Flaxseeds Market Summary

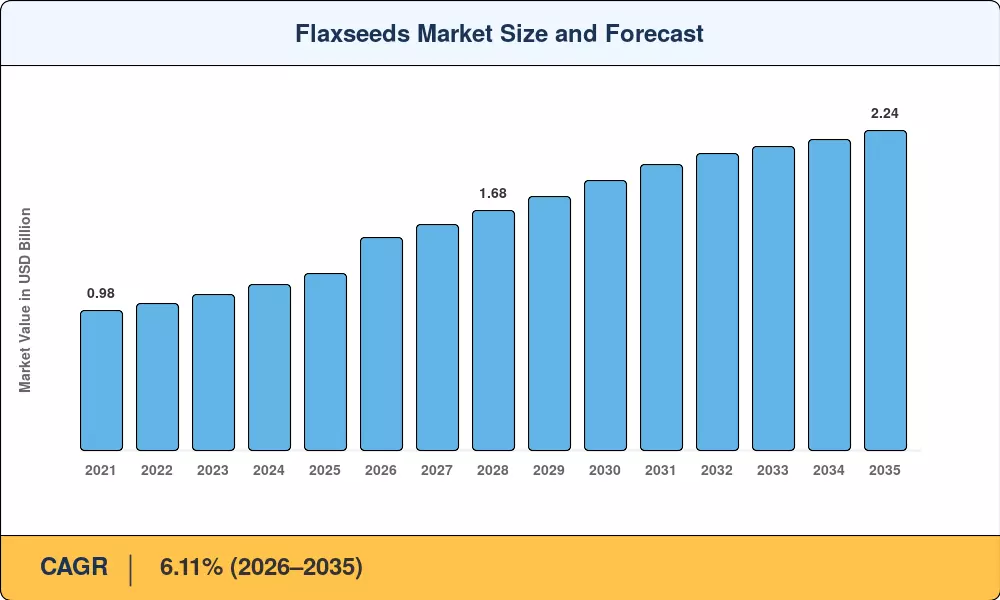

The global flaxseed market was valued at approximately USD 1.24 billion in 2025 and is projected to reach USD 1.49 billion in 2026, advancing to USD 2.24 billion by 2035 at a CAGR of 6.11% over the 2026–2035 forecast window. Two catalysts are doing much of the heavy lifting here: the USDA Emergency Commodity Assistance Program, which has actively incentivized acreage expansion among North American producers, and rising EU regulatory pressure on synthetic fiber usage in automotive composites, which is accelerating demand for natural flax fiber across European manufacturing supply chains. The flaxseed market sits at an interesting intersection of food, feed, and industrial applications — a cross-sector position that insulates it from single-sector demand shocks.

There is a big change in the processing technique. Cold-press extraction lines, which were historically the norm for flaxseed oil production, are being replaced by supercritical CO2 extraction systems, which offer better omega-3 fatty acid retention and longer shelf-life profiles. Several Canadian processors have pledged a combined total of more than CAD 85 million to boost extraction capacity between 2023 and 2026. Meanwhile, ground and whole flaxseeds used for functional foods are benefiting from microencapsulation technology that conceals the bitter taste and preserves the nutritious fiber of flaxseeds. This major hurdle had previously hampered retail adoption.

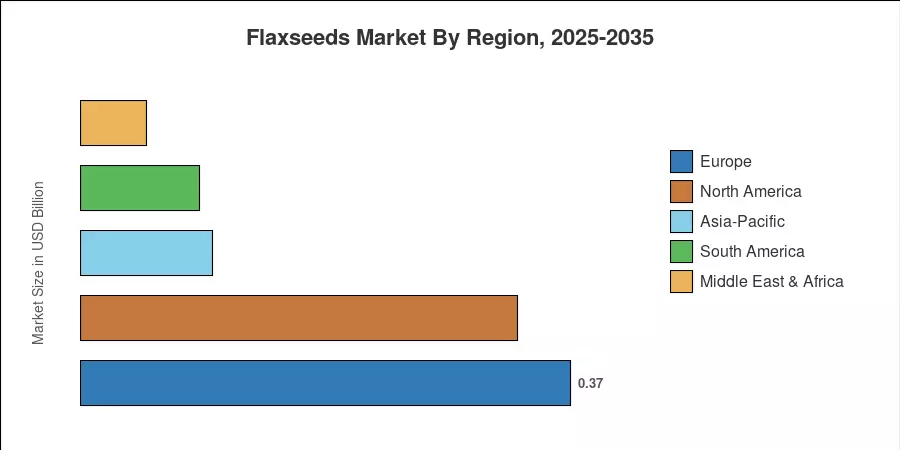

Europe is projected to hold the largest share of the worldwide flaxseed market revenue in 2025 and account for almost 29.5%. The presence of established retting infrastructure and high demand from automotive bio-composite applications supports this. Asia-Pacific is the fastest expanding area, with growth expected to be at 8.1% CAGR through 2035, led by China’s quickly increasing functional food processing sector and India’s emerging oilseed crush capacity. North America has the second-highest share at about 26.8%, and blockchain traceability systems are adding a margin premium for specialty-grade manufacturers. The next decade will reward those who can straddle nutrition and industrial uses.

Key Report Takeaways

• By Product Form

- Ground and whole flaxseeds collectively account for the largest product share in the flaxseeds market, commanding approximately 48.3% of total revenue in 2025, driven by direct retail incorporation into cereals, breads, and smoothie products.

- Flaxseed oil and lignans extracts represent the fastest-growing product sub-segment at an estimated 7.4% CAGR through 2035, propelled by nutraceutical and pharmaceutical demand for concentrated bioactive compounds.

• By Application

- The food and beverage application segment leads the flaxseed market with a dominant share, reflecting the broad integration of dietary fiber from flaxseeds and linseed omega-3 fatty acids into mainstream consumer products.

- Industrial applications — principally flax fiber in bio-composites for automotive interiors — are expanding at approximately 7.9% CAGR, the fastest pace among all application categories in the flaxseeds market.

• By Region

- Europe led with approximately 29.5% revenue share in the flaxseed market in 2025, supported by agro-climatic advantages and long-standing retting processing infrastructure.

- Asia-Pacific is the fastest-growing region in the flaxseed market, projected at ~8.1% CAGR through 2035, with China accounting for the bulk of incremental import demand.

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)’s approach to market sizing triangulates supply side production data from national agriculture agencies (USDA, Statistics Canada, Eurostat), demand side consumer surveys and trade flow databases (UN Comtrade, ITC). Historical figures for 2021-2024 are associated with the FAO oilseed production data. Forecast values are based on Market Research Future (MRFR)’s proprietary demand-weighting model in food, industrial and nutraceutical end-uses. The annual growth rates are compounded from the calibrated base.

.webp?v=1781612628)