Lentil Market Summary

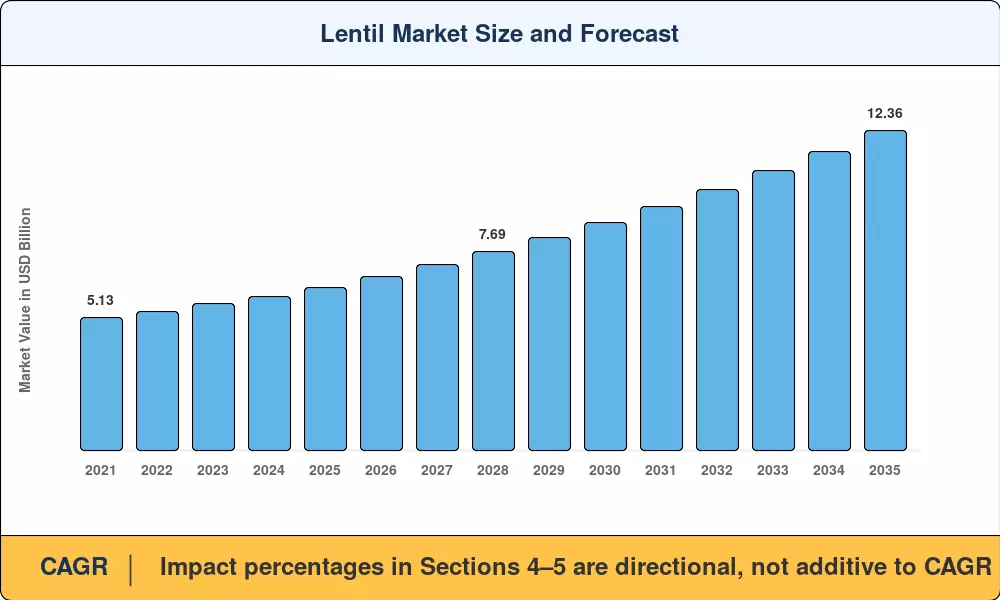

The global lentil market reached USD 6.28 billion in 2025 and is projected to grow from USD 6.72 billion in 2026 to USD 12.36 billion by 2035, registering a CAGR of 7.00% over the forecast period. Flexitarian and plant-forward dietary shifts across South and Southeast Asia are a primary catalyst, with India's National Food Security Act procurement quotas locking in minimum support prices that underpin grower margins and stabilize import demand cycles. Carbon credit schemes rewarding pulse crop production and trade for nitrogen fixation have simultaneously widened per-acre returns in Saskatchewan and South Australia, incentivizing rotation-intensive planting calendars [2].

Mid-stream processing technology is revolutionizing the lentil market. Legacy gravity-fed sorting tables are being replaced with optical color sorters, presently available for about USD 160,000, which level the playing field for quality access between major integrators and mid-tier facilities. These technologies have pushed the global average No. 1 grade recovery rate to about 78%, opening export grade yields for processors who previously sold via domestic cheap channels. Governments of Ethiopia and Bangladesh have pledged nearly USD 420 million cumulatively to pulse milling facilities up to 2028, indicating sustained investment in dry and split lentil types [3][4].

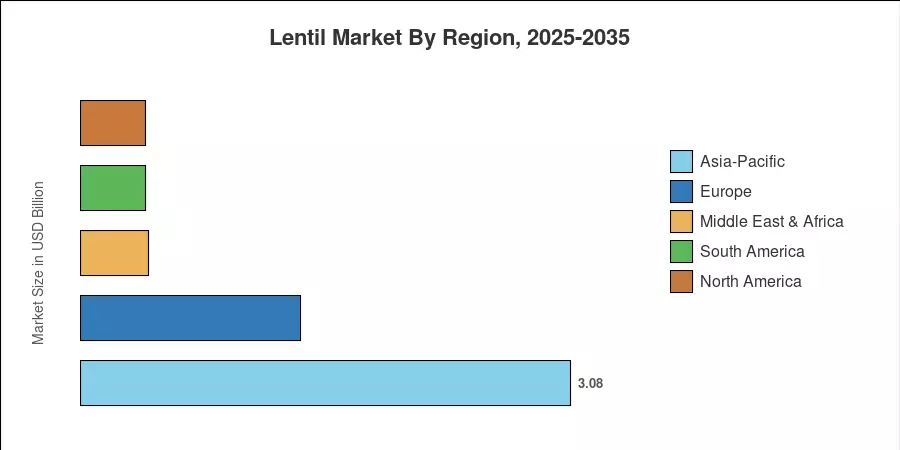

Asia-Pacific commands a dominating position in the lentil market, generating about 49% of the worldwide income, propelled by household consumption habits in India, Bangladesh, and Nepal. Africa is the fastest expanding area with a projected CAGR of 6.9% through 2035, driven by school feeding regulations and urbanization-driven demand for convenient foods. Europe is second at 22% share, from organic retail premiums for red, green and black lentils purchased under identity-preserved contracts. Increased acknowledgment by food formulators of the importance of lentil protein and fiber content suggests the potential for increasing value addition at each node of the supply chain until 2035 [5].

Key Report Takeaways

• By Type

- Red lentils accounted for the largest revenue share of the lentil market in 2025, reflecting dominant consumption in South Asian dal preparations and Middle Eastern soups

- Green lentils are forecast to grow at a CAGR of 7.6% through 2035, propelled by rising demand in European salad and ready-meal applications

- Black and brown lentil varieties are gaining traction in specialty health-food channels, reaching USD 0.74 billion in 2025

• By Form

- Dried and split lentil varieties represented over 68% of global volume in 2025 due to shelf stability and cost efficiency in bulk trade

- Lentil flour and protein isolates are the fastest-growing form segment in the lentil market, with emerging applications in plant-based meat analogs

• By Geography

- Asia-Pacific dominated the lentil market at approximately 49% share in 2025, underpinned by Indian government procurement programs

- Africa is projected to register a 6.9% CAGR as school feeding mandates expand pulse crop production and trade volumes

Lentil Market Size and Forecast (2021–2035)

Market size estimates are based on FAO production and trade statistics and national customs data from the top 15 producing and importing nations, supplemented with primary interviews with grain traders, processors and pulse breeding programs. Historical statistics (2021-2024) are based on realized wholesale values; the base year 2025 is anchored to validated shipment records. Forecasts (2026–2035) are derived from a calibrated compound growth rate based on modeling of consumption elasticity, predictions of the trend in area, and policy scenario analysis[6].