Green Hydrogen Market Summary

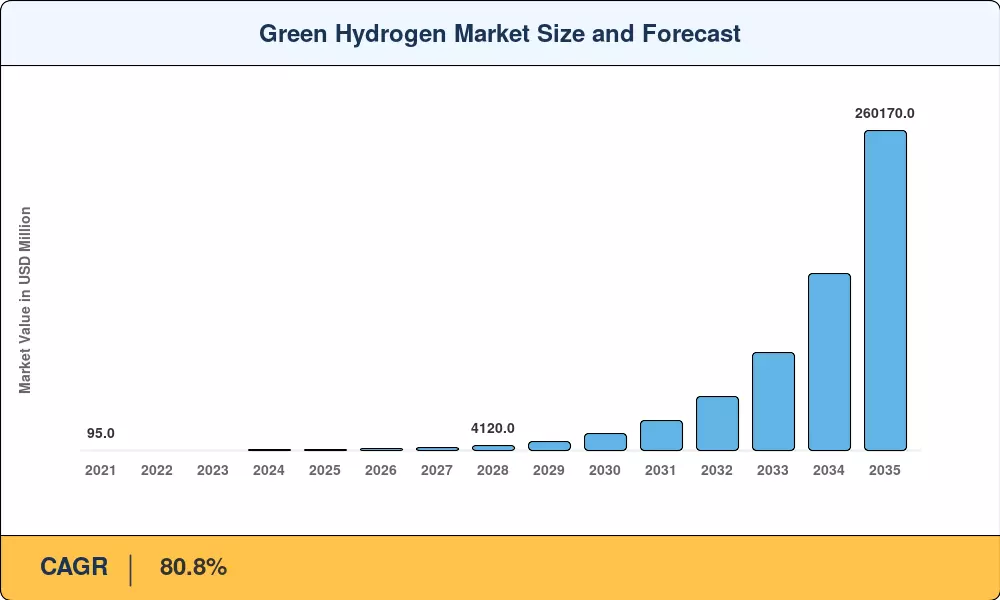

The Green Hydrogen Market stood at USD 680 Million in 2025 and is projected to reach USD 1,260 Million in 2026 before climbing to USD 260,170 Million by 2035, reflecting a CAGR of 80.8% over the 2026–2035 forecast period. Two forces are pulling this trajectory upward: the EU's EUR 3 billion Hydrogen Bank auction rounds, which have triggered binding offtake contracts across refineries and steelmakers, and the U.S. Inflation Reduction Act's Section 45V production tax credit, which now delivers up to USD 3.00 per kilogram of qualifying clean hydrogen [1][2]. Together, these policy anchors have converted what was a pilot-stage curiosity into a bankable asset class.

On the technology front, the shift away from fossil-derived gray hydrogen is accelerating faster than most 2022-era projections anticipated. Electrolyzer gigafactories announced between 2023 and 2025 — representing over 35 GW of combined annual manufacturing capacity — are pushing stack costs below USD 400/kW for atmospheric alkaline units and below USD 650/kW for polymer-electrolyte-membrane systems [3]. Renewable electricity purchase agreements struck at sub-USD 25/MWh in the Middle East and parts of South America are compressing the levelized cost of hydrogen toward USD 2.50/kg, a threshold widely regarded as the competitiveness crossover against unabated gray hydrogen [4].

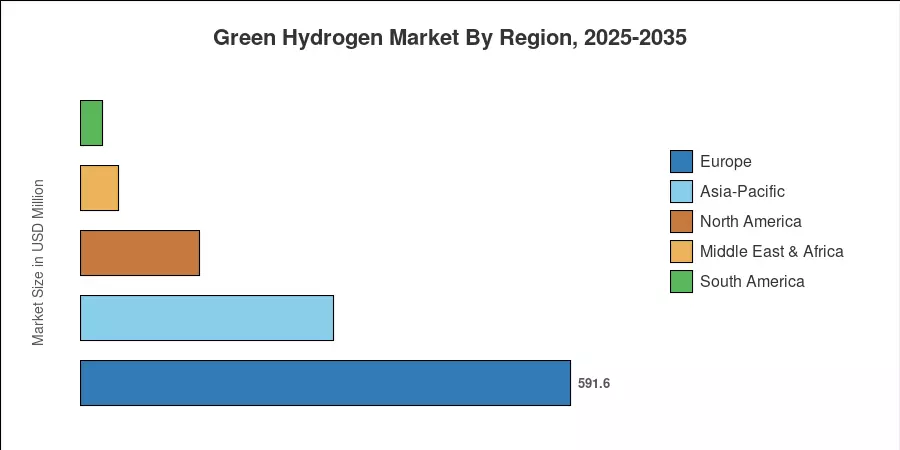

Asia-Pacific controlled approximately 45% of the Green Hydrogen Market in 2025, driven by China's National Hydrogen Roadmap targets and India's National Green Hydrogen Mission, which earmarked USD 2.3 billion in incentives [5]. Europe is the fastest-growing region, forecast to register an 87% CAGR through 2035 as carbon border adjustment obligations and REPowerEU mandates compel industrial buyers to lock in green supply. North America accounted for the second-largest share, underpinned by project announcements across the U.S. Gulf Coast hydrogen hub corridors. The next decade will separate early-mover economies that build pipeline and port infrastructure from those forced to import molecules at a premium.

Key Report Takeaways

• By Technology

- Alkaline electrolysis commanded roughly 51% of global installed capacity in 2025, anchored by mature stack designs and lower upfront capital intensity.

- PEM electrolysis is forecast to register the highest segment CAGR at approximately 99% through 2035, driven by superior dynamic-response characteristics that pair well with variable renewable generation.

• By End-User Industry

- Refining held an estimated 38% share of the Green Hydrogen Market in 2025, as petroleum processors began substituting gray feedstock to meet scope-1 decarbonization targets.

- The chemicals segment is projected to expand at roughly 90% CAGR to 2035, reflecting green ammonia commitments from fertilizer producers across Europe and South Asia.

• By Region

- Asia-Pacific captured about 45% of the Green Hydrogen Market in 2025, led by state-backed electrolyzer deployment in China and India.

- Europe is expected to advance at approximately 87% CAGR through 2035, propelled by binding renewable-hydrogen mandates under the revised Renewable Energy Directive.

Green Hydrogen Market Size and Forecast (2021–2035)

Market sizing combines bottom-up electrolyzer capacity tracking with top-down demand modeling across end-user verticals. Historical figures (2021–2024) draw on operational project databases, while forecasts incorporate announced FID-stage projects, committed policy subsidies, and proprietary cost-learning curves for electrolyzer stacks and renewable power procurement.