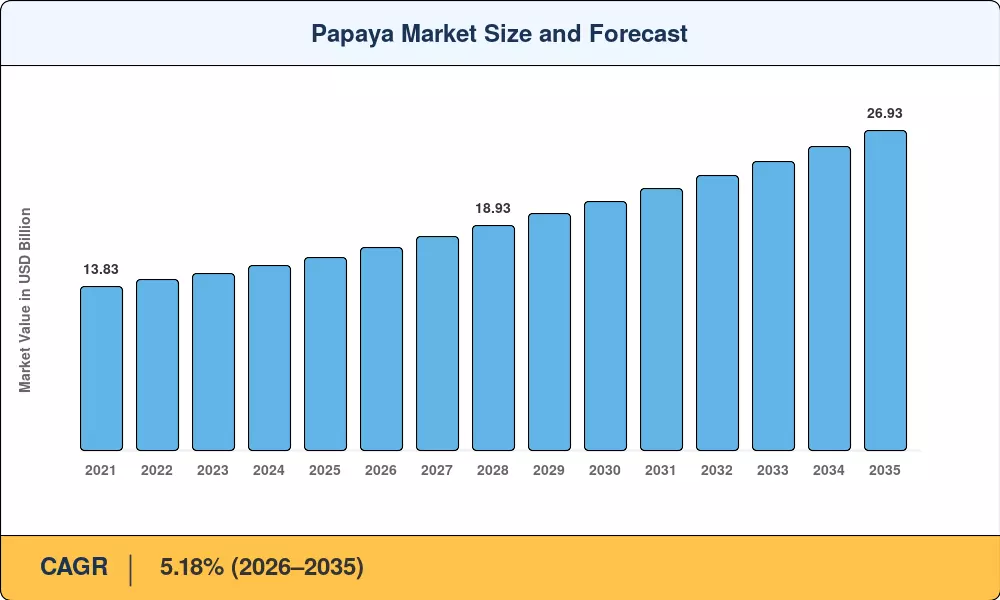

The papaya market reached USD 16.27 billion in 2025 and is projected to grow from USD 17.11 billion in 2026 to USD 26.93 billion by 2035, registering a CAGR of 5.18% during 2026–2035. Two converging forces are propelling this expansion: first, national food-security programs across South and Southeast Asia — India's National Horticulture Mission alone channeled over USD 320 million toward tropical fruit cultivation between 2022 and 2025 [1] — and second, the fast-rising consumer appetite for functional foods rich in the papain enzyme from papaya, which has become a staple ingredient in digestive supplements and clean-label food processing.

A quiet transformation is reshaping how papaya moves from farm to table. Traditional open-field cultivation with limited cold-chain infrastructure is giving way to precision-agriculture models that combine drip irrigation, tissue-culture propagation, and IoT-enabled harvest monitoring. Disease-resistant transgenic and hybrid cultivars — particularly solo and Maradol papaya varieties — have cut crop-loss rates by an estimated 15–20% in commercial plantations across Brazil and the Philippines [2]. The FAO estimates global papaya production exceeded 14 million metric tons in 2024, with biotechnology investments in papaya cultivation in the tropics expected to surpass USD 450 million cumulatively by 2028 [3].

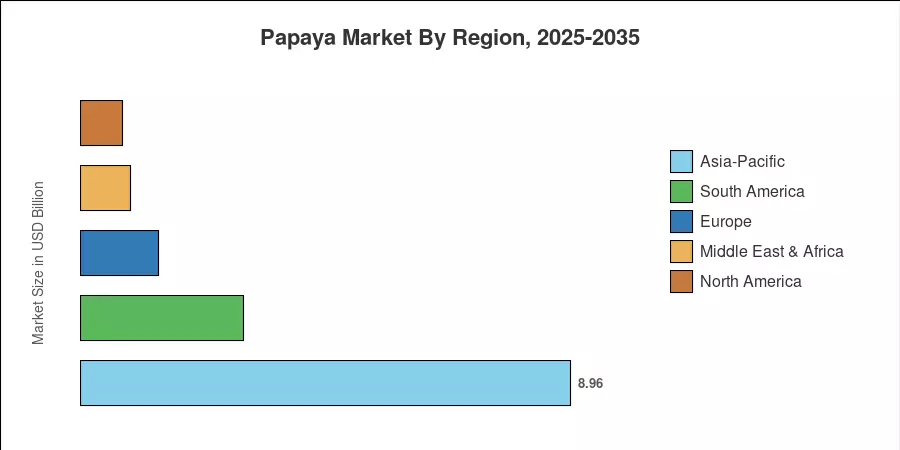

Asia-Pacific commands roughly 55.1% of the papaya market by value and simultaneously registers the fastest regional CAGR at 5.24%. South America holds the second-largest share at approximately 18.3%, driven by Brazil's dominant export volumes. North America accounts for 10.5% of the papaya market, fueled by health-conscious demand for fresh and dried papaya fruit in premium grocery channels. As cold-chain networks mature and e-grocery penetration deepens, the papaya market is positioned for sustained global expansion well into the next decade.

Key Report Takeaways

• By Form

- Fresh papaya held 62.4% of the papaya market share in 2025, driven by direct consumption and retail distribution growth across Asia-Pacific and South America.

- Papaya-based processed products (juice, puree, concentrate) are expanding at a CAGR of 6.31% through 2035, led by food-processing demand for papain enzyme from papaya.

- Dried papaya fruit is valued at USD 1.89 billion in 2025, reflecting rising snacking trends in North America and Europe.

• By Application

- Direct consumption accounts for 47.8% of the papaya market, as fresh and dried papaya fruit remains a dietary staple in tropical regions.

- Nutraceuticals and dietary supplements represent the fastest-growing application at a 6.57% CAGR, underpinned by growing awareness of papaya digestive health benefits.

• By Region

- Asia-Pacific dominates the papaya market with a 55.1% share, anchored by India, the Philippines, and Indonesia's massive cultivation base.

- North America is growing at a 4.76% CAGR, supported by expanding imports of solo and Maradol papaya varieties into the US and Canada.

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s market sizing integrates top-down trade-flow analysis (FAO, UN Comtrade export data) with bottom-up producer-level revenue estimates from 30+ countries. Historical values (2021–2024) are calibrated to government agricultural census data; forecast values (2026–2035) apply econometric modeling anchored to the 5.18% CAGR.