Market Summary

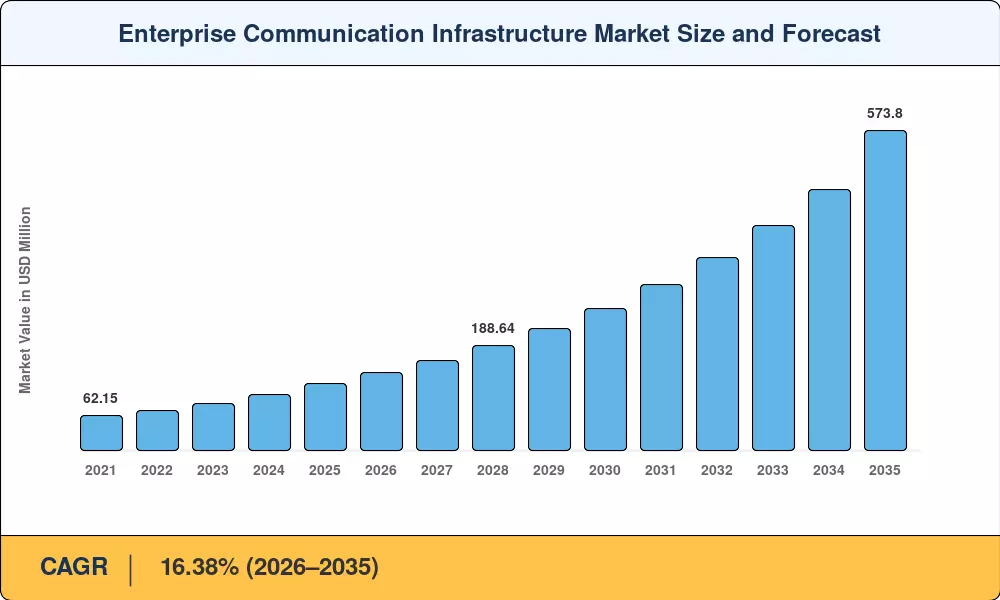

The Enterprise Communication Infrastructure Market reached an estimated USD 119.67 Billion in 2025 and is projected to grow from USD 139.28 Billion in 2026 to USD 573.80 Billion by 2035, registering a CAGR of 16.38% during the forecast period (2026–2035). This expansion is anchored by aggressive enterprise digital transformation budgets — global IT spending on communication and collaboration platforms exceeded USD 480 Billion in 2024 according to Gartner — and by regulatory mandates pushing organizations toward secure, compliant communication architectures. SD-WAN for enterprise branch connectivity has emerged as a cornerstone investment category, displacing legacy MPLS circuits at an accelerating pace.

A sweeping technology overhaul is reshaping how enterprises manage voice, video, messaging, and data traffic. Legacy TDM-based PBX systems and static WAN topologies are giving way to cloud-native unified communications, software-defined networking, and IP PBX and UCaaS enterprise telephony platforms. The U.S. Federal Communications Commission's ongoing broadband modernization programs and the European Commission's Digital Decade 2030 initiative — targeting gigabit connectivity for all enterprises — are funneling billions into network infrastructure for hybrid work. These policy frameworks translate directly into procurement cycles for enterprise LAN WAN and SDLAN architecture upgrades.

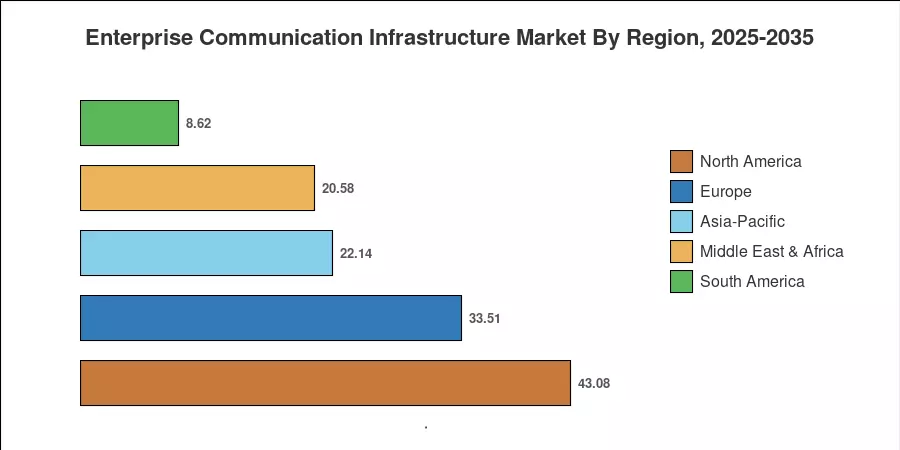

North America commands the largest share of the Enterprise Communication Infrastructure Market at roughly 36% of global revenue, driven by mature cloud adoption and early 5G rollouts. Asia-Pacific is the fastest-growing region with a CAGR exceeding 18.5%, propelled by India's Digital India program and China's aggressive 5G private networks for enterprise communications deployments. Europe holds the second-largest share near 28%, buoyed by GDPR-compliant communication mandates and the EU's Connected Europe broadband strategy [4]. The trajectory through 2035 points to sustained double-digit expansion as hybrid work, AI-driven collaboration, and edge computing become standard enterprise requirements.

Key Report Takeaways

• By Deployment

- Cloud deployment holds approximately 61% share of the Enterprise Communication Infrastructure Market, reflecting the rapid migration from on-premise PBX and legacy telephony to UCaaS and hosted collaboration platforms

- On-premise deployment is forecast to grow at a CAGR of 11.2%, sustained by regulated industries — banking, defense, healthcare — that require data sovereignty and on-site IP PBX and UCaaS enterprise telephony installations

• By End User

- IT and Telecom is the dominant vertical, valued at approximately USD 41.9 Billion in 2025, as carriers reinvest in enterprise LAN WAN and SDLAN architecture to deliver managed SD-WAN for enterprise branch connectivity services

- BFSI represents the fastest-growing end-user segment with a CAGR of 18.1%, driven by compliance-grade unified communications and real-time trading floor connectivity

• By Region

- North America accounts for ~36% of the Enterprise Communication Infrastructure Market, with the US alone contributing over 78% of regional revenue

- Asia-Pacific is projected to reach USD 178.5 Billion by 2035, underpinned by 5G private networks for enterprise communications adoption across manufacturing hubs in China, Japan, and South Korea

- Europe's share stands near 28%, shaped by network infrastructure for hybrid work investments mandated under EU digital sovereignty policies

Market Research Future (MRFR)'s forecasting model integrates bottom-up vendor revenue analysis, top-down macroeconomic correlation, and primary survey data from over 350 enterprise IT decision-makers globally. Historical figures (2021–2024) are validated against public filings and IDC/Gartner IT spending trackers. Forecast projections (2026–2035) apply a calibrated CAGR of 16.38%, adjusted for anticipated policy shifts, technology adoption S-curves, and regional GDP-weighted demand models.